Electronic Arts (NASDAQ: EA) ended fiscal 2024 on a mixed note, reporting lower revenues and improved bottom-line performance for the fourth quarter. The stock declined following the announcement as earnings missed estimates and the management issued a cautious outlook. While the video game publisher maintains a strong financial trajectory with stable revenues and healthy cash flows, it faces challenges like growing competition in the gaming industry and rapidly changing customer preferences.

Electronic Arts’ stock slipped to a five-month low in mid-April, before regaining some momentum in the following sessions. The shares have lost around 6% so far this year. Considering experts’ positive outlook on the stock, EA is likely to make a strong recovery and go beyond its 2021 peak. The valuation looks favorable from an investment perspective. The company is working to tackle competition by adopting new technology and transitioning from the console-based model to include mobile and PC gaming.

AI Push

Going forward, the firm’s strategic AI integration is expected to enhance efficiency significantly. It has a promising suite of game franchises like Battlefield, Madden NFL, and EA Sports FC which have been performing well, and the trend is likely to continue. Moreover, the company is a market leader in sports video games.

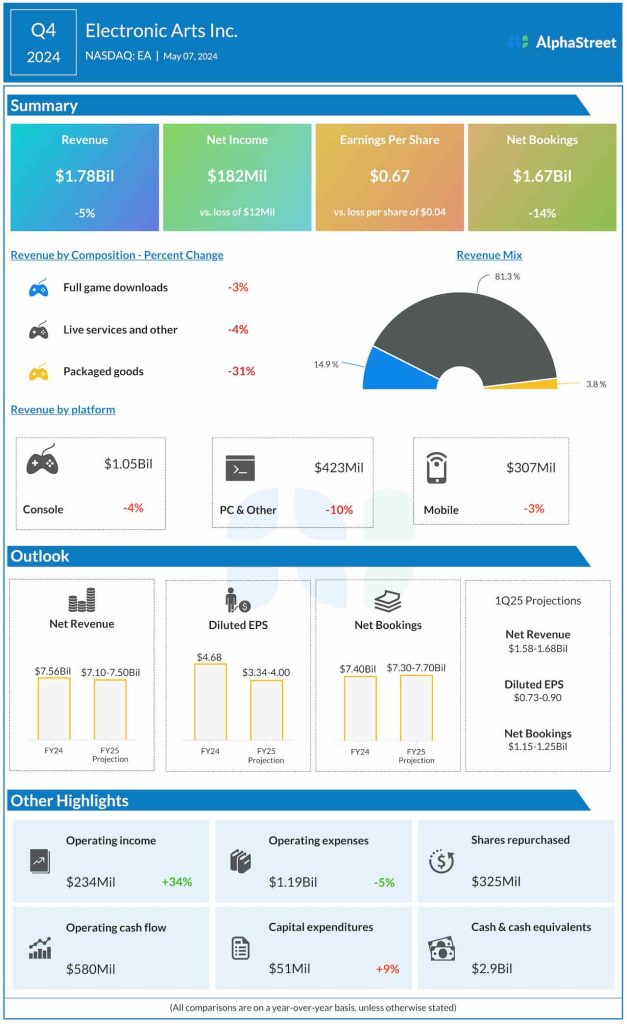

Electronic Arts reported earnings per share of $0.67 for the fourth quarter, compared to a loss of $0.04 per share in the year-ago period. Net profit was $182 million, vs. a loss of $12 million a year earlier. Revenues decreased 5% to $1.78 billion in the March quarter from $1.87 billion in the corresponding period of fiscal 2023. All three operating segments – Full Game Downloads, Live Services & Other, and Packaged Goods – contracted in Q4. The top line was broadly in line with Wall Street’s forecast, while earnings missed.

Guidance

The management issued cautious guidance for the first quarter, forecasting revenues in the range of $1.58 billion to $1.68 billion and net bookings between $1.15 billion and $1.25 billion. The Q1 earnings per share estimate is $0.73-0.90. For the whole of 2025, it expects revenues in the range of $7.10 billion to $7.50 billion, the mid-point of which is lower than the $7.56 billion reported in the prior year. Full-year profit is expected to be between $3.34 per share and $3.40 per share, compared to $4.68 per share in fiscal 2024. The forecast for FY25 net bookings is $7.30-$7.70 billion, which is slightly above the year-ago number.

“Looking ahead, we are committed to entertaining and inspiring our loyal and engaged Sims 4 fans through over 15 content updates over the coming year, while working on multiple experiences in the Sims universe to leverage user-generated content to deepen our community and expand our audience. With each immersive, action-packed season of Battlefield 2042, players have made it clear that they wanted an even deeper experience. Our teams have listened to the community, have learned valuable lessons, and are driving to the future,” said Andrew Wilson, chief executive officer of Electronic Arts, at the Q4 earnings call.

Shares of Electronic Arts traded down 3.6% on Wednesday afternoon, after opening the session higher. It continues to languish below the 52-week average.