More than two years after the coronavirus outbreak, the film industry in the U.S is recovering from one of the biggest setbacks in its history. Though widespread theatre closures led to a mass shift to online platforms, the rebound in activity in recent months indicates that movie theatres would remain as relevant as ever.

Moving iMage Technologies, Inc. (NYSE: MITQ) is a market leader in the thriving motion picture exhibition industry, providing equipment and technology needed for the production and exhibition of films. The company’s services range from custom engineering and digital technology solutions for 3D to audiovisual integration and installation & project management.

In an exclusive interview with AlphaStreet, Joe Delgado, co-founder and EVP of sales & marketing at Moving iMage Technologies, spoke about the various aspects of the business and emerging trends in the industry.

As a public company, how was the journey since last year’s IPO in terms of expanding the business and creating shareholder value?

The excitement level has risen in line with our revenue growth. We communicated a plan of secular growth drivers that would serve as tailwinds to the business, combined with our existing leadership in the market and a proprietary product strategy that would drive higher margins and recurring revenues. So far, we’ve raised our initial FY22 revenue growth guidance to 93 to 121%, reshaped our balance sheet, and have taken advantage of opportunities we wouldn’t have been able to previously, including accounts payable discounts and opportunistic inventory purchases. Our cash on hand and equity currency also allow us to execute on the M&A pillar of our growth strategy.

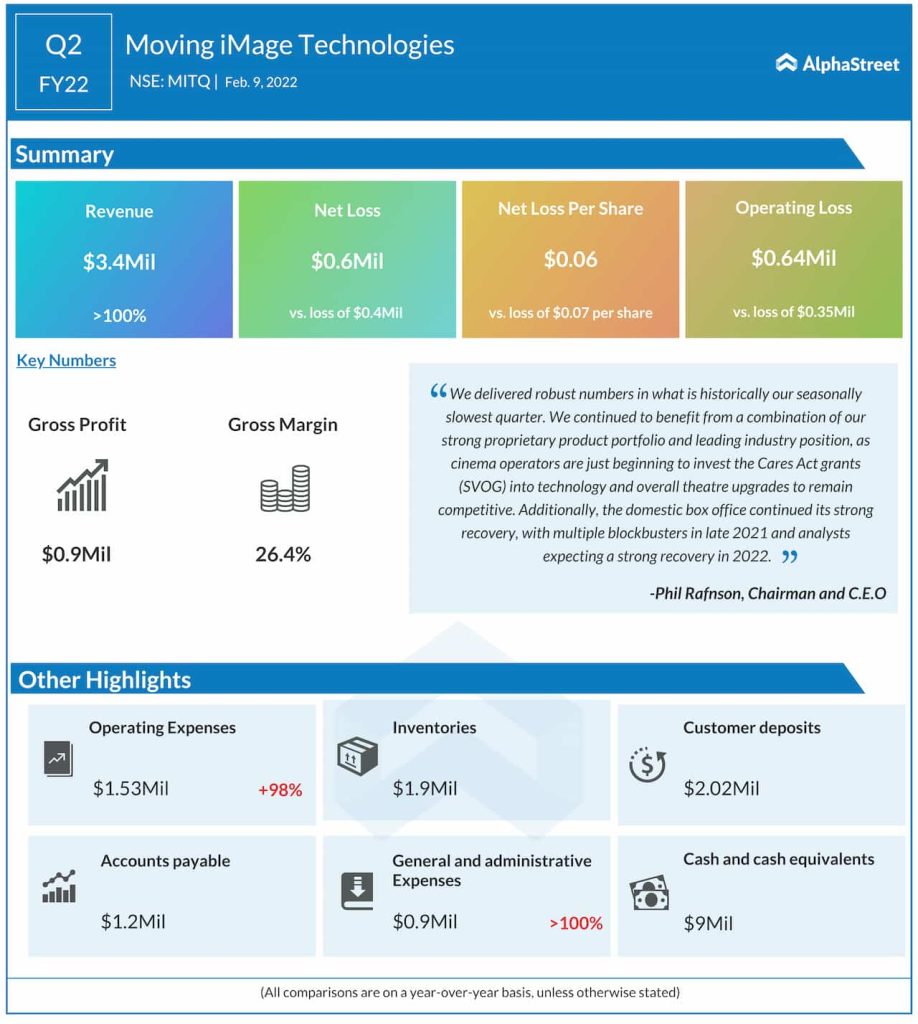

Also Read: Moving Image Technologies Inc (MITQ) Q2 2022 Earnings Call Transcript

Do you see any long-term impact to the business from the ongoing shift from theaters to OTT platforms, which accelerated after the coronavirus outbreak?

