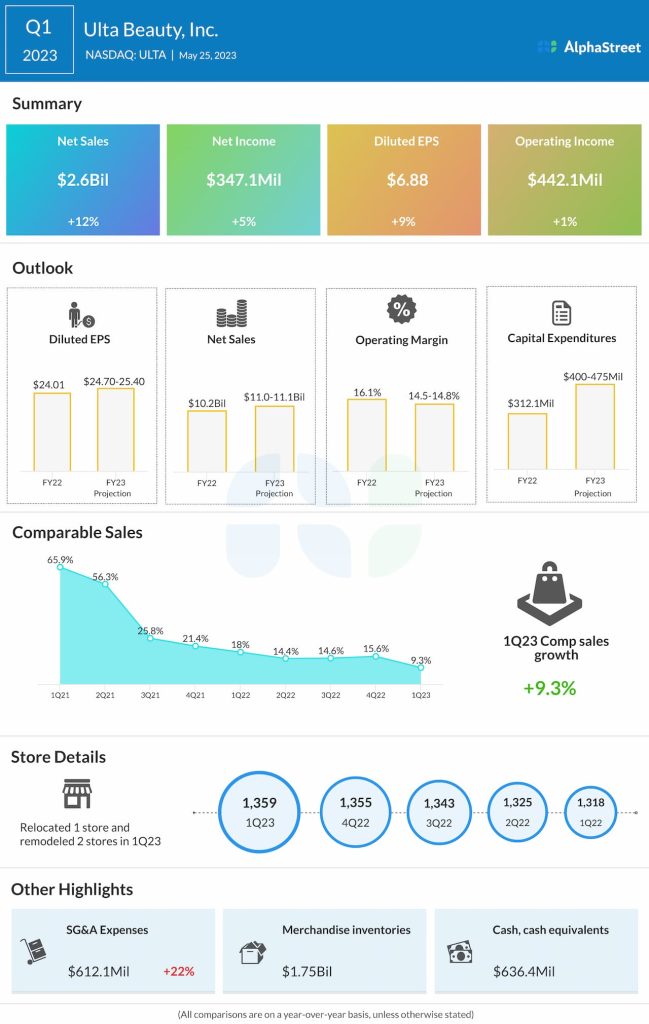

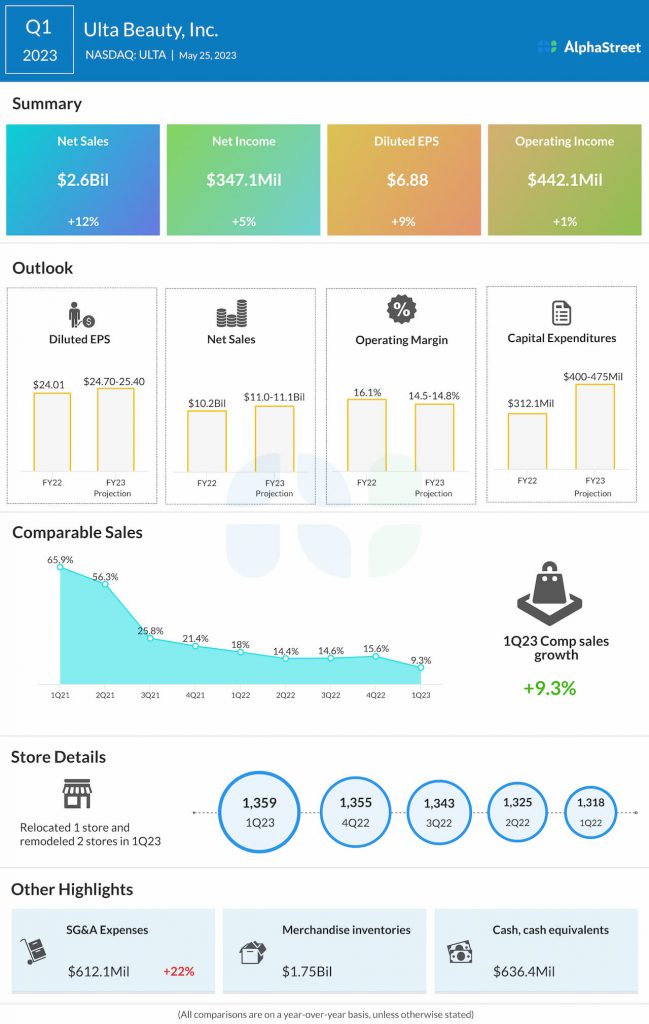

Shares of Ulta Beauty, Inc. (NASDAQ: ULTA) stayed green on Monday. The stock has dropped 9% year-to-date and 17% over the past three months. The beauty retailer delivered sales and profit growth for its most recent quarter but its margins remain under pressure. Despite this, the sentiment around the stock appears to be positive based on optimism over the long-term prospects of the company. Here are a few points to keep in mind if you have an eye on this one:

Sales growth

Ulta Beauty continues to see sales growth. Its net sales increased over 12% year-over-year to $2.6 billion in the first quarter of 2023. The top line performance was driven by comparable sales growth, strong performance by new stores, and growth in other revenue.

Comparable sales increased 9.3% in the quarter, driven by double-digit growth in store traffic and transactions, which more than offset a drop in average ticket. Comp sales also benefited from product price increases.

As stated on the company’s quarterly conference call, the beauty industry is not immune to macroeconomic challenges but it has shown more resilience than other discretionary categories as beauty is seen as a form of self-care and wellness. Even against an inflationary backdrop, Ulta Beauty is seeing customers continue to spend on beauty products which points to the prioritization of self-care.

The company has been seeing sales in its mass category grow faster than sales in its prestige categories. This could either be due to increased consumer price sensitivity or due to brand preference. Due to its wide range of price points, Ulta Beauty is well-positioned to capture consumer shifts within price points.

During the first quarter, the company saw growth across most of its segments. Its efforts in enhancing its assortment as well as expanding its footprint through partnerships are paying off.

Profitability

In Q1 2023, Ulta Beauty delivered earnings of $6.88 per share, which was up 9% from the same period a year ago. Gross profit increased 12% to $1.1 billion. Operating income rose 1% to $442.1 million versus last year.

However, the company’s margins faced pressure during the quarter. Gross profit margin dropped 10 basis points to 40% while operating margin fell to 16.8% from 18.7% last year. Gross margin was impacted by higher inventory shrink, lower merchandise margins and higher supply chain costs. Inventory shrink remains a persistent problem for the retailer and it is expected to impact full-year performance as well.

Outlook

Ulta Beauty raised its full-year 2023 outlook for sales but lowered its guidance for operating margin. The lowered margin guidance includes the impact of higher inventory shrink. For FY2023, the company now expects net sales of $11.0-11.1 billion versus its previous outlook of $10.95-11.05 billion.

Comparable sales are expected to increase 4-5% for the year. Operating margin is now expected to range between 14.5-14.8% versus the prior range of 14.7-15.0%. EPS is expected to be $24.70-25.40 in FY2023.