Shares of Pinterest Inc. (NYSE: PINS) stayed in green territory on Monday. The stock has dropped 40% year-to-date and 62% in the past 12 months. There is a mixed sentiment around the stock as the pandemic-driven spike in engagement continues to wane impacting Pinterest’s user growth raising concerns over its future growth trajectory. However, some experts believe the company has significant potential to expand and grow in international markets. Here are a few points to note while considering this stock:

Revenue

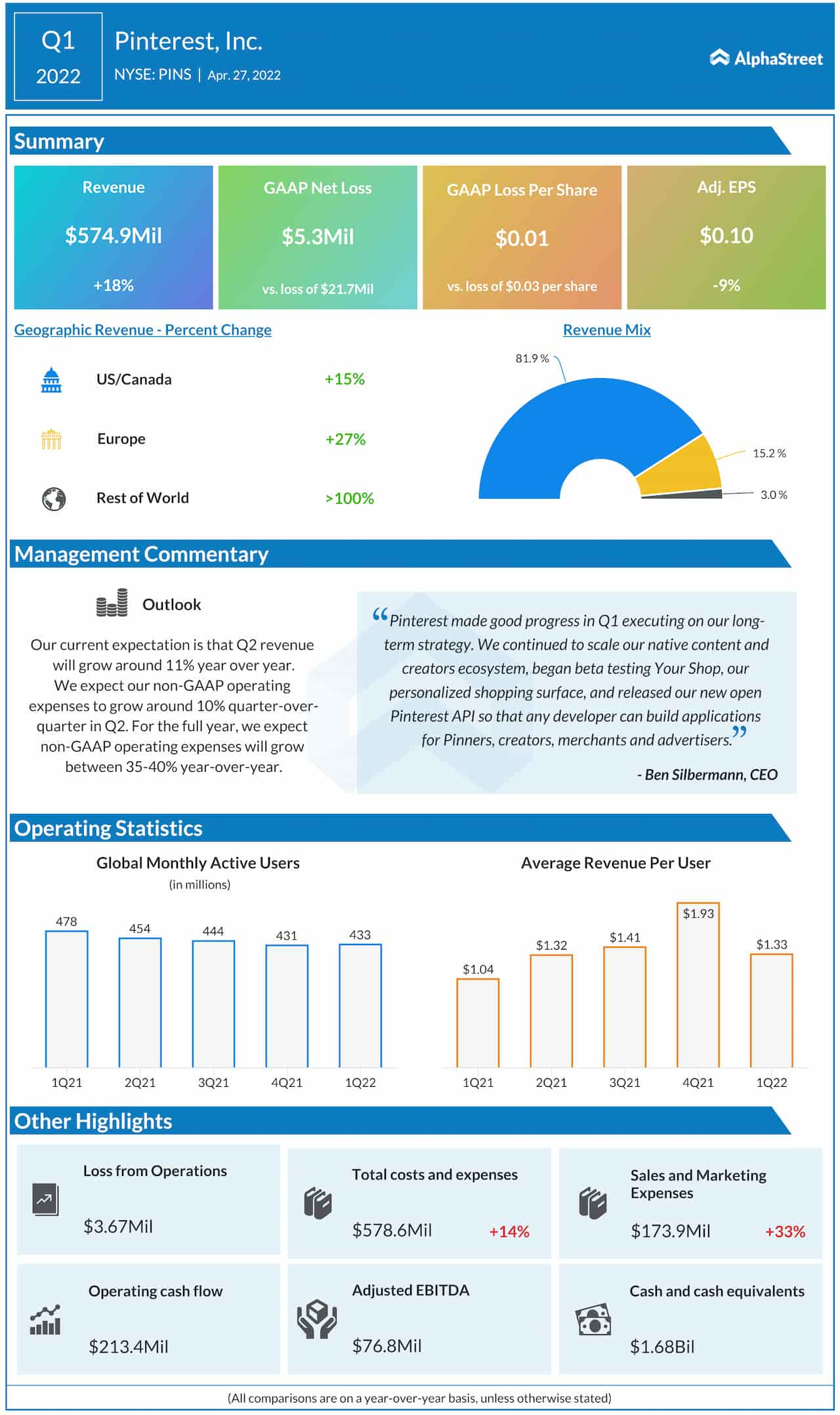

In the first quarter of 2022, Pinterest’s revenue increased 18% year-over-year to $575 million, driven by strength in advertising and growth in international markets. Although the revenue growth rate was much lower than the 78% seen in the year-ago period, the company managed to grow the top line in a challenging macro environment amid supply chain issues and the Russia-Ukraine conflict.

Pinterest saw revenue growth across all its regions as well with US and Canada posting a 15% growth and Europe posting a 27% growth YoY driven by increases in average revenue per user (ARPU). Revenue in the US was up 14%. Rest of World revenue more than doubled YoY, fueled by triple-digit growth in ARPU. Global ARPU increased 28% YoY to $1.33, driven by advertising demand. ARPU grew 31% in US and Canada and 40% in Europe. Rest of World ARPU grew 164%.

For the second quarter of 2022, Pinterest expects revenue to grow around 11% YoY. This compares to a revenue growth of 125% in Q2 2021. The company believes it will continue to face headwinds such as supply chain issues and inflation. On its quarterly conference call, Pinterest said its investment in building a native content ecosystem is likely to remain a mid-single digit headwind to revenue but it believes this effort will be accretive to revenue and engagement over time.

User growth and engagement

Pinterest’s declining user numbers are a prime cause of concern. Global monthly active users (MAUs) were down 9% YoY to 433 million in Q1 2022 as the pandemic-fueled boom subsided. MAUs were also impacted by lower search traffic caused by Google’s algorithm change last November. Pinterest saw MAUs decline across all its regions. US and Canada MAUs were down 13% while Europe MAUs fell 12% YoY. Rest of World MAUs dropped 6%.

Despite these declines, in Q1, Pinterest witnessed a mid-single digit growth in its global mobile app MAUs, which account for a vast portion of its impressions and revenue. The company also witnessed resilience in its shopping engagement as the number of Pinners engaging in shopping surfaces grew compared to last year.

Pinterest is working on driving user acquisition and retention by removing barriers to longer browsing sessions. The company now does not ask users to sign up immediately when they land on the site. Despite slight negative impacts on new user sign-ups initially, Pinterest believes these efforts can drive activations over time.

Looking ahead, in Q2, Pinterest expects to face seasonal impacts as well as headwinds from the search algorithm change along with potential challenges from future search algorithm updates. Additionally, the company believes the pandemic unwind will no longer cause a headwind to MAUs in the third quarter of this year.

International opportunity

Several experts believe that Pinterest has substantial opportunity to expand and grow in international markets. Despite a decline in users, revenues in the Rest of World region grew 152% YoY to $17 million. ARPU rose 164% to $0.08. Although this is much lower compared to ARPU of $4.98 in the US and Canada, there appears to be significant room for expansion in these markets presenting the company with further growth opportunity over the long term.

Click here to read the full transcript of Pinterest’s Q1 2022 earnings conference call