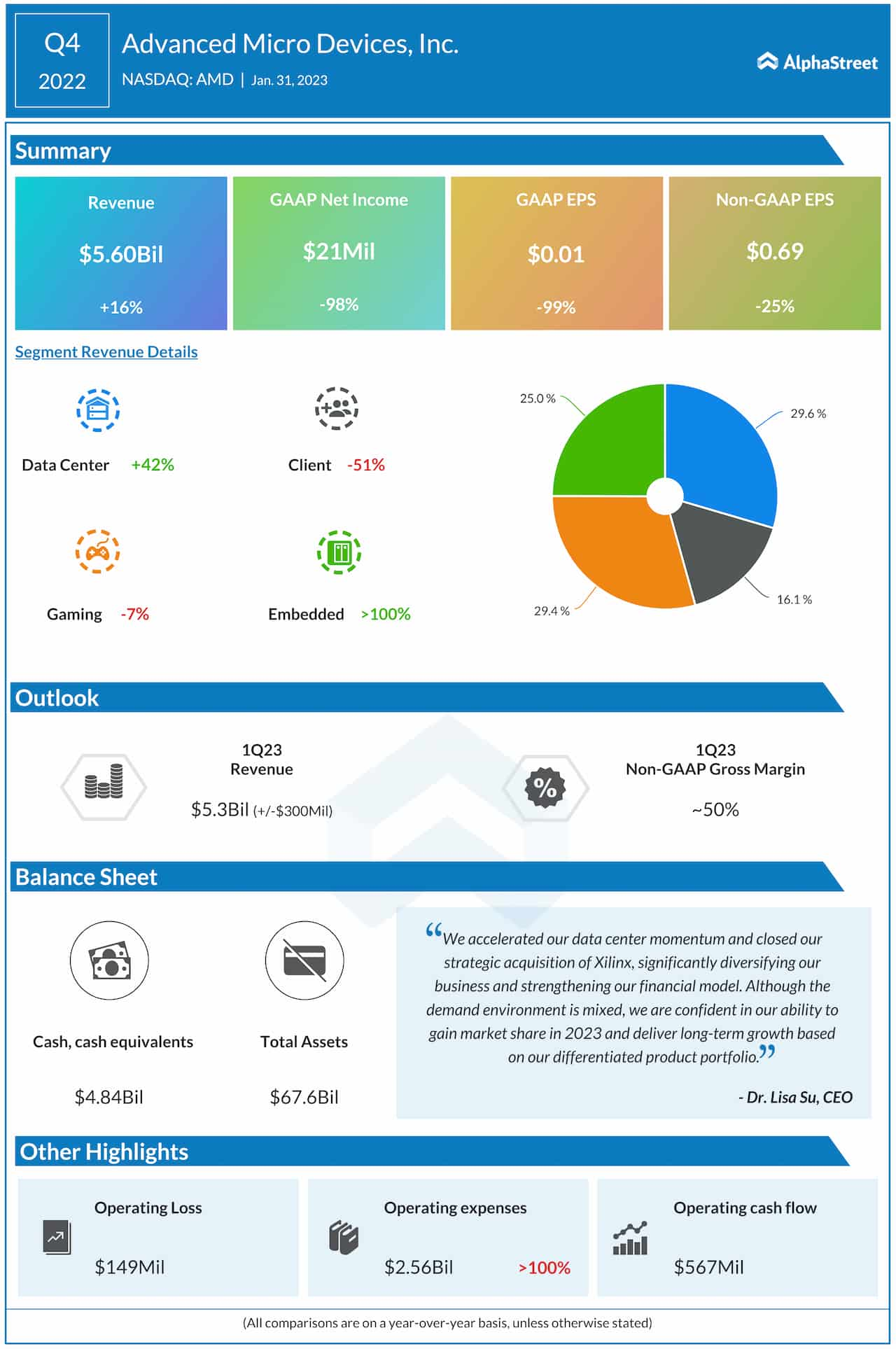

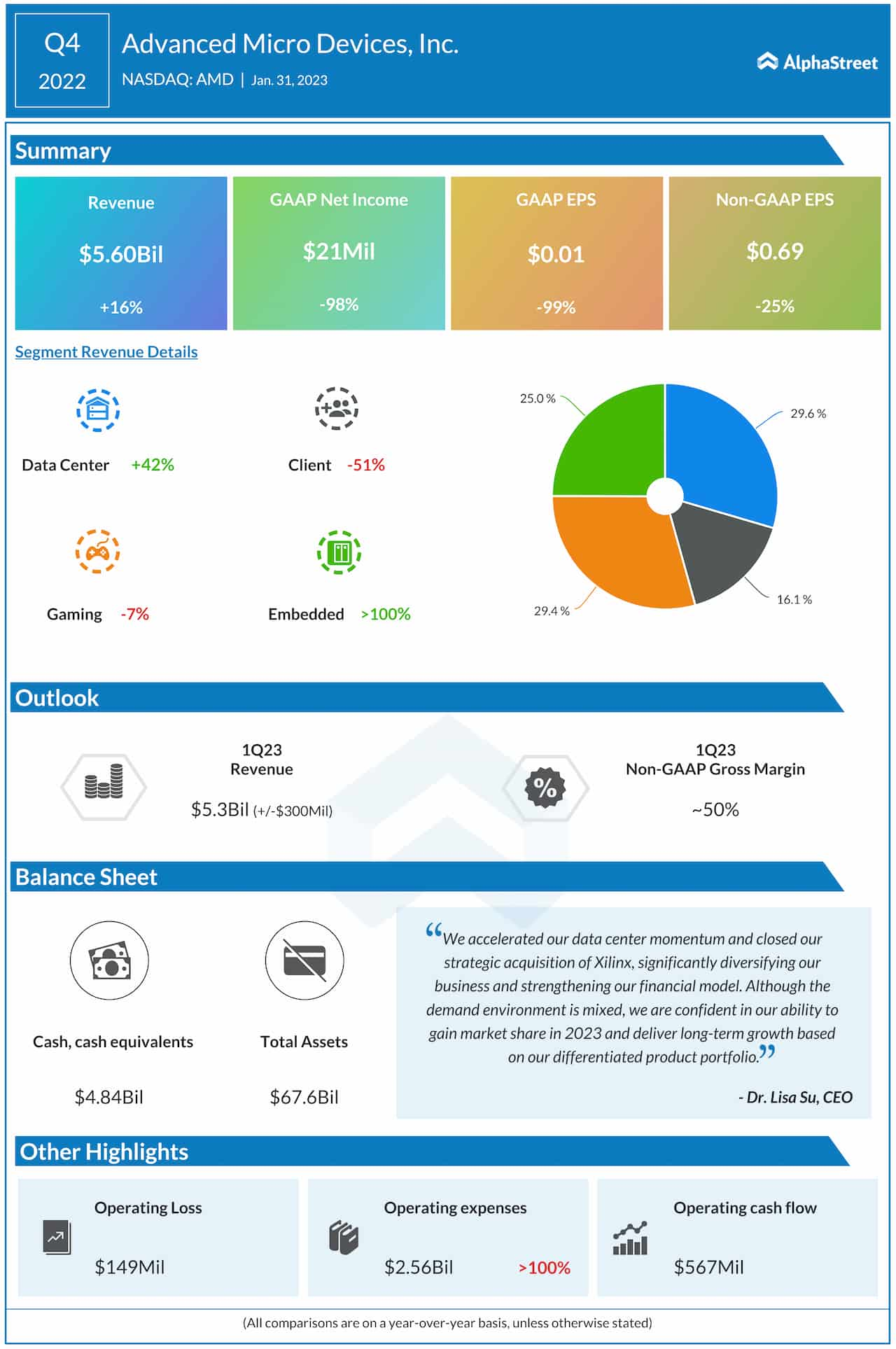

Advanced Micro Devices, Inc. (NASDAQ: AMD) this week issued a cautious outlook for the first quarter of 2023, after reporting stronger-than-expected fourth-quarter results. The chipmaker did not provide full-year guidance, citing macroeconomic uncertainties, but the stock made strong gains following the announcement.

AMD has been in a downward spiral for quite some time, except for a few short-lived recoveries in between. The company’s market value has nearly halved since peaking more than a year ago. Investors seem to have taken the management’s warning of a near-term slowdown in their stride, and responded positively to the earnings report.

The Stock

Some experts are bullish on the stock’s recovery prospects, citing the company’s resilience to the volatile demand environment and its better financial performance than competitors. That, together with the low valuation, offers a good investment opportunity that is worth considering.

Check this space to read management/analysts’ comments on quarterly reports

AMD’s adjusted earnings came in at $0.69 per share in the December quarter, down 25% from the prior-year period. The bottom line topped expectations, after missing in the previous quarter. Revenue rose sharply to $5.6 billion and exceeded expectations, as it did in almost every quarter in recent years.

Continued strong growth in the Data Center and Embedded segments — with contributions from the Xilinx business –more than offset the weak revenues performance by other divisions. The Client division, which includes PC and laptop chips, remained under pressure from the demand slowdown. This trend is estimated to have persisted in the current quarter.

