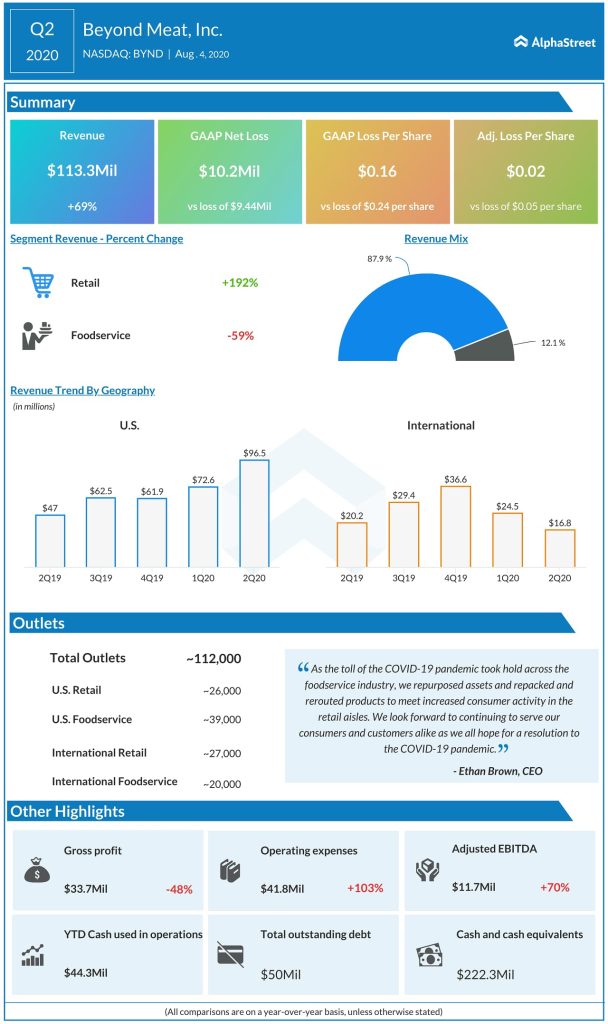

Shares of Beyond Meat Inc. (NASDAQ: BYND) have gained 150% since the beginning of this year and continue to rally, pleasing supporters. The company delivered year-over-year revenue growth of 68.5% and managed to narrow its adjusted loss per share to $0.02 during the second quarter of 2020. Revenues in the US jumped 105% versus last year with considerable strength in the retail channel.

However, not everyone is optimistic on the stock and there are questions being raised on the prospects and stability of the company and its products. Let’s take a look at whether it is sensible to join the parade right now or watch from the side lines.

Pros

First off, there is a growing preference for alternative proteins as more people move to plant-based meat products as part of vegan and vegetarian lifestyles. This is particularly prominent among the new generation and the demand for these products is expected to increase in the coming years.

A report by Research and Markets forecasts that the global plant-based meat market size by revenue is likely to cross $12 billion by 2025, growing at a CAGR of over 18% during the period from 2019-2025. Beyond Meat, as a leader in this market, stands to benefit from this situation.

Secondly, Beyond Meat has witnessed massive strength in its retail channel, particularly during the COVID-19 pandemic as declines in the foodservice channel forced the company to shift its products more towards the retail line. During the second quarter, retail net revenues grew 192% year-over-year, with US retail sales jumping 195% and international retail sales rising nearly 167%.

From the Q2 2020 transcript:

Looking at consumer takeaway in US retail, according to SPINS data, for total US multi-outlet natural and specialty channels for the 12-week period ended June 14th, 2020, sales of Beyond Meat products were up 121% year-over-year, with the velocity growth of 88% contributing to 550-basis-point increase in market share, while the plant-based meat category as a whole was up 57% year-over-year.

Thirdly, Beyond Meat is seeing increases in household penetration, average spend per household and repeat rates i.e. consumers trying its products are buying them again. According to SPINS/IRI panel data, US household penetration for the brand increased 4.9% as of June this year from 3.5% in January, reflecting a 40% spike in just five months. On a year-over-year basis, US household penetration has more than doubled.

Beyond Meat is looking to drive growth through production and distribution partnerships as well as a shift to ecommerce. In August, the company rolled out its new ecommerce site which complements its vast retail presence.

Last month, Beyond Meat signed an agreement to produce plant-based meat products in China which is expected to become a major market in the coming years. The company also broadened the distribution agreement with Walmart to include its Beyond Burger in 2,400 stores, up from the previous 800 locations. Beyond Meat products are currently available at approx. 112,000 retail and foodservice outlets.

Cons

Although Beyond Meat’s revenues have been climbing steadily, the growth rate has slowed down both on a year-over-year and sequential basis. In the second quarter of 2019, revenues surged 287% year-over-year to $67 million. This came down to just 69% growth in revenue in Q2 2020.

Looking at revenues over the past five quarters on a sequential basis, from Q2 2019 to Q3 2019 the company registered a 37% growth. From Q3 to Q4, revenues increased just 6%. In the first quarter of 2020, revenues dipped slightly and then went on to gain 16% in Q2. Beyond Meat has been unable to pick up pace despite being the market leader in this space. In the face of increasing competition, this presents a challenge for the company.

Beyond Meat’s foodservice channel was significantly impacted by the COVID-19 pandemic. During the second quarter of 2020, foodservice revenues fell 59% year-over-year. Foodservice sales in the US declined nearly 61% while international foodservice sales were down over 56%. The company expects revenues in this channel to continue to be negatively impacted by the pandemic for the remainder of this year.

Despite the popularity of plant-based meat products, the demand for traditional meat products appears to be relatively intact. In June, the global meat industry estimate stood at $1.4 trillion. It remains to be seen whether the trend of choosing plant-based products picks up or slows down due to health concerns or other reasons. This trend will definitely affect Beyond Meat’s future growth.

Stock

The majority of analysts have recommended holding the stock while some recommend Sell. Very few appear to be in favor of Buy. The 12-month average price target is $135, which reflects a 28% downside from the current price.

All in all, given the strong position of the traditional meat industry and the uncertainty currently prevalent in the market, it might be prudent to wait and watch before making a decision on this stock.

Click here to read the full transcript of Beyond Meat Q2 2020 earnings call