Riding on the growing demand for information technology services, Accenture (NYSE: ACN) scaled new heights this year and established itself as a dominant player in the delivery of digital and cloud services. Armed with its industry-leading solutions, the professional services provider is likely headed to another rewarding year. It is ending 2019 with a robust order pipeline and a stable customer base.

Bull Run

The stock maintained a steady uptrend over the years and crossed the $200-mark for the first time early this year. Analysts are bullish about its prospects and the majority recommends buy, predicting further gains in the coming days. Brokerage firms, including RBC Capital and UBS Group, recently lifted their price targets, taking the average to about $221. Accenture has an impressive track record of rewarding shareholders by paying handsome dividends and repurchasing the stock regularly.

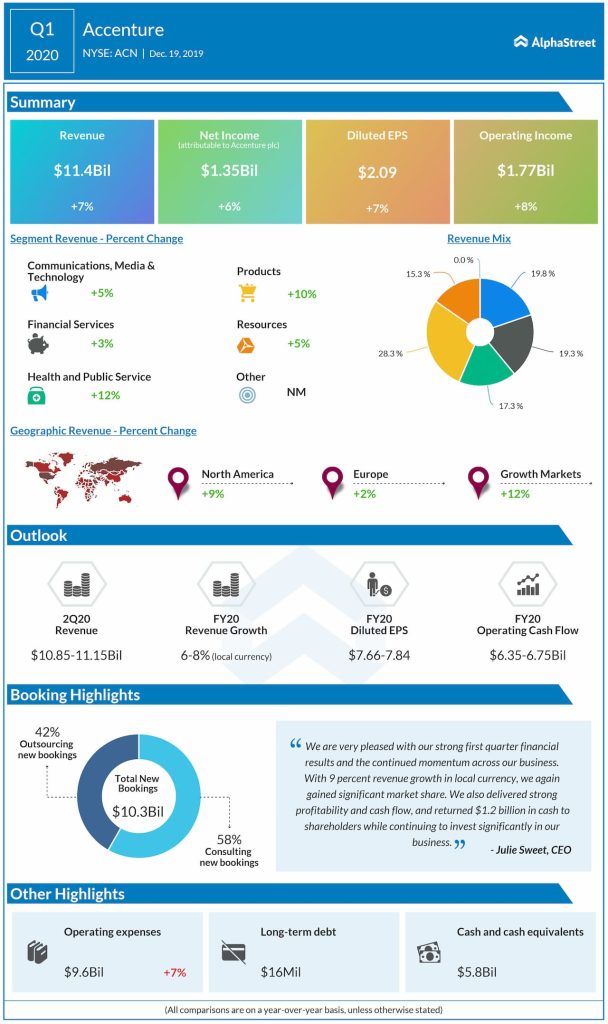