Road Ahead

AMD executives warned of a 10% drop in revenues to about $5.3 billion in the current quarter, indicating the softness in demand, especially from PC and server manufacturers. Meanwhile, the company bets on its differentiated product portfolio to gain market share and deliver strong long-term growth. Adjusted operating margin is expected to be approximately 50% in the first three months of 2023.

From AMD’s Q4 2022 earnings call:

“AMD now powers more than 100 of the world’s fastest supercomputers and 15 of the top 20 most energy-efficient supercomputers in the world. To build our data center leadership, we launched our fourth gen EPYC processors this past November that delivers up to two times faster performance in the cloud, enterprise, and HPC applications, and are up to 80% more energy efficient than the competition’s most recently announced offerings. We are seeing very strong customer pull for fourth-gen EPYC CPUs, which complement our third-gen offerings with additional performance and capabilities.”

Why investors should add Nvidia stock to their watchlist

Rival chipmaker Intel Corporation (NASDAQ: INTC) last week disappointed its stakeholders with dismal numbers, reflecting the slowdown in the electronics market. Intel earned a meager 10 cents in the fourth quarter, on a per-share basis, due to a 32% fall in revenues.

Extending the post-earnings gains, AMD’s shares traded up an impressive 12% on Wednesday afternoon. The stock has gained 31% so far this year.