As markets return to normalcy after being hit by the pandemic for over two years, oil demand is growing amid continued rebound in mobility and improving sentiment. According to a recent survey, global oil demand would surpass pre-Covid levels by the end of 2022, which is good news for energy companies like Schlumberger Limited (NYSE: SLB)

Schlumberger, a market leader in oilfield services, recently adopted a new brand identity by rechristening itself to SLB, as part of its strategy to focus on energy innovation and decarbonization. The move would also affirm Schlumberger’s transformation from the largest oilfield services provider into a global technology company, with elevated oil prices adding to the momentum.

Bullish View

The Houston-based firm’s performance in the stock market has been impressive during the COVID era, when the broad market experienced high volatility. Interestingly, SLB has maintained an uptrend since recovering from a multi-year low in the early weeks of the pandemic. It got a boost last week following the strong third-quarter results, and continued to gain since then. Considering the favorble market environment and the company’s innovation-focused model, the stock can be a good investment.

Schlumberger Limited Q3 2022 Earnings Call Transcript

While SLB has more room to grow in the coming months, the valuation is expected to remain reasonable. Analysts overwhelmingly recommend buying the stock.

The oil company started the second half on a positive note, supported by broad-based growth across its international and offshore businesses. However, that is being partially offset by slowdown in the domestic market. Strong operating leverage and improved net pricing are acting as catalysts to the ongoing recovery. Encouraged by the tailwinds, the management has raised its full-year revenue guidance.

Innovation

The digital push is expected to enable Schlumberger to deliver higher value in terms of fiscal performance and decarbonization. Going forward, the business is poised to benefit significantly from fast-paced technology integration and accelerated activity in the industry. The lingering supply disruption and impact of geopolitical issues on the demand-supply balance indicate that the market is going to witness a sharp increase in energy investment.

From Schlumberger’s Q3 2022 earnings conference call:

“We expect investment growth will be durable, reinforced by the long-term demand trajectory, multi capacity expansion plans, lower operating breakeven price and supportive commodity prices. Growth will be simultaneous in North America and in international markets. This started first in North America market, and we are already witnessing the next phase of growth with an acceleration in pace in the offshore and international markets that was very visible in the third quarter.”

