The resurgence of COVID infections has dimmed recovery hopes of the virus-hit restaurant industry to some extent, even as uncertainty looms over the government’s market reopening plans. Fast-food chain McDonald’s Corporation (NYSE: MCD) is trying to regain the lost momentum through aggressive marketing efforts and enhancing customer experience.

Shares of the San Bernardino, California-based quick-service restaurant operator jumped to a record high this week and outperformed the market, continuing the uptrend that started about a month ago. With the company navigating through the crisis effectively, the stock is eliciting significant investor interest. The shares are on track to scale new heights this year, which makes them an investment option worth trying. Meanwhile, they look slightly overvalued.

In Recovery Mode

McDonald’s is set to release statistics for the first three months of fiscal 2021 on April 29 before the opening bell. Analysts’ outlook indicates the company is in recovery mode, with sales projected to grow 6.5% to about $5 billion and earnings by 22% to $1.79 per share.

From McDonald’s Q4 2020 earnings conference call:

“In 2021, we expect to convert more than 90% of our net earnings to free cash flow and to generate free cash flow near 2019 levels or about $5.5 billion to $6 billion. Our capital allocation priorities remain the same. First, investing in the business to drive growth. This includes both capital expenditures, as well as investments in technology and digital. Second, prioritizing dividends to our shareholders. After that, most of our remaining free cash flow for 2021 will go towards paying down debt to get back to pre-COVID leverage ratios by the end of the year.”

Road Ahead

The focus of the strategy laid down by the company to get back on track is expanding curbside pickup, drive-thru, and contactless delivery, while also increasing its digital capabilities. Last year, the digital platform accounted for about 20% of total system-wide sales. Interestingly, around $1.6 billion was spent on opening around 1,000 new restaurants in key markets and modernizing as many units in the domestic market. Meanwhile, elevated costs, mainly those related to COVID safety and restaurant closure, could be a drag on profitability in the near future.

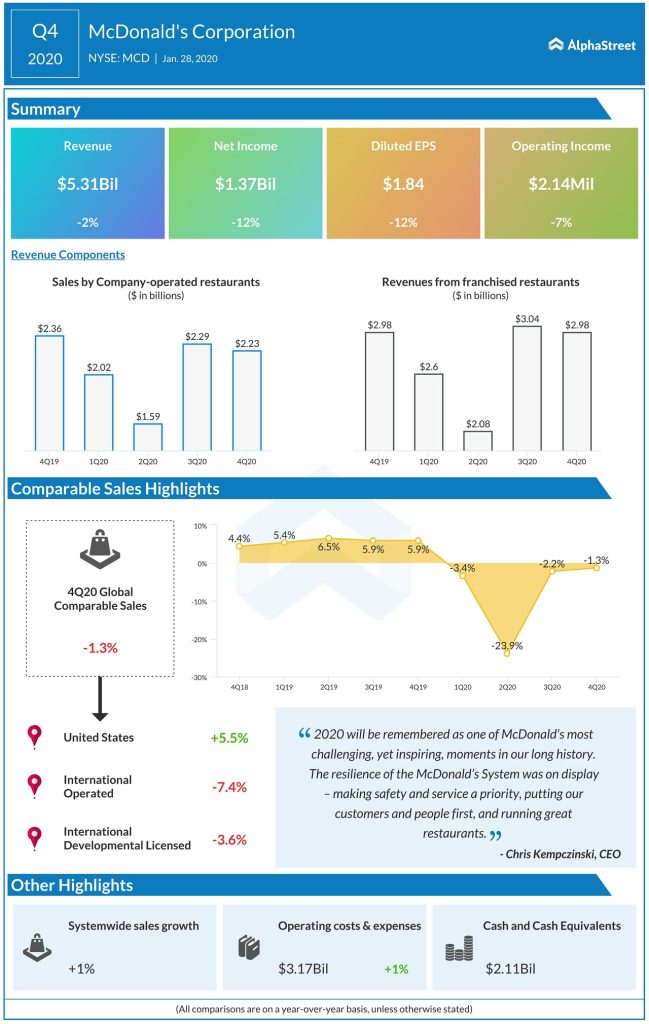

Challenging 2020

In the last several quarters, McDonald’s financial performance often fell short of expectations as the top-line remained under pressure due to the virus-related dip in restaurant traffic. In the three months ended December 2020, sales at company-operated restaurants decreased, while franchise sales remained unchanged. At $5.31 billion, fourth-quarter revenue was down 2% year-over-year, which caused earnings to fall 12% to $1.84 per share. The numbers also missed the market’s forecast.

Read management/analysts’ comments on McDonald’s Q4 results

After peaking earlier this week, McDonald’s shares closed Wednesday’s session slightly higher. It has grown 10% so far this year, with most of the gains coming in the last 30 days.