Enterprise data cloud company Cloudera, Inc. (NASDAQ: CLDR) has been incurring losses ever since it was founded more than a decade ago. There is uncertainty as to when the company would turn profitable, especially in the absence of a proper turnaround strategy. The latest buzz is that the management might be looking for potential buyers to sell the company.

The main challenges facing the tech firm include relatively longer sales cycles and stiff competition from industry leaders like Amazon (AMZN) and IBM (IBM). Cloudera’s prospects of moving into the positive territory in the near term were further dampened by the US-China trade war, which is affecting its overseas expansion.

Related: Cloudera Q3 2020 Earnings Conference Call Transcript

When Cloudera reports fourth-quarter results early next month, the market will be looking for cues on creating value for shareholders, who have been patiently waiting for updates on the management’s revival strategy.

The fact is that Cloudera might not record profit in the near future. Despite its unimpressive earnings performance, the company continues to spend heavily on customer acquisition and commercialization of the platform, adding to its growing deficit. Also, costs associated with the integration of Hortonworks, the rival cloud firm that joined the Cloudera fold recently, have been taking a toll on profitability.

Headwinds

The company, which generates revenue mainly from subscriptions and services, also deals with government agencies and other regulated entities. Such transactions could be time-consuming and pose challenges when it comes to monetization. The stress on profitability will persist in the near future as the management goes ahead with its aggressive expansion program. The key initiatives include investments in research and development and enhancement of the open-source data management ecosystem.