CVX Earnings: Chevron Q2 2022 profit beats estimates; revenue up 83%

Financial Performance

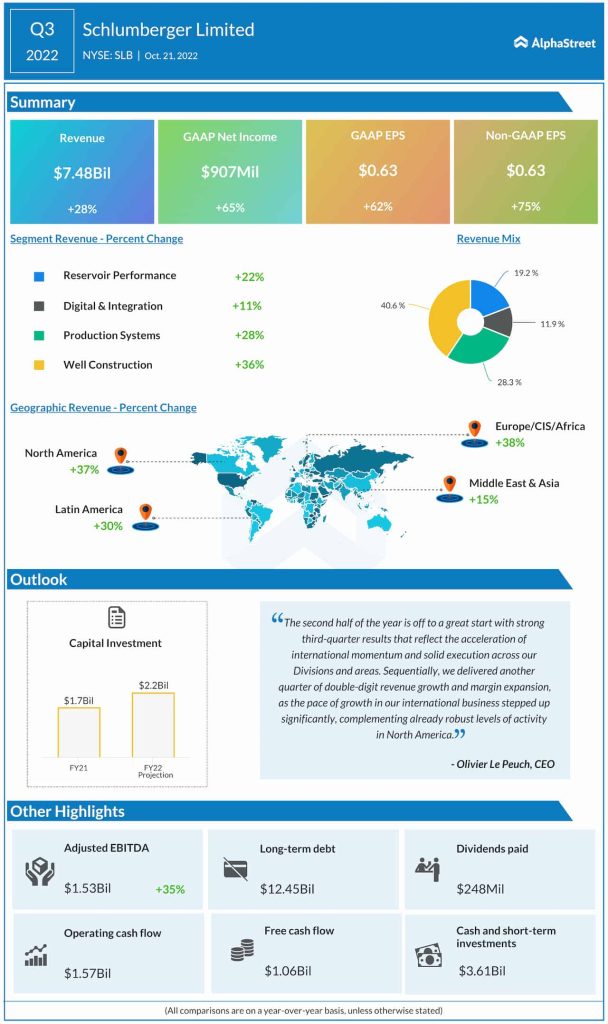

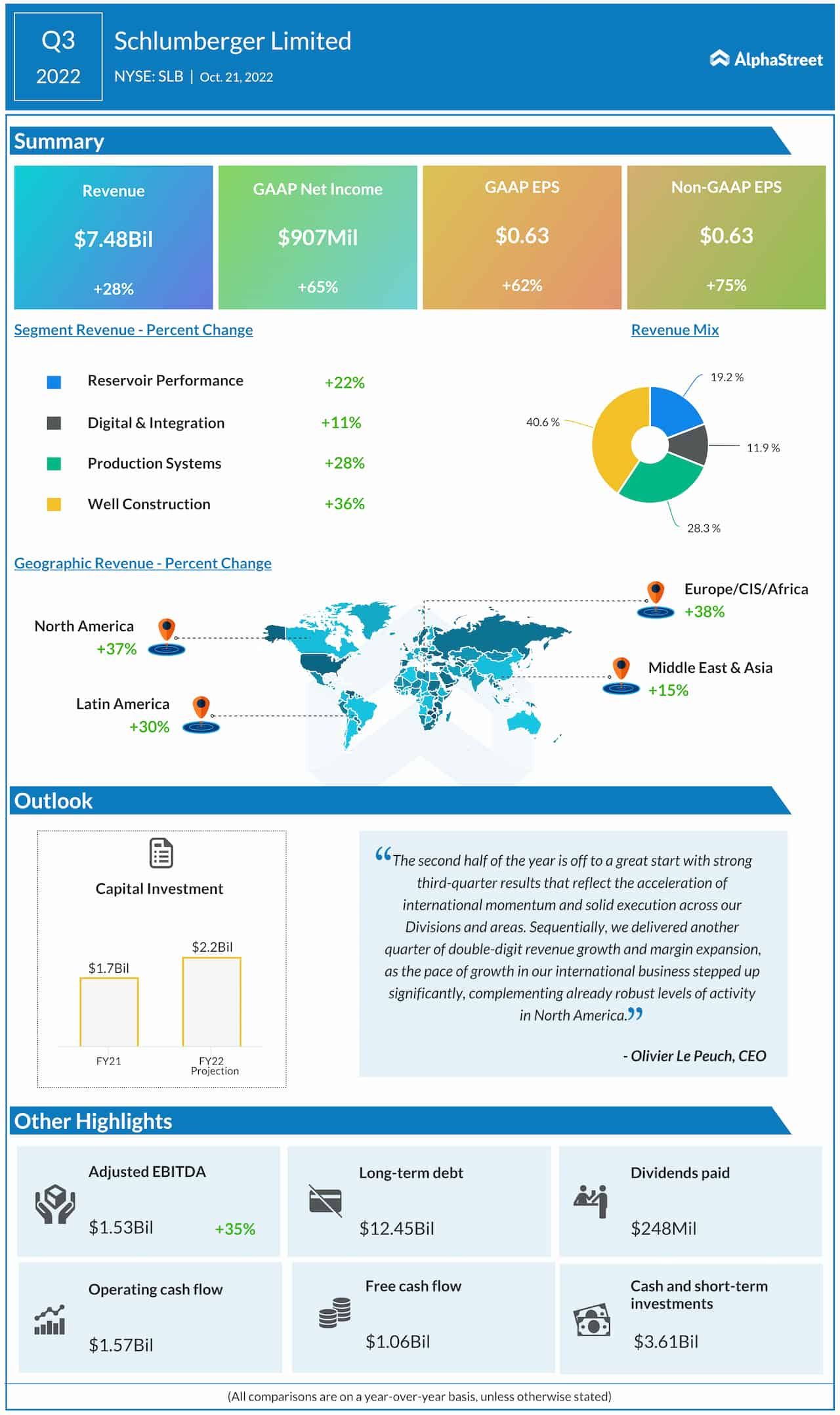

Schlumberger has maintained stable profitability over the past several years, with quarterly net income either beating or matching estimates regularly. The trend continued in the September quarter when earnings surged 75% to $0.63 per share. At $7.48 billion, revenues were up 28% year-over-year, marking the fastest growth in more than a decade. The top-line also exceeded expectations, as it did in each of the trailing three quarters.

Shares of Schlumberger traded slightly above $50 on Monday afternoon, after gaining around 3% thus far during the session. They’ve gained about 48% since the beginning of the year.