Shares of McCormick & Company, Incorporated (NYSE: MKC) were up 8% on Tuesday after the company delivered first quarter 2023 earnings results that beat expectations. The condiments maker reaffirmed its guidance for the full year of 2023 as well. Here are some of the highlights from the earnings report:

Better-than-expected results

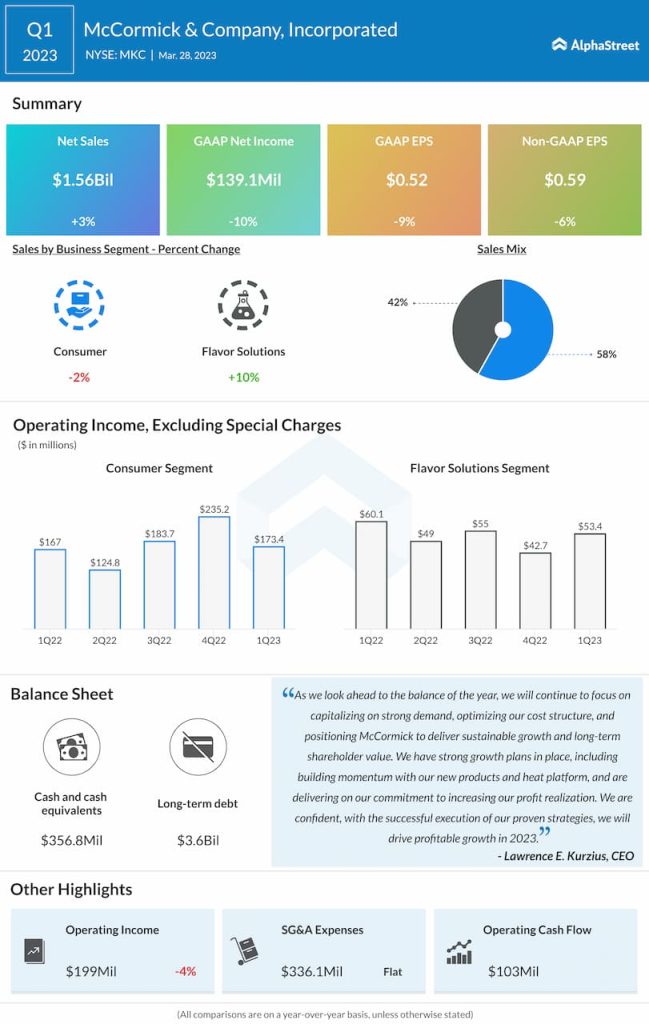

McCormick reported net sales of $1.56 billion for the first quarter of 2023, which was up 3% year-over-year and ahead of estimates of $1.54 billion. Sales growth in constant currency was 5%, driven mainly by pricing actions but partly offset by volume declines. Adjusted EPS fell 6% from last year to $0.59 but surpassed projections of $0.51.

Consumer segment recovery

McCormick’s Q1 results benefited from strong demand for its products although sales growth during the quarter was impacted by the Kitchen Basics divestiture, COVID-related disruptions in China, and the exit of the company’s Consumer business in Russia.

In Q1, sales in the Consumer segment declined 2% on a reported basis but rose 1% in constant currency, reflecting a 9% increase from pricing actions. The growth in the Consumer segment was driven by the Americas region, which saw sales growth of 3% during the quarter.

Volumes in the Consumer segment were hit by the Kitchen Basics divestiture, lower consumption in China due to the pandemic and the exit of the business in Russia. McCormick expects to see a pick-up in its Consumer segment growth from the second quarter of 2023 onwards as it laps the exit of its business in Russia and the impact of last year’s pandemic-related shutdowns in China.

Sales in the Flavor Solutions segment rose 10% on a reported basis and 12% in constant currency, driven by pricing actions. Sales growth in this segment was led by the Americas and EMEA regions, both of which saw double-digit sales increases on a constant currency basis.

In the Americas, the company saw strong growth in snack seasonings driven by new products and base business while in EMEA, higher sales to foodservice customers helped drive broad-based growth across the portfolio.

Reaffirms outlook

McCormick continues to reap the benefits of the pandemic-induced trend of consumers cooking healthy meals at home. Their strong demand for varied flavors along with McCormick’s diverse portfolio put the company in a good position to drive growth.

The company expects net sales to grow 5-7% in FY2023 versus the prior year, driven mainly by pricing actions, which along with cost savings are expected to offset the impacts of inflation. Reported EPS is expected to range between $2.42-2.47 while adjusted EPS is estimated to be $2.56-2.61 for the year.