KB Home (NYSE: KBH) has been expanding its presence beyond the key markets lately, while also diversifying homebuilding operations by offering highly customized options to customers. The downturn in the US housing market had a negative impact on the homebuilder last year, but it entered 2023 on an optimistic note.

The company has been able to tackle the difficult selling conditions to some extent with stable deliveries and healthy margins, leveraging the large backlog. KB Home’s stock got a major boost post last week’s earnings and is once again trading above $40.00. Despite the relatively low price, the valuation is high when compared with the long-term earnings performance and considering the cautious business outlook. When it comes to investing, it would be a good idea to keep an eye on the stock and wait patiently for a good entry point.

Risks

The primary challenge facing the company is the rising mortgage rates, at a time when the economy is feared to be on the brink of a recession. With high inflation and stressed personal finances affecting people’s propensity to make major investments, home sales might remain under pressure in the near future. Also, the lingering supply chain issues would result in a shortage of raw materials and slow down activities.

From KB Home’s Q1 2023 earnings call:

“While supply chain disruptions will likely continue at some level for the foreseeable future with ongoing shortages and flooring, heating and cooling materials and insulation, we are encouraged by the improvements we are seeing in many areas, which we believe will provide greater predictability for our business and for our customers. Another critical area of focus of our operations is driving direct cost reductions.”

Though KB Home has relatively low debt, total liabilities are significantly higher than the cash balance plus total receivables. The deficit, in relation to the company’s market capitalization, does not look good.

That said, cash flows have remained stable, prompting the management to continue its share buyback program to reward shareholders with decent returns going forward. In a sign that the market is stabilizing after last year’s crisis, data released by the government recently showed that US home sales increased unexpectedly in February. Taking a cue from the positive shift in sales trends, the management has exuded confidence in the company’s prospects for the remainder of the year and predicts stable sales and pricing. Going forward, the gross margin is forecast to stay above 20%.

