Walgreens Boots Alliance, Inc. (NASDAQ: WBA), a market leader in retail pharmacy, has regularly revised its business model to better align with the transformation the healthcare space is witnessing. Currently, the company is working to enhance the scale and profitability of its US healthcare business by streamlining investments, with a focus on primary and multi-specialty care services.

Of late, the market has not been very kind to Walgreens’ stock, which has lost about 30% in the past twelve months. Having reversed most of the recent gains, WBA is currently trading below it 52-week average. While the stock is likely to remain volatile in the near future, growth initiatives like scaling value-based care delivery would help the company expand market share in the long term and create shareholder value.

Diversification

It is worth noting that Walgreens’ expansion drive has been successful so far, even during market uncertainties. Since the company keeps venturing into new areas, it looks set to become one of the most diversified healthcare providers a few years from now. Those looking to benefit from long-term opportunities can consider the relatively low share price as an entry point.

The company is on track to becoming a one-stop shop for all healthcare needs, from retail pharmacy to primary care and preventive care to telemedicine. The entry into the primary care space, supported by the acquisition of Summit Health, would be the key to returning to the growth path. If the company succeeds in eliciting the desired response from the market, that would definitely give it an edge.

Competition

However, the strategy would not make Walgreens immune to competition, and any misstep in execution would become an opportunity for competitors to eat into its market share. Arch-rival CVS Health Corporation (NYSE: CVS) is aggressively expanding beyond the core retail pharmacy business. But its performance, both financially and in the stock market, has not been very encouraging, lately. When it comes to Walgreens, continued weakness in annual sales performance and falling margins would be a concern for its stakeholders in the near term.

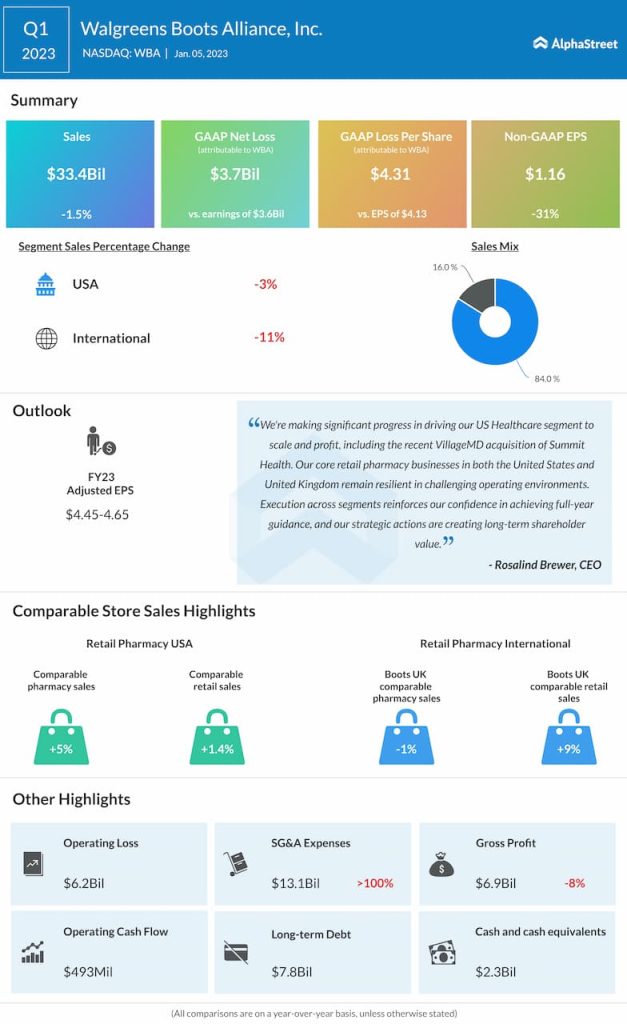

Despite uncertainties like the pandemic-related business disruption and economic slowdown, Walgreens constantly delivered stronger-than-expected quarterly earnings in recent years. The trend was maintained in the early months of fiscal 2023, though adjusted profit dropped by more than a third to $1.16 per share in the first quarter. There was a year-over-year decrease in sales in both the domestic market and overseas, and total revenues came in at $33.4 billion but exceeded estimates.

From Walgreens’ Q1 2023 earnings call:

“We are raising our sales guidance, and we have greater visibility toward the strong 8% to 10% core growth that underpins our results, offsetting the COVID headwind of 16% to 18%. We are quickly scaling U.S. healthcare with a defined path to achieve profitability exiting this fiscal year. Our strategic actions are working to create sustainable shareholder value as we reimagine local healthcare and wellness for all. We are making progress against each of our four strategic priorities. U.S.”

Q2 Report on Tap

When Walgreens reports second-quarter results on March 28 before the opening bell, the market will be looking for a double-digit year-over-year decline in adjusted earnings to $1.10 per share. The estimated weakness in bottom-line performance reflects a modest drop in revenues to $33.42 billion.

Walgreens shares opened Wednesday’s session at $33.55 and mostly traded lower during the day. The company’s market cap is slightly above $28 billion now.