DocuSign, Inc. (NASDAQ: DOCU) has long been a dominant player in the e-signature market, but it entered a rough patch after growth slowed in recent years due to competition and macro uncertainties. The company is working to reduce its dependency on the core e-signature business by diversifying into new areas.

DocuSign’s stock is currently trading at a 3-month low, but its price is still above the 12-month average. DOCU is yet to recover after withdrawing from an all-time high in September 2021. The value has declined manyfold since then.

Estimates

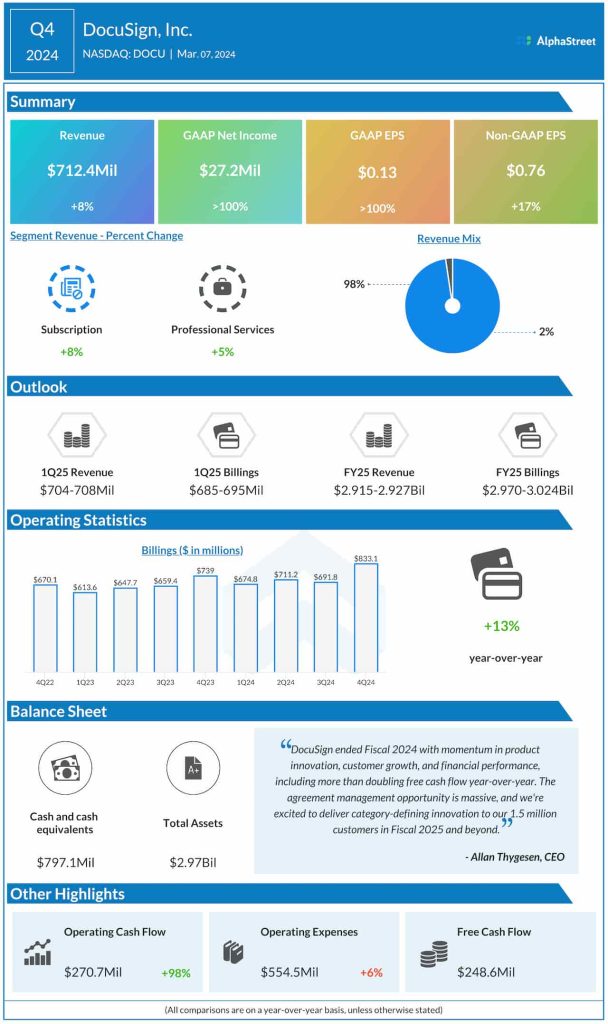

The tech firm’s first-quarter 2025 report is slated for release on Thursday, June 6, at 4:05 pm ET. On average, analysts estimate that Q1 revenues increased to $707.46 million from $661.4 million last year. The forecast comes at the higher end of the management’s top-line projection of $704-708 million. The consensus earnings estimate is $0.79 per share, on an adjusted basis, which is higher than $0.72 per share reported in Q1 2024.

Recently, the DocuSign leadership said it expects first-quarter billings to be between $685 million and $695 million. For the full fiscal year, the company forecasts revenues in the range of $2.915 billion to $2.927 billion, and billings between $2.970 billion and $3.024 billion.

These days, the company’s core business faces stiff competition from both startups and established players like Dropbox, underscoring the need to revisit the business model. Currently, a key priority for the leadership is to grow the contract lifecycle management business. DocuSign’s Agreement Cloud platform is designed for contract creation, collaboration, workflow automation, contract management, and e-signature analytics.

Performance

While the company witnessed a surge in customer numbers and high demand for its services during the pandemic — due to the movement restrictions — the momentum waned in the post-pandemic era. However, the business has become more efficient in terms of margin performance and cash flow generation. In fiscal 2024, the company’s free cash flow more than doubled annually.

From DocuSign’s Q4 2024 earnings call:

“The opportunity in front of DocuSign remains massive. Today’s world runs on agreements, but agreement processes haven’t changed in the last 100 years. Even with the evolution to digital documents, agreements and how we use their insights remain relics of antiquated paper-based systems. Sign a document stored as a flat file preserved, but disconnected from the systems that run your operations. Our sole focus is transforming those systems for our 1.5 million existing customers to make agreements more valuable for enterprises and SMBs alike.”

Q4 Outcome

In the final three months of 2024, the core subscription revenue grew 8% annually, driving up total revenues to a stronger-than-expected $712.4 million. That translated into a 17% rise in adjusted earnings to $0.76 per share. The bottom line topped expectations, as it has done consistently since Q2 2023. On an unadjusted basis, Q4 profit more than doubled to $27.2 million or $0.13 per share.

Shares of DocuSign traded down 3% on Monday afternoon, continuing the recent downtrend. They have lost around 24% in the past 30 days.