Key Numbers

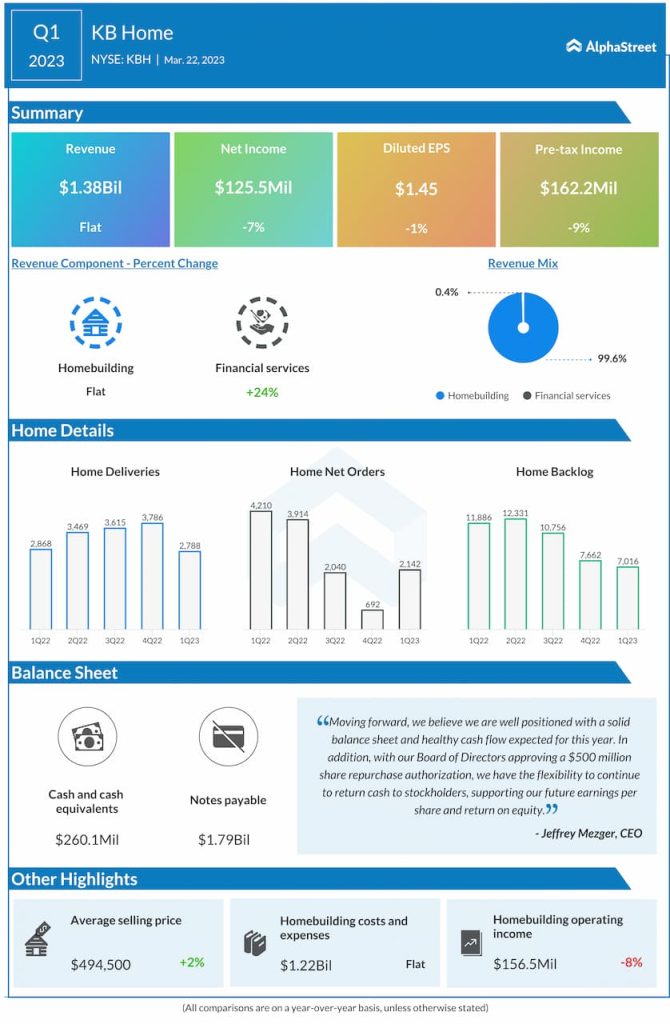

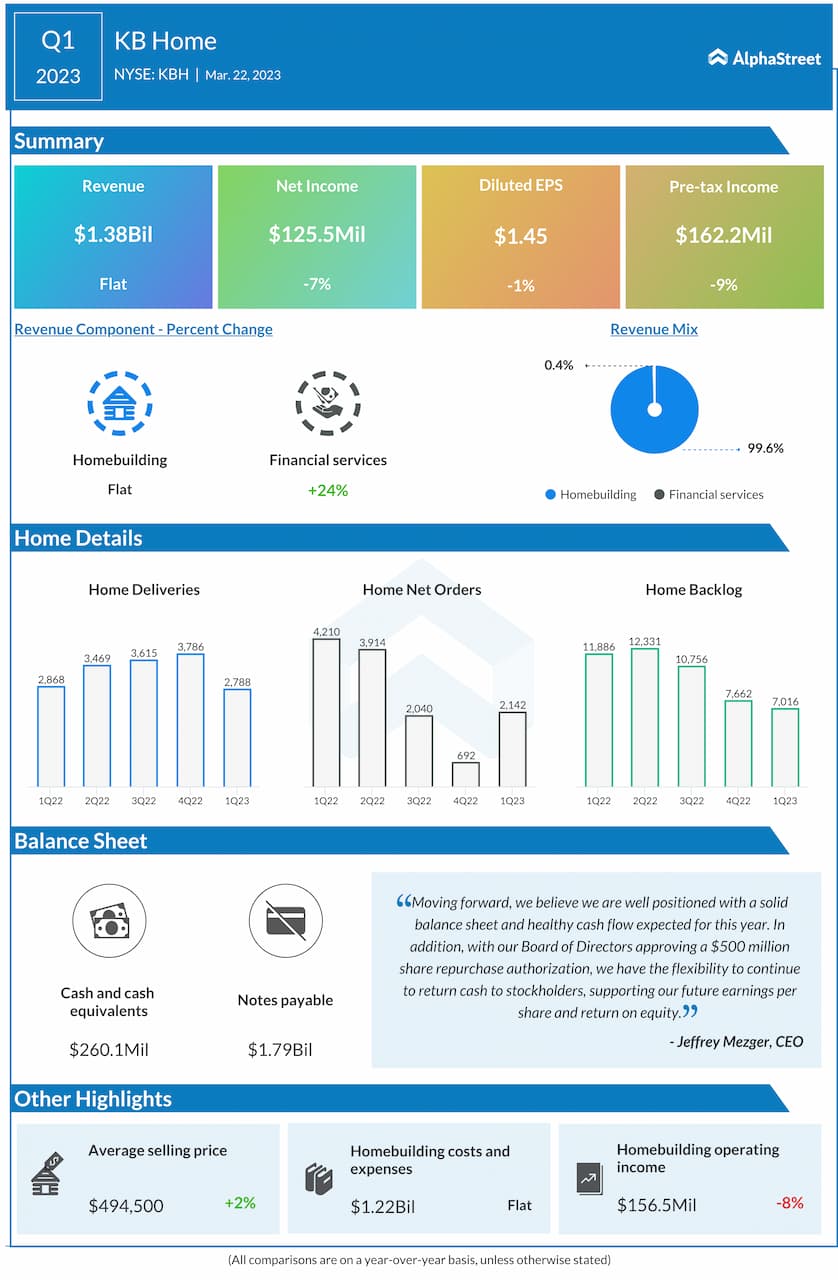

In the first three months of fiscal 2023, earnings beat the estimates after missing in the previous quarter, while revenues missed for the third time in a row. The homebuilding segment, which accounts for about 99% of total revenues, remained unchanged at around $1.38 billion. Earnings dropped modestly by 1% to $1.45 per share. While homebuilding costs remained flat, the average selling price rose by 2%.

Extending the post-earnings momentum, KBH opened the week higher and traded mixed in the early hours of Monday’s session. The current price is about half the record highs the stock had reached nearly two decades ago.