Shares of Snap Inc. (NYSE: SNAP) were down 12% on Wednesday, a day after the company reported its fourth quarter 2022 earnings results and provided a lacklustre guidance. Revenue was in line with expectations and earnings surpassed projections but the slow growth and dent in profits disappointed the Street. Here’s a look at the good and the bad from the Q4 report:

Slow revenue growth

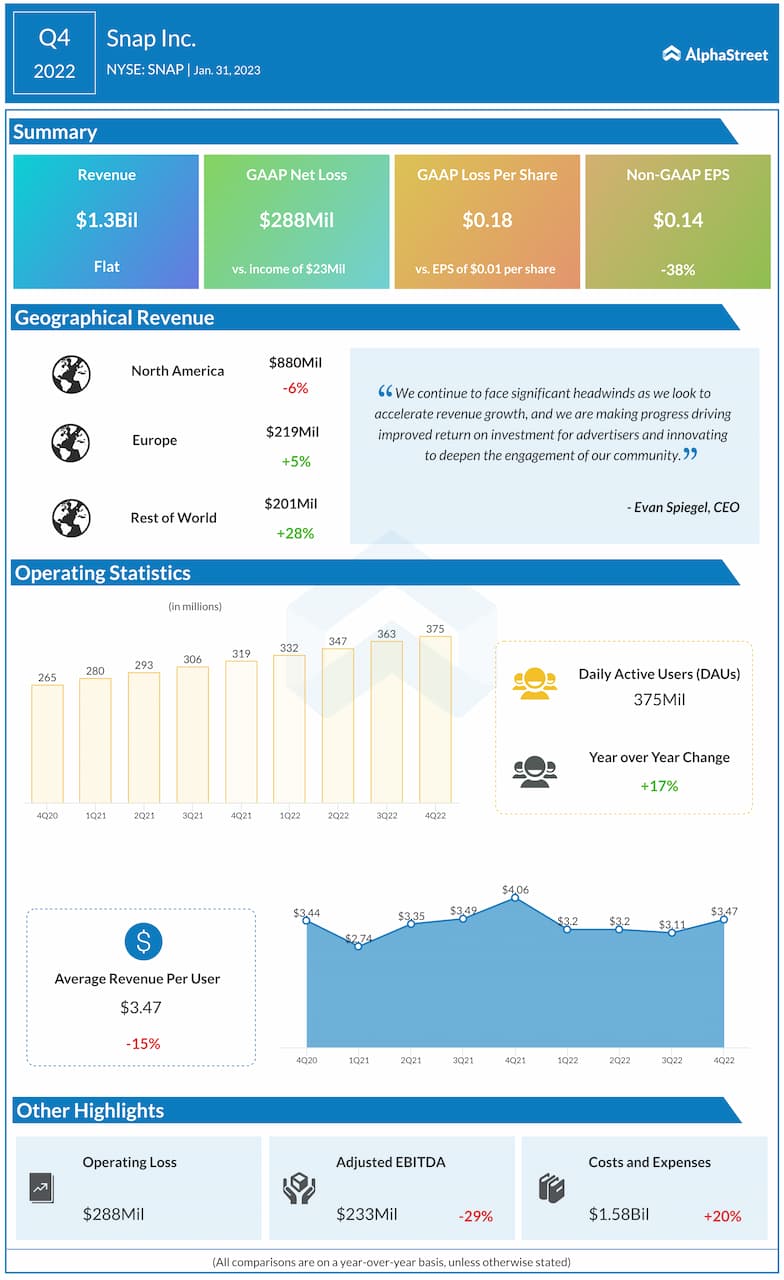

Snap reported revenues of $1.3 billion for the fourth quarter of 2022, which matched expectations but remained relatively flat compared to the year-ago period. Snap’s revenue growth has been slowing down over the past couple of quarters going from 38% in the first quarter of 2022 to 6% in the third quarter. So the lack of growth in the latest quarter did not sit well with the Street.

The revenue growth was impacted by a double-digit decline in the brand-oriented business. The company continued to face challenges in the form of macroeconomic headwinds, platform policy changes, and increased competition which created a tough operating environment. At the same time, the direct response business managed to grow 4% year-over-year as the company made progress on measurement and optimization.

Drop in profits

Snap reported adjusted EPS of $0.14 in Q4, which surpassed projections but was down 38% from the year-ago quarter. The company also posted a net loss of $288 million, or $0.18 per share, on a GAAP basis compared to a net income of $22.5 million, or $0.01 per share, in the year-ago period.

User growth

On the bright side, Snap’s daily active users (DAUs) grew 17% year-over-year to 375 million in Q4. DAUs increased both sequentially and year-over-year across all its regions. DAUs reached 100 million in North America while in Europe, they reached 92 million. Rest of World DAUs stood at 183 million and the company sees significant potential for community growth over the long term in this segment. For the first quarter of 2023, Snap expects DAUs to range between 382-384 million.

Bleak outlook

Snap did not provide guidance for the first quarter of 2023 due to the challenging operating environment and it expects the headwinds faced in Q4 to persist in Q1. On its quarterly call, the company said it has seen revenue decline 7% YoY thus far in Q1. Its internal forecast assumes revenue will decline 2% to 10% YoY in Q1.