The record growth in Chewy’s (NYSE: CHWY) market value in the past few weeks shows that the demand for pet care services was not hampered by the virus outbreak. In a surprise rally, the stock climbed to an all-time high this week though the momentum waned slightly following the April-quarter earnings.

[irp posts=”63790″]

Chewy is well-positioned to tap the stable demand condition, thanks to the digital-only business model that helped the company serve customers effectively in unfavorable market conditions. Data shows that, overall, online retailers performed much better during the crisis period than their brick-and-mortar counterparts. On the flip side, freight-related delays and supply-chain issues might pose challenges to both store operators and online retailers for some time.

“We’ve needed the agility of a sprint and the stamina of a marathon as we have come into this and as we come out of it. We have continued to innovate on our customers as we have, and we will continue to do so. We are focused appropriately in making sure that priorities that hit growth profitability and customer experience are top of mind for us.”

Sumit Singh, chief executive officer of Chewy

In a way, the pandemic was a blessing in disguise for the company as a higher number of pet owners visited the online platform due to the shelter-in-place orders. Though Chewy launched gift cards to attract customers during the quarter, the offer might not be is sustainable at a time when the company needs to preserve margins. The bottom-line remains under pressure from heavy spending on logistics and fulfillment centers for improving customer experience.

Cash Balance

Overall, elevated capital spending weighs on liquidity, and the company recorded a negative free cash flow in the most recent quarter. The trend is expected to extend into the second quarter amid continuing cost pressure, mainly related to marketing and publicity, which will be partially offset by a moderation in customer acquisition costs due to an uptick in organic traffic.

While the management predicts that the new shopping habit is going to stay here, the ramped-up advertising campaign underscores the need for incremental spending to retain the new customers.

Growth Drivers

An encouraging trend associated with the change in customer behavior is a steady growth in the number of active users during the COVID period, with most of the existing customers creating bigger baskets with a higher mix of consumables. Also, there is high optimism that the new wave of pet adoptions would add to revenue growth going forward.

Responding to a question at the post-earnings conference call, the executives said they would focus on leveraging the rapid increase in average pet spending in the domestic market and the pandemic-induced digital adoption while maintaining their international strategy.

Turnaround Hopes

Nearly a year after going public, the current focus of the pet food company is on coming out of the losing spree and turning profitable. For that, the positive sales performance and rapid customer growth need to be complemented by effective cost-reduction measures. The progressive improvement in bottom-line performance in recent quarters shows that the company is on the path to a turnaround. The bullish sentiment is evident in analysts’ consensus rating on the stock, with the majority favoring buy.

Loss Widens

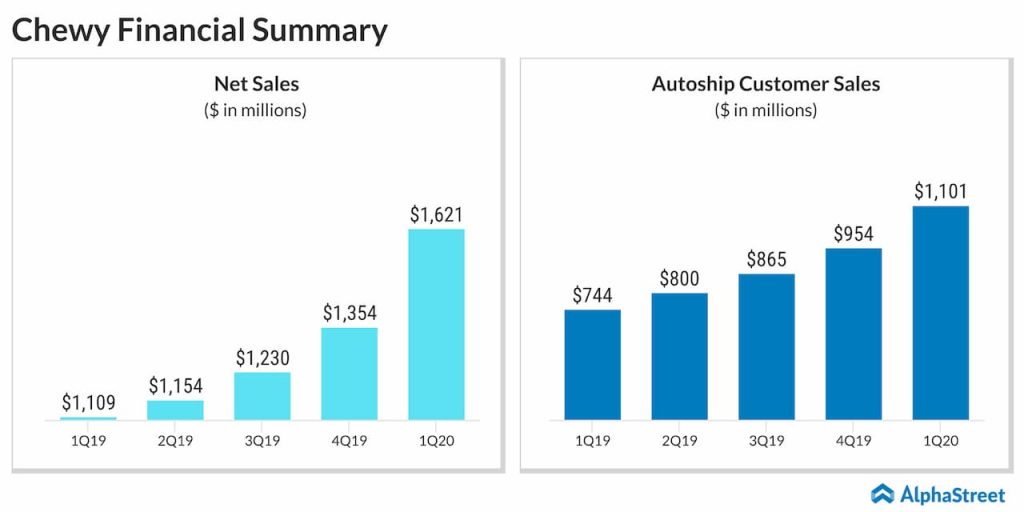

In the first quarter, net loss widened to $0.12 per share from $0.08 per share last year, despite a 47% surge in revenues to $1.62 billion. The results, meanwhile, topped the Street view. It seems the management is pretty confident about the long-term prospects and predicts double-digit sales growth for the current quarter and fiscal 2020.

“Our sales momentum, combined with the marketing efficiencies more than offset incremental COVID-related costs in the quarter, leading to positive adjusted EBITDA. We believe that the volume-related cost pressures are temporary and we expect those to moderate as we look ahead. We further believe this combination of scaled revenues and cost discipline will accelerate us along our path of sustainable profitability,” said CEO Sumit Singh.

[irp posts=”63742″]

Unlike most

Wall Street firms, Chewy witnessed a steady increase in its stock value since

early March, after dropping modestly due to the COVID-related disruption. The

shares, which gained about 72% since the beginning of the year and 45% in the

past twelve months, pulled back slightly this week following the company’s

not-so-impressive quarterly report.