Walmart Inc. (NYSE: WMT) has a good track record of navigating through market headwinds effectively. However, after the COVID-induced shopping spree ended and sales returned to normal levels, the company is now feeling the pinch of inflation and economic downturn. Like some of its peers, the big-box retailer is on a cost-cutting drive and is laying off hundreds of employees, mainly in the e-commerce division.

Walmart’s stock went through a series of ups and downs in recent months but maintained an uptrend all along. It picked momentum ahead of next week’s earnings and is trading close to the all-time highs seen more than a year ago. The value has nearly doubled in the past six months. Being a market leader with strong fundamentals, Walmart is unlikely to disappoint long-term investors.

Road Ahead

The management is anticipating a sales slowdown this year and beyond – due to cautious consumer spending amid economic uncertainties – which would in turn drag down margins. So, it is taking initiatives to boost profitability, such as heavy investments in automation and cost reduction. While delivering increased cost-efficiency and raising throughput, the measures will also help the company compete effectively with arch-rival Amazon.com. Recently, Amazon cut several jobs to beat the slowdown and enhance margins.

Cautious Outlook

Walmart will be publishing first-quarter results on May 18, before the opening bell. On average, analysts estimate that the retailer’s adjusted earnings dropped to $1.19 per share in the first three months of fiscal 2024 from $1.30 per share last year. The consensus sales forecast for the April quarter is $135.23 billion, which represents a 4.5% decline from last year. The bottom line beat estimates in the three trailing quarters.

“We’re driving a lot of change inside our company. We know where to tap the brakes on cost and inventory, but our focus is more on the gas pedal with respect to our strategic improvements related to assortment growth and our customer-member experience. We’ll keep shaping the business model by scaling our newer mutually reinforcing businesses in areas like Marketplace, fulfillment services, and advertising. It’s exciting to see our global advertising business grow to $2.7 billion for the year we just completed,” Walmart’s CEO Doug McMillon said at the last earnings call.

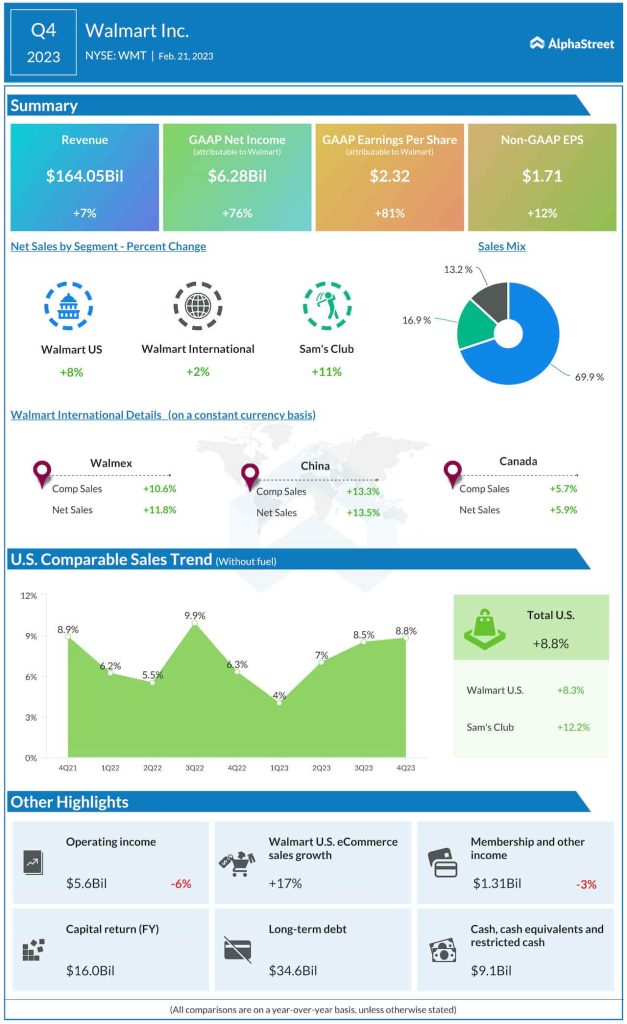

Strong End to FY23

In the fourth quarter, both revenues and adjusted earnings increased to $164.05 billion and $1.71 per share, respectively, reflecting decent gains both in the domestic and international segments as well as in Sam’s Club. Comparable sales growth accelerated for the third time in a row, and e-commerce sales moved up 17%. The positive outcome is primarily attributable to the strong holiday season.

The stock, which has been trading above the long-term average for the past few weeks, ended Friday’s session almost flat.