Shares of Philip Morris International Inc. (NYSE: PM) were down slightly on Friday, a day after the company reported its fourth quarter 2022 earnings results. Both the top and bottom line numbers beat estimates and the company expects to see earnings growth in the coming year. With the achievement of two important milestones in the form of the IQOS agreement and the Swedish Match acquisition, PMI believes it is well positioned to accelerate its smoke-free transformation in the years to come.

Quarterly performance

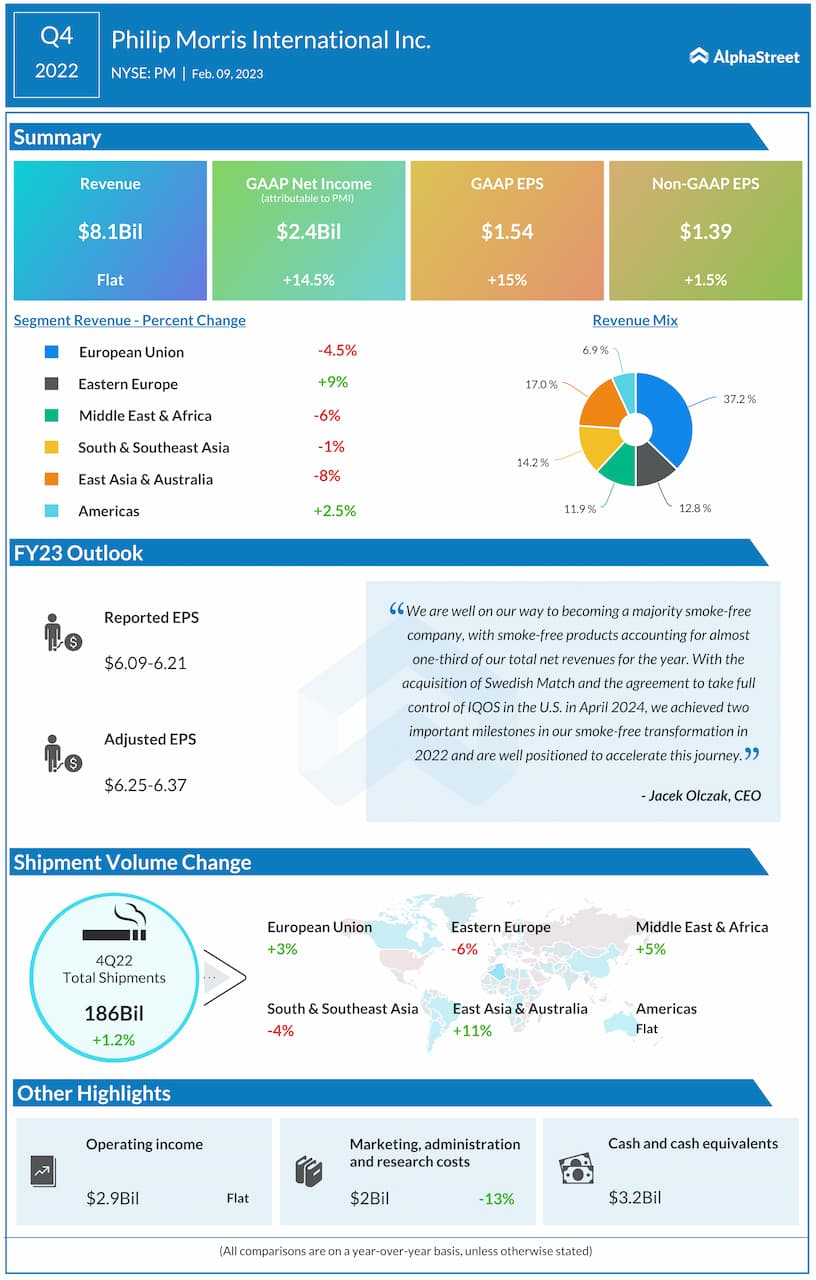

In the fourth quarter of 2022, Philip Morris generated revenue of $8.15 billion, which was relatively flat compared to the year-ago period on a reported basis. On an adjusted basis, revenue grew 7.5%, helped by higher heated tobacco units (HTU) volume and higher device volume as well as favorable pricing. GAAP EPS grew 15% to $1.54 while adjusted EPS rose 1.5% to $1.39.

Smoke-free portfolio

In 2022, PMI achieved two important strategic milestones – the acquisition of Swedish Match and the agreement to take control of IQOS in the US in 2024. On its quarterly conference call, the company said these achievements will help in accelerating its smoke-free transformation. PMI sees vast potential to drive growth for its smoke-free products in the US through leading brands like IQOS and ZYN.

The global roll-out of IQOS ILUMA is a top priority for Philip Morris and it expects to make meaningful progress on this goal in 2023. During the fourth quarter, the company launched ILUMA in eight new markets including Italy, Portugal and South Korea, bringing the total to 16. More than half of PMI’s total HTU volume now comes from markets where ILUMA has been launched.

The Swedish Match acquisition and the addition of leading nicotine pouch brand ZYN opens up significant growth opportunity for PMI in the US. In Q4, ZYN’s shipment volume grew 35%. In addition, its retail value share remains strong at 75.7%. Philip Morris is also working on the expansion of nicotine pouches into international markets.

Philip Morris expects to deliver around $13.5 billion in smoke-free net revenues in 2023 on a constant currency basis, including Swedish Match, compared to $10 billion in 2022. This is estimated to approach 40% of total PMI net revenues for the year.

Outlook

In 2023, Philip Morris expects organic net revenues to grow 7-8.5%, driven by a step-up in combustible pricing and progress from IQOS. Reported EPS is expected to be $6.09-6.21 in 2023 compared to $5.81 in 2022. Adjusted EPS is expected to be $6.25-6.37 compared to $5.98 in 2022.