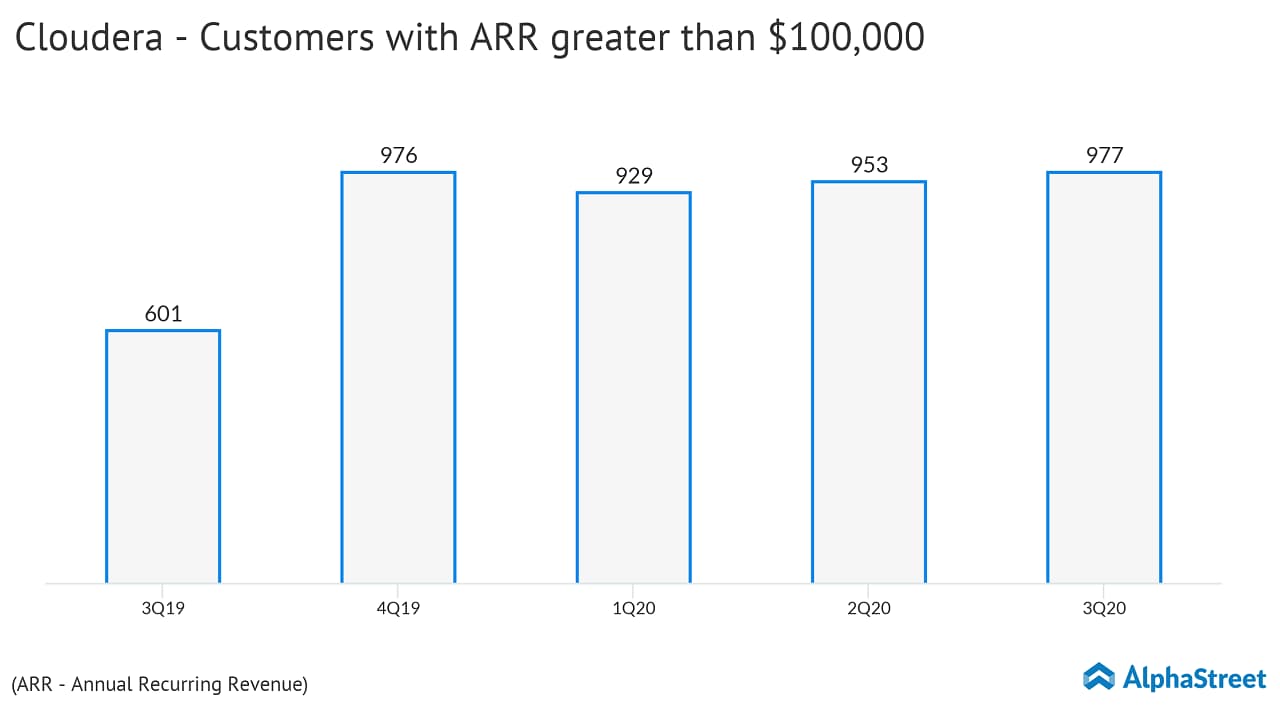

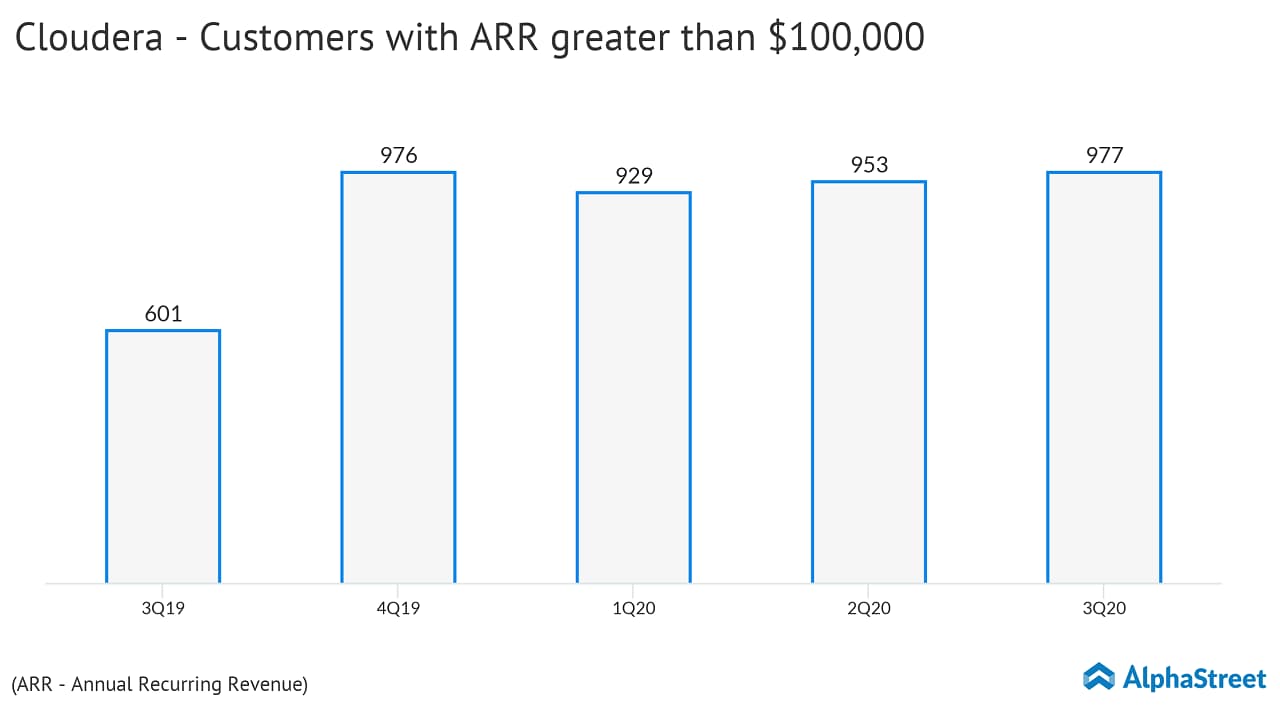

Customer Additions

The company registered steady growth in its client base this year and ended the third quarter with 977 high-value customers. It reported an adjusted net loss of $0.03 per share for the quarter on revenues of $198.3 million, which surpassed the market’s prediction.

Those buying Cloudera’s stock need to be cautious as it is not for short-term investors. Most of the analysts covering the company recommend holding the stock, with a target price that suggests that the value would improve gradually. The fact that Cloudera has only a short operational history makes it difficult to predict its future.

Stock Performance

Cloudera shares made notable gains last year, after falling to an all-time low in mid-2019, but once again lost momentum towards the end of the year. The stock lost 22% in the past twelve months.

Also read: Accenture to thrive on digital, cloud prowess next year

ADVERTISEMENT

In an interesting move, the company last month roped in Rob Bearden, who previously headed Hortonworks, to take up the role of chief executive officer.