Cintas Corporation (NASDAQ: CTAS) has been growing its market share by diversifying into new areas and through acquisitions. The prudent business model, with a focus on recurring revenues, has helped it dominate the corporate identity services market. The company has been able to maintain stable revenues even in times of market uncertainty, thanks to its diversified customer base.

This week, Cintas’ stock rallied and hit a record high after it reported robust third-quarter results and lifted the full-year guidance for revenues and profit. After the recent gains, CTAS is currently trading at a premium. The stock has outperformed the market, but the valuation is high and above the historical average which is not good news for prospective investors.

Pricing Power

The Mason, Ohio-headquartered uniform rental company bets on its pricing advantage and steady expansion of non-core areas of the business, like first-aid and safety, to maintain the growth momentum. Since it takes a relatively long time for inflation pressures to have an impact on the business, the management gets the required leeway to do the planning for process improvement. So, the business can stay immune to macroeconomic uncertainties and cost escalation in the market, to some extent.

“Our pricing, it varies based upon your pricing at a local subject. So, we handle it differently in different businesses and in different geographies. So, that being said, yeah, our pricing is above what it has been historically. That being said, the volume growth is the majority of our growth. And the reason is the inflationary environment is such that — that we have to pass on a larger price increase than we do historically. Fortunately, the customers are — they understand that they understand the environment and we’ve been very successful in providing the right levels of service so that they are open to those adjustments,” said Cintas’ CEO Todd Schneider during a recent interaction with analysts.

Meanwhile, considering Cintas’ high exposure in the small and medium business segment, the drop in business confidence among SMB enterprises following the banking crisis is a cause for worry. In general, the company has a healthy balance sheet, but the $2.5-billion debt doesn’t look good. Despite the uncertainties in the market, M&A remains a key priority for the management when it comes to capital allocation, a trend that has continued over the years.

Impressive Data

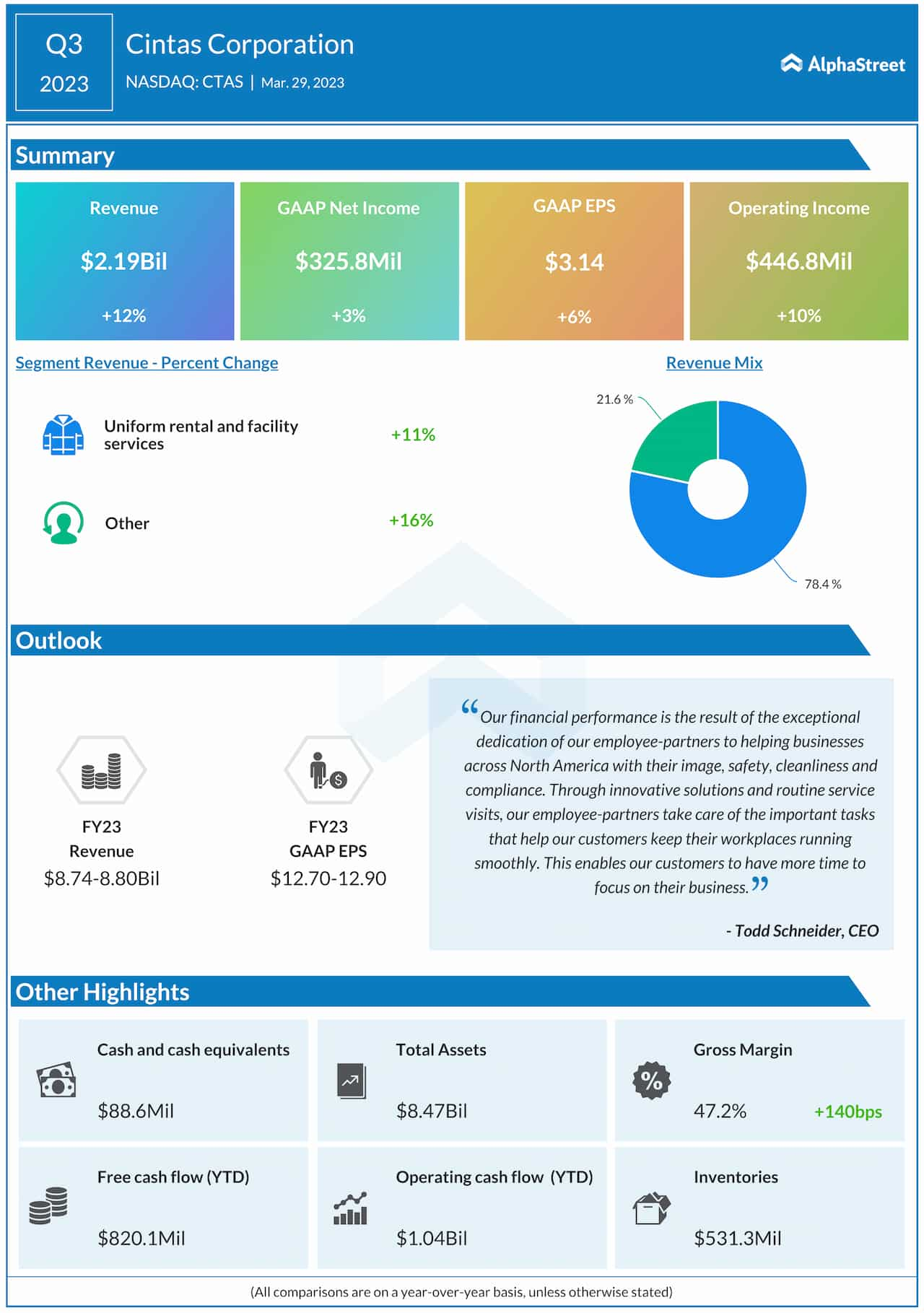

In what could be a testimony to the underlying strength of the business, Cintas reported quarterly revenues and earnings that consistently topped expectations in recent years. It achieved 11.8% organic revenue growth in the third quarter when total revenues moved up to $2.19 billion, reflecting double-digit growth in the core business. Gross margin rose an impressive 140 basis points to 47.2%, benefitting from effective cost management. The company’s extensive delivery network in the U.S. market, which accounts for the lion’s share of revenues, gives it an edge over rivals.

Outlook

The positive Q3 outcome prompted the management to raise its full-year revenue forecast to $8.74-$8.80 billion. The earnings outlook has been revised up to $12.70 – $12.90 per share. The projections are above the consensus estimates. On Thursday, Cintas’ stock traded slightly lower, paring a part of the gains that followed the earnings release. It has increased by around 7% since last week.