The mass adoption of internet-based shopping has prompted store-based retailers to develop online channels to serve customers remotely, and eCommerce players to further enhance their digital prowess. Alibaba Group Holding Limited (NYSE: BABA), the China-based e-tailer with a significant global presence, is a beneficiary of the digital shift but it seems not everything is going well with the e-commerce platform.

Like most of its peers, Alibaba has been at the receiving end of the crackdown launched by the Chinese government on large technology companies. The regulatory restrictions and bleak sentiment are having a negative impact on the business – in the most recent quarter, revenue growth slowed the most in one-and-half years. Sales are also affected by growing competition and falling consumption in the core domestic market, where macroeconomic issues like the real estate crash and resurgence of COVID-19 infections weigh on consumer sentiment.

Read management’s comments on Alibaba’s Q3 2022 earnings

Stock Performance

Of late, investors have not been kind to BABA, which lost around 85% in the past twelve months. But it might not be a good idea to buy the dip, considering the lingering uncertainty, though some analysts are bullish on the stock’s near-term prospects.

Going ahead, China’s digital industry would remain under strict scrutiny as regulators seek to bring order by taking measures to safeguard user rights and ensure data security. That would clip the wings of tech majors like Alibaba and Tencent in the foreseeable future. However, the management’s efforts to sustain market share through growth initiatives like strategic acquisitions are expected to offset the impact of the headwinds to some extent. Currently, the company is reinvesting in the business with a focus on high-growth areas like cloud computing.

From Alibaba’s Q3 2022 earnings conference call:

“In cloud computing in better intelligence, we will strengthen our market leadership by further enhancing our core product and technology capability. No matter the challenges in the current macroeconomic environment and with more and more players entering into the industry, we remain very confident in our business strategy and our future. We will continue to focus on capacity building, value creation, and a multi-engine approach to growth. We firmly believe our strategy and the perseverance will bring mid and long-term returns to our customers and investors.”