Streaming, OTT, and similar platforms are benign on their own. The behaviors of the controlling entities at media companies, which temporarily shifted towards driving success at their online platforms, were behind a lot of this worry. However, they’ve now seen that this strategy doesn’t work, whether it was Marvel’s experience with Black Widow or DCs experience with releasing their movies only via streaming that have led them back to the cinema release model. With a cinema release, the content has much more potential to acquire downstream revenue, including increased recognition for VOD, OTT, broadcast, premium/non-premium cable bundles, merchandising, toys, video games, etc. Success has proven that the cinema release model breeds value as a springboard to downstream revenue. Studies have also shown that consumer attention and content retention are more intense in the cinema.

How do you look at the competition, and what factors give Moving iMage Technologies an edge over rivals?

The platforms and product/services offerings are unique, and there is no “like for like” competition. We have strong relationships and scale with leading industry suppliers, whether Samsung, LG and Sony for screens or Christie Digital Systems and Barco for projectors. Additionally, we have nearly 50 proprietary manufactured products that differentiate us in the industry. Finally, we are introducing new, potentially disruptive technology offerings such as our CineQC SaaS platform, our MiTranslator product, and subscription service that allows audiences to watch a movie in multiple different languages in the same auditorium, and more in development.

From a project standpoint, we are the only company with national capabilities. Most of our competitors are local and regional dealers or resellers. Our advantage is that we have signed deals with growing circuits with both national and international footprints. In addition, our technical resources, people, and scale put us in a position to win the vast majority of the sales for which we compete.

What is your current strategy for becoming profitable, especially after achieving impressive revenue growth in the most recent quarter?

We are always looking for ways to improve margins and cash flow. Sometimes it is opportunistic. As I mentioned earlier, we used our balance sheet to pay off our debt and eliminate interest expense; we’ve taken advantage of pre-payment discounts and made opportunistic discounted inventory purchases.

From an ongoing profitability perspective, during 2021, we used the pandemic to lean out our manufacturing, which will help gross margins. Additionally, we have minimal variable operating expenses, so there is significant operating leverage where we likely won’t have to add resources until we start to approach $50 or $60 million in revenue. On top of this, we are continuously working to shift our mix towards higher-margin offerings. For example, since the last cycle, we added nearly 50 proprietary manufactured products and acquired the Caddy products, both of which have gross margins above 40%. Finally, we are in the early stages of ramping our emerging proprietary technology products such as the CIneQC SaaS and solutions platform, our MiTranslator AR glasses and subscription service, and digitizing the real estate on our Caddy products.

Also Read: ZeroFox CEO James Foster: IDX deal will be incrementally valuable to company, clients

What are the emerging trends in the industry for cinema production technology, and where do you see Moving iMage Technologies five years from now?

Cinema production will continue to evolve. We already see filming in 4k. From a viewing technology perspective, we are in the very early days of a revolutionary screen technology called direct-view LED. This technology from our partners Samsung, LG, and Sony eliminates the need for a projector, increases the useful life of a screen significantly, and most importantly for viewers, the image and sound quality is an order of magnitude better than today’s laser projectors. There have been less than a handful of installations in the US to date, and we’ve done them all. Right now, this is a super-premium product, but over the next several years, we expect demand to increase and costs to come down, which will drive the next technology upgrade cycle in the second half of the decade.

As for us, we believe we can be a $100 million company over the next several years driven by a number of industry tailwinds. First, is the recovery in the domestic box office. After doing over $11 billion in 2019, 2020 and 2021 were at levels likely in the $2-3 billion range. Industry analysts are predicting that with a long line of potential blockbusters in 2022, a return above $10 billion is likely and then continued growth in subsequent years.

Next, we are beginning a technology upgrade cycle for servers, screens, and projectors. These cycles typically last 4-5 years. Additionally, there are upgrades and refurbs to existing theaters as they add amenities such as breweries, bars, dine-in, restaurants, and more to attract customers. With this very strong backdrop in place, we are in the best position we’ve ever been in to benefit from these tailwinds.

Also Read: NFTs open the door for new product and revenue possibilities: Zedge CEO Jonathan Reich

From a company-specific view, we have a whole lineup of proprietary and potentially disruptive products as I mentioned previously. We also brought in a senior business development executive with over 20 years of industry experience to identify new growth opportunities via M&A, as well as to drive our new technology offerings like CineQC and MiTranslator. We also see the opportunity to offer these and other technologies to adjacent markets such as stadiums and arenas, where our Caddy business has a strong leadership position and existing relationships. We believe they will also be attractive beyond North America, which aligns with our goals to expand to Europe over the next 24 months and parts of Asia longer-term. Overall, it isn’t far-fetched for the business to grow to $100 million from less than $20 million today.