Shares of the J.M. Smucker Company (NYSE: SJM) were up over 1% on Monday after the company exceeded expectations for its second quarter 2023 earnings results and raised its outlook for the full year. The stock has gained 9% year-to-date and 17% over the past 12 months. The company expects to see high demand for many of its brands through the latter half of the year even as it tackles inflation through price hikes.

Quarterly performance

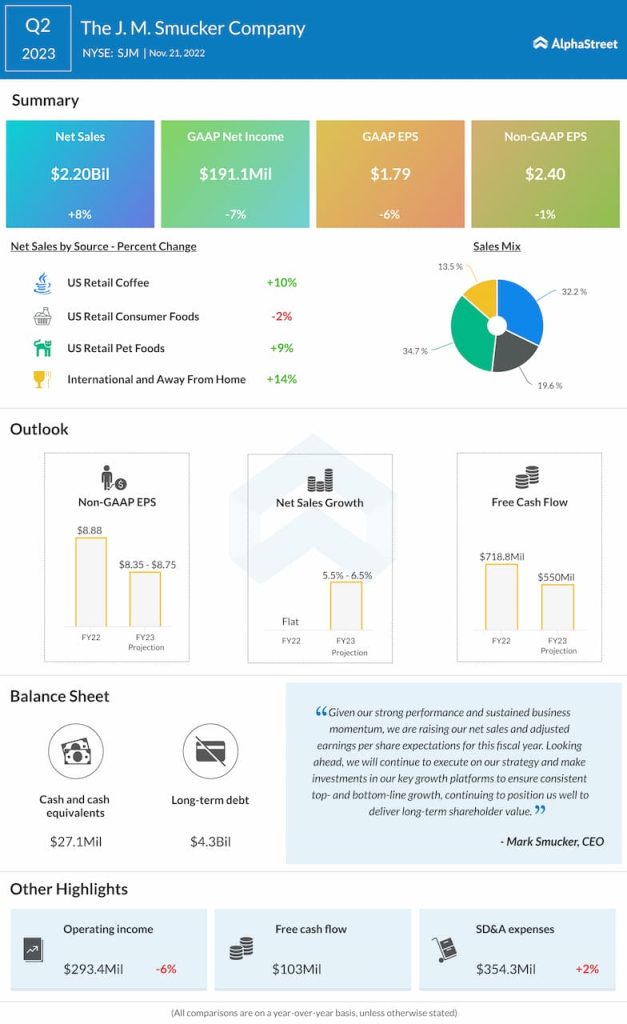

Net sales for the second quarter of 2023 increased 8% year-over-year to $2.20 billion, beating estimates. Net sales excluding divestitures and foreign currency exchange grew 11%. The growth in sales was driven mainly by price increases across its segments. Adjusted EPS dropped by 1% to $2.40 but surpassed projections.

Category performance

During the second quarter, SJM saw overall at-home food purchases remain strong amid inflationary pressures. The company recorded sales increases across most of its segments and brands helped by price increases taken to offset the impacts of inflation. It saw particular strength in the pet, coffee and snacks categories during the quarter.

In Q2, sales in the US Retail Pet Foods segment increased 9% YoY. Excluding divestitures, sales was up 14%. This growth was driven by double-digit sales increases in cat food, dog food and dog snacks. The company saw strong performances from brands like Meow Mix, Milk-Bone, Kibbles ‘N Bits and Nutrish during the quarter.

Sales in US Retail Coffee grew 10% driven by the strong performance of the at-home coffee portfolio. The company stated that at-home consumption represented 70% of all coffee drinking occasions, indicating the resilience of the category. Brands like Cafe Bustelo and Folgers delivered strong growth during the quarter. SJM expects this momentum to continue despite inflationary pressures and volume declines as customers hold on to their coffee routines.

In the US Retail Consumer Foods Segment, sales dropped 2% but was up 7% excluding divestitures. The growth was driven by double-digit sales increases in Uncrustables sandwiches and Smuckers fruit spreads. Total company net sales of Uncrustables sandwiches, including away-from-home, were $168 million in Q2. SJM expects volume and sales for the brand to grow double-digits through the rest of the year thanks to an increase in production capacity at Colorado.

International sales grew 14%, or 17% excluding divestitures during the quarter driven mainly by pet food and snacks.

Outlook

JM Smucker increased its full year 2023 revenue and earnings guidance based on strong results and demand for its brands. Net sales are now expected to increase 5.5-6.5% from the previous year. This compares to the previous outlook of 4-5% growth. This growth reflects price hikes to offset higher costs along with increased volume/mix for some of its brands and momentum in away-from-home channels. Excluding divestitures, net sales are estimated to increase around 8% in FY2023.

Adjusted EPS is now expected to range between $8.35-8.75 for the full year compared to the prior outlook of $8.20-8.60, reflecting a 2% increase at the midpoint of the guidance range. Earnings are expected to decline in the third quarter of 2023 as higher expenses offset sales benefits. In the fourth quarter, earnings are expected to grow around 10% reflecting strength across the portfolio, sequential gross margin improvement and a moderation in expenses.

Click here to read the full transcript of JM Smucker’s Q2 2023 earnings conference call