Investing in microcap stocks are considered to be risky; even higher so in uncertain market environments like the one we are seeing right now. So what’s the case with Biocept (NASDAQ: BIOC)?

Biocept overview

Biocept, a cancer diagnostics and research company, was founded 23 years ago and became a public company in 2014. Biocept develops and commercializes proprietary circulating tumor cell (CTC) and circulating tumor DNA (ctDNA) assays using a standard blood sample. The company generates revenues by:

- Providing laboratory services to medical oncologists, surgical oncologists, urologists, pulmonologists, pathologists and other physicians

- Providing laboratory services to pharmaceutical and biopharmaceutical companies, which are developing cancer treatment drugs

- Licensing and/or selling its proprietary testing and/or technologies to partners in the US and abroad

Recent financial performance

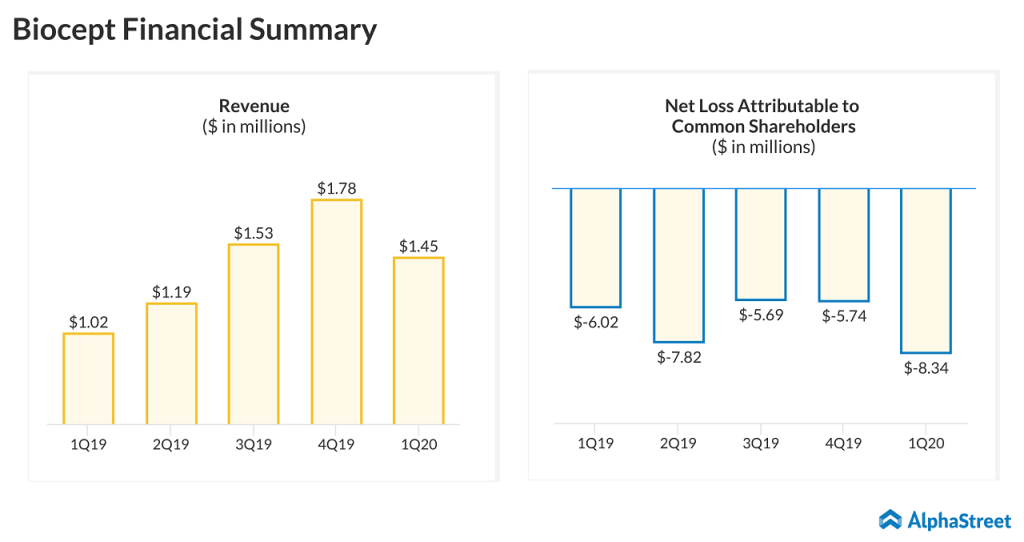

The San Diego, California-based biotech firm posted net losses of $24.6 million in fiscal 2018 and $25.1 million in fiscal 2019. Revenue surged 70% year-over-year to $5.53 million in fiscal 2019. For the first quarter ended March 31, 2020, net loss attributable to common shareholders widened to $8.34 million from $6.02 million in the prior-year quarter.

NASDAQ compliance

From its 52-week high of $1.15 achieved last July, BIOC stock fell below $1 mark in the following month and continued to trade below $1. In September 2019, Biocept received a notification from NASDAQ for not complying with the minimum closing bid price of $1. In March 2020, the molecular oncology diagnostic company received a 180-day extension from NASDAQ to regain the compliance.

Also read: Biocept Inc. (BIOC) Q2 2020 Earnings Call Transcript

After the one-for-thirty reverse stock split in July 2018, Biocept has planned to seek shareholder approval again for its reverse stock split in a reconvened virtual Annual Meeting on July 31, 2020.

Expenses

Biocept anticipates R&D expenses to remain consistent in the near-term and costs related to collaborations with research and academic institutions to increase. Sales and marketing expenses are expected to increase as the company works on generating higher revenues and marketing additional offerings. General and administrative expenses are also expected to increase as Biocept expands its business operations.

Also read: Biocept (BIOC) revenue drops 23% in Q2 2020; loss narrows

COVID-19 testing

In late June, Biocept announced the availability of 10,000 oropharyngeal specimen collection kits for COVID-19 testing. In an email communication with AlphaStreet, the company spokesperson said its too early to provide daily average testing numbers, as its been only a few weeks that COVID-19 testing kits became available.

The company spokesman added,

“Securing specimen collection kits to conduct COVID-19 testing has been challenging both for Biocept and other providers. We are working towards offering Biocept-developed specimen collection kits while making available kits with parts Biocept assembles from another provider. We expect our proprietary Biocept-developed COVID-19 collection kits to be available in the third quarter of 2020.”

The global outbreak of the COVID-19 continues to rapidly evolve, and the effect of COVID-19 will depend on the future developments. While Biocept receives specimens from clients on a daily basis, it anticipates a potential slowdown in volume as many clinic visits are being re-scheduled and delayed.

Final verdict

As of March 31, 2020, Biocept had $21.5 million in cash and an accumulated deficit of $254.1 million. While the company is currently in the commercialization stage of operations, it has not yet achieved profitability and anticipates net losses and negative cash flows from operations to continue for the foreseeable future. As revenues grow, sales and marketing and R&D expenses are estimated to continue to grow, albeit at a slower rate. The company needs to generate significant growth in revenues to achieve and sustain income from operations.

Two analysts have recommended buying BIOC stock with a price target of $1.53. Shares of Biocept have given a positive return of about 140% since the beginning of this year. Despite COVID-19 pandemic disrupting Biocept’s business in many ways, it had also given some benefits. With the expected increase in COVID-19 testing capabilities in the third quarter, Biocept is expected to perform better in the rest of 2020. Yet, the continuous losses and higher cash burn remain headwinds for the company.

DISCLAIMER: This article does not necessarily imply the views of AlphaStreet, and contains opinions of the author alone.