Q2 Results

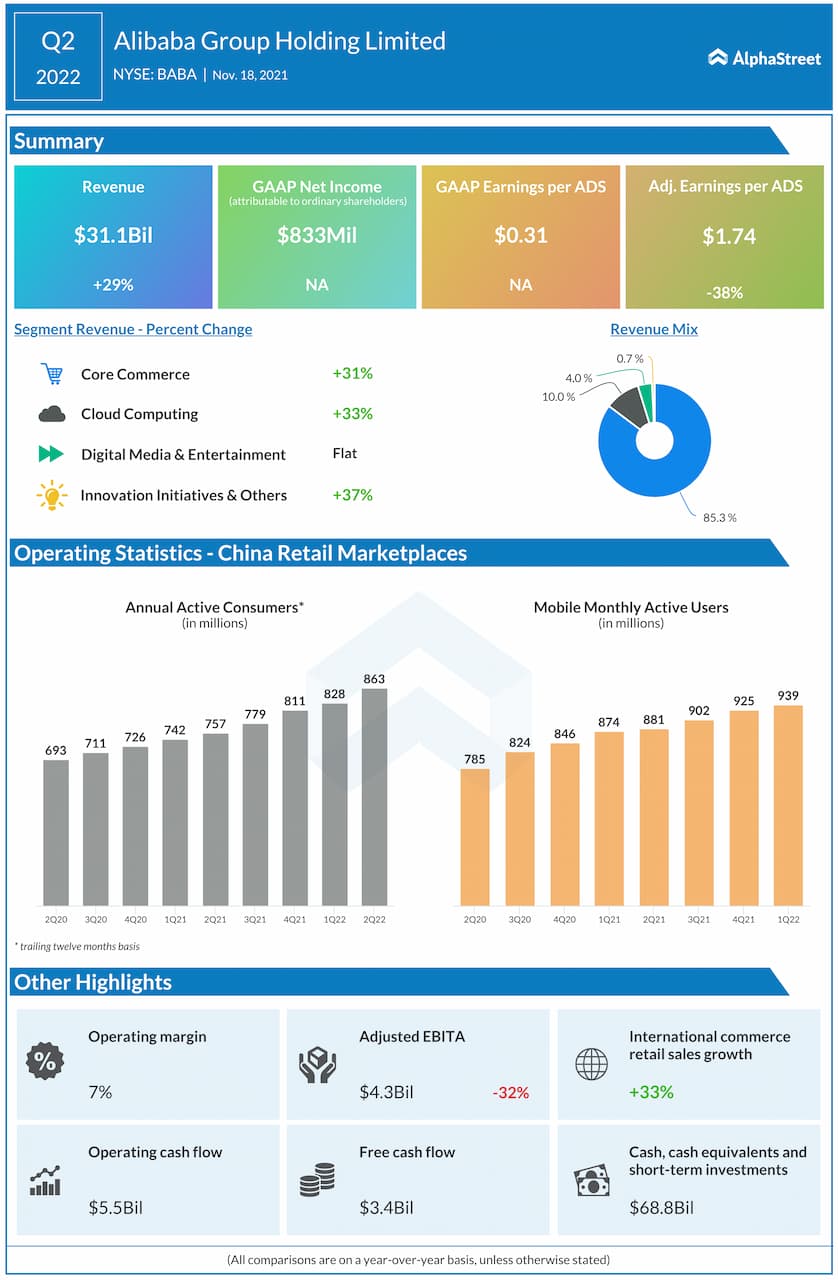

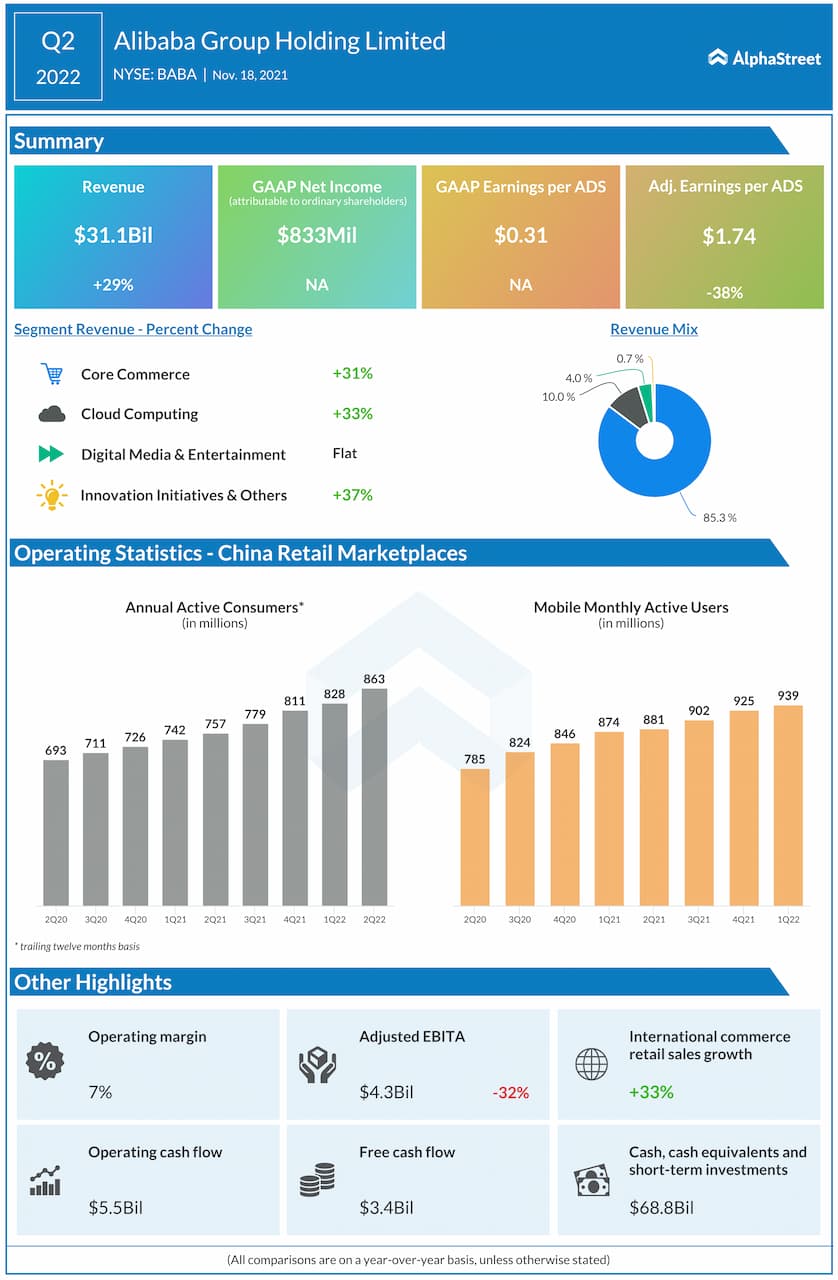

In the second quarter of 2022, the bottom-line performance fell short of expectations, with adjusted earnings falling 35% to $1.74 per share. On the other hand, revenues moved up 29% year-over-year to $31.1 billion but still came in below analysts’ forecast. Adding to investors’ concerns, the management issued annual revenue outlook that missed estimates.

On the positive side, the company added around 62 million new customers during the quarter, raising the total number to around 1.24 billion, which complements the management’s long-term target of reaching 2 billion customers globally. The third-quarter earnings release is due on February 24, before the opening bell.

AMZN Earnings: All you need to know about Amazon’s Q4 2021 earnings results

BABA traded lower on Friday at the New York Stock Exchange, after closing the previous session down 1%. The stock, which has been on a losing streak for quite some time, stabilized in recent weeks.