PepsiCo has seen and acted upon the structural shift seen away from sugary beverages to healthier alternatives. Now, COVID-19 has also created another wave of change for consumption preferences. There is a lack of mobility, and that has led to a slump in away-from-home channels such as gas stations, business places, restaurants and other immediate consumption channels leading to lowering profitability. However, PepsiCo CFO Johnston claims to have less exposure to the ‘hardest hit’ channels, in comparison to Coca Cola. According to Reuters, about 90% of PepsiCo’s volumes are sold through retail store channels, in comparison to only 60% of Coca-Cola’s volumes. Consequently, it has led to increased penetration of the household.

As consumers shift to the comforts of their homes and order conveniently from their phones, PepsiCo has the opportunity to develop its e-commerce and mobile commerce application channels in the wake of this increased usage. Still, shifting away from their traditional channels and venturing into this rising channel is going to require more investment to maximize their gains.

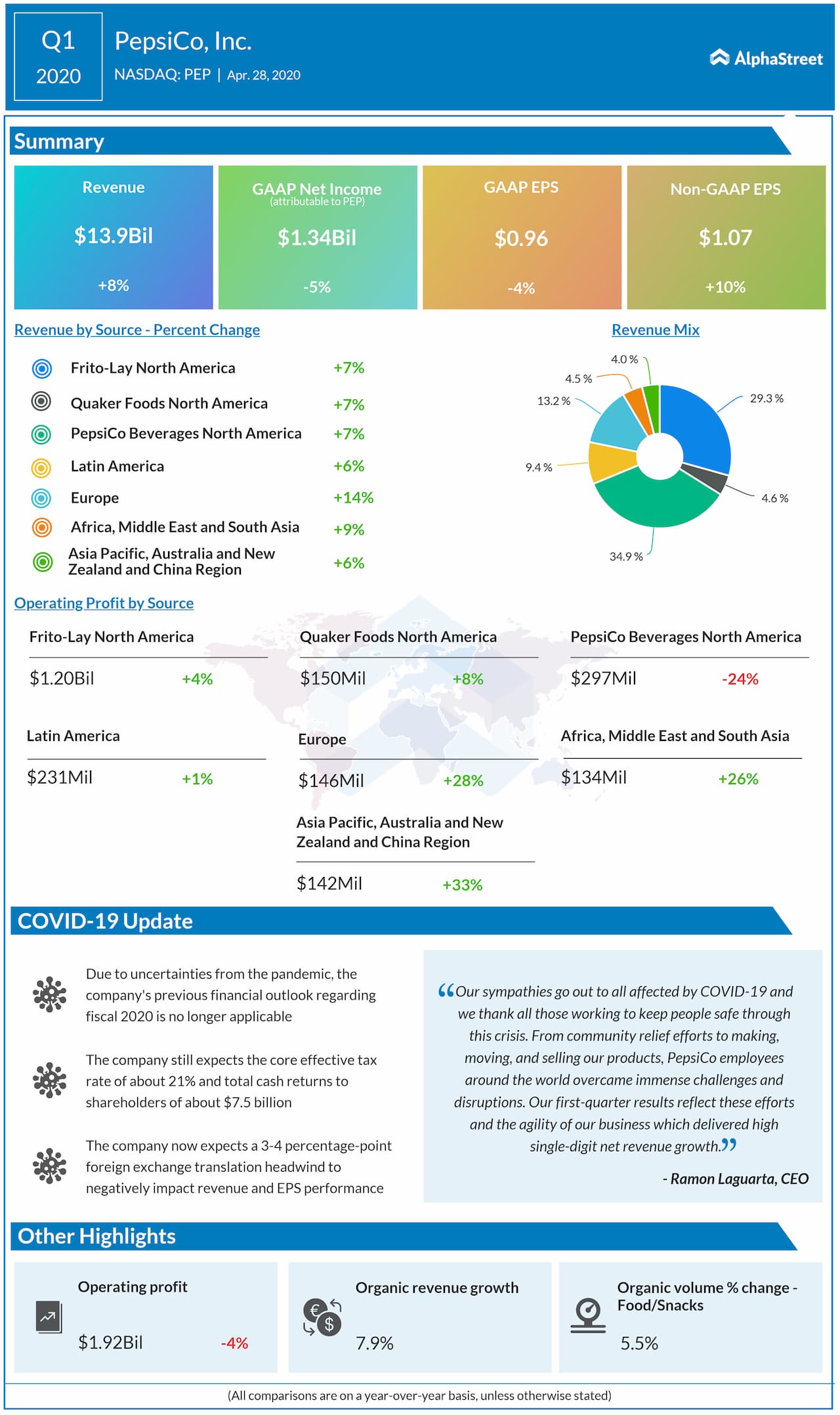

COVID-19 has also contributed to an increase in consumers’ basket size, due to stock ups and lockdown restrictions. The revenue increase from the pandemic was reflected across PepsiCo’s portfolio, contributed by its snack brands (FLNA) through Cheetos and Tostitos, in the foods brand (QFNA) through Quaker Oatmeal and ready-to-eat cereals, and in beverages (PBNA) through non-carbonated beverages in the overall water portfolio and Gatorade in the USA. From emerging markets, there are risks from decreasing disposable incomes and distribution. International markets contribute almost 30% revenue in food, snacks and beverages.

The quarterly earnings forecast for June 2020 and September 2020 have seen multiple down revisions, no up revisions. PepsiCo has given an expectation of shrinkage of its revenues by ‘low single digits’ due to the closure of the channels like restaurants, movie theatres and sports stadiums.

PepsiCo is signaling increasing operating costs in the future for smoothing out supply chain disruptions, increased advertising, write-offs of receivables from their customers (such as restaurants and other businesses that have been impacted by the ongoing crisis) and in manufacturing efficiencies. It says the capital allocation priorities begin by reinvesting, then go to dividend payouts, then M&As and end with share repurchase.

Dividend trend

Starting from a $0.14 cash dividend per share in 2000 to $0.955 cash dividend in 2020, there is a whopping 582% increase over the past 20 years. PepsiCo has been giving increasing dividends since the past 47 years. It is counted as one of the Dividend Aristocrats – a group of companies in the S&P 500 Index that has given 25+ years of consecutively increasing dividends.

PepsiCo exceeded the Street’s consensus with its Q1 FY21 earnings, with group revenues at $13.88 billion against a forecasted $13.2 billion. It attributes this increase to its feet on the ground and the robust Super Bowl season along with the end-of-the-quarter pantry stocking due to COVID-19 restrictions. Even in these trying times where companies are slashing dividends in order to conserve cash, PepsiCo is giving back to the shareholders, to the tune of $7.5 billion with share repurchases and cash dividend payouts, from its cash-generative business.

Although, one key piece of information hidden is the 2.8% yield, which falls on the lower side of the 5-year historical yield range that PepsiCo has been offering, reflecting the uncertainty in the prospective macroeconomic environment with a somewhat conservative yield offering. If PepsiCo plays its cards right and adapts to the changes with the right pace, they can cash in on the uncertainty.

Outlook

PepsiCo might have to increase its marketing, higher advertising and operational expenditures to retain the newly gained customers through changing consumption patterns. However, given that it’s been a defensive company with a diversified portfolio with increasing market share through acquisitions, increasing organic growth and multi-channel penetration, PepsiCo could come out as a stronger player in the market.

(Written by Shreya Chandra)