After suffering one of the worst setbacks in its history the airline industry is probably limping back to normalcy, with travel demand picking up and the authorities relaxing COVID-related restrictions. JetBlue Airways Corporation (NASDAQ: JBLU) is currently busy preparing for the recovery, supported by its low-cost model and growth initiatives.

Spreading Wings

The management is quite bullish on the plan to start services to Europe this summer, offering cheaper flights operated by the company’s typical narrow-bodied aircraft. Meanwhile, the proposal for revenue/code-sharing partnership with American Airlines (AAL) got approval from the Department of Transportation recently. Those initiatives are expected to open new revenue streams for the company, at a time when it is most needed.

JetBlue reported loss for every quarter last year as passenger traffic slipped to historical lows after the virus outbreak. Encouragingly, loss narrowed sequentially in recent quarters and beat the market’s prediction. Shares of the airline plunged to a six-year low a year ago but bounced back quickly and stayed on the recovery path since then. The stock returned to the pre-COVID levels this month after entering 2021on an upbeat note. The recovery can be linked to the government’s stimulus bill and improvement in traffic.

Rough Road Ahead

However, continued stress on margins and choppy bookings will weigh on profitability in the foreseeable future, given the lingering market uncertainty and slugging economic recovery. Though demand has improved since the early weeks of the pandemic, it would be a long time before traffic returns to the pre-COVID levels. Meanwhile, the reduction in cash burn has been a bright spot for JetBlue.

Read management/analysts’ comments on JetBlue’s Q4 earnings

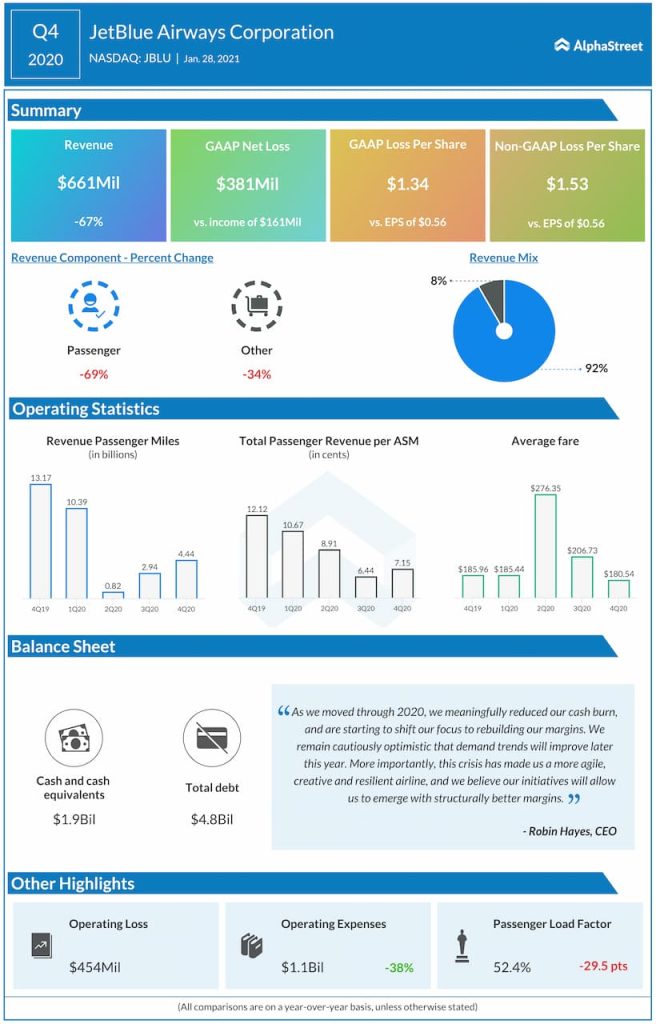

From JetBlue’s Q4 2020 earnings conference call:

“We continue on our path to recovery, which consists of three steps: first, reducing our cash burn, second, rebuilding our margins; and third, repairing our balance sheet. As we moved through 2020 and meaningfully reduced our cash burn, and we are now starting to shift our focus to rebuilding our margins. We remain cautiously optimistic that demand trends will improve later this year. More importantly, this crisis has made us a more agile, creative, and resilient airline. And we believe our initiatives will allow us to emerge with structurally better margins.”

Poor Show

In the final three months of fiscal 2020, a 69% fall in passenger traffic dragged down revenues to a dismal $661 million. While that translated into an adjusted loss of $1.53 per share, revenue passenger miles decreased at a slower pace than in the prior quarter and came in at 4.44 billion. Interestingly, both revenues and the bottom-line beat the Street view.

JetBlue’s stock has gained 47% since the beginning of 2021 and crossed the $20-mark for the first time since the virus outbreak, outperforming the sector and the broad market. The shares closed Tuesday’s regular session sharply lower, paring a part of their recent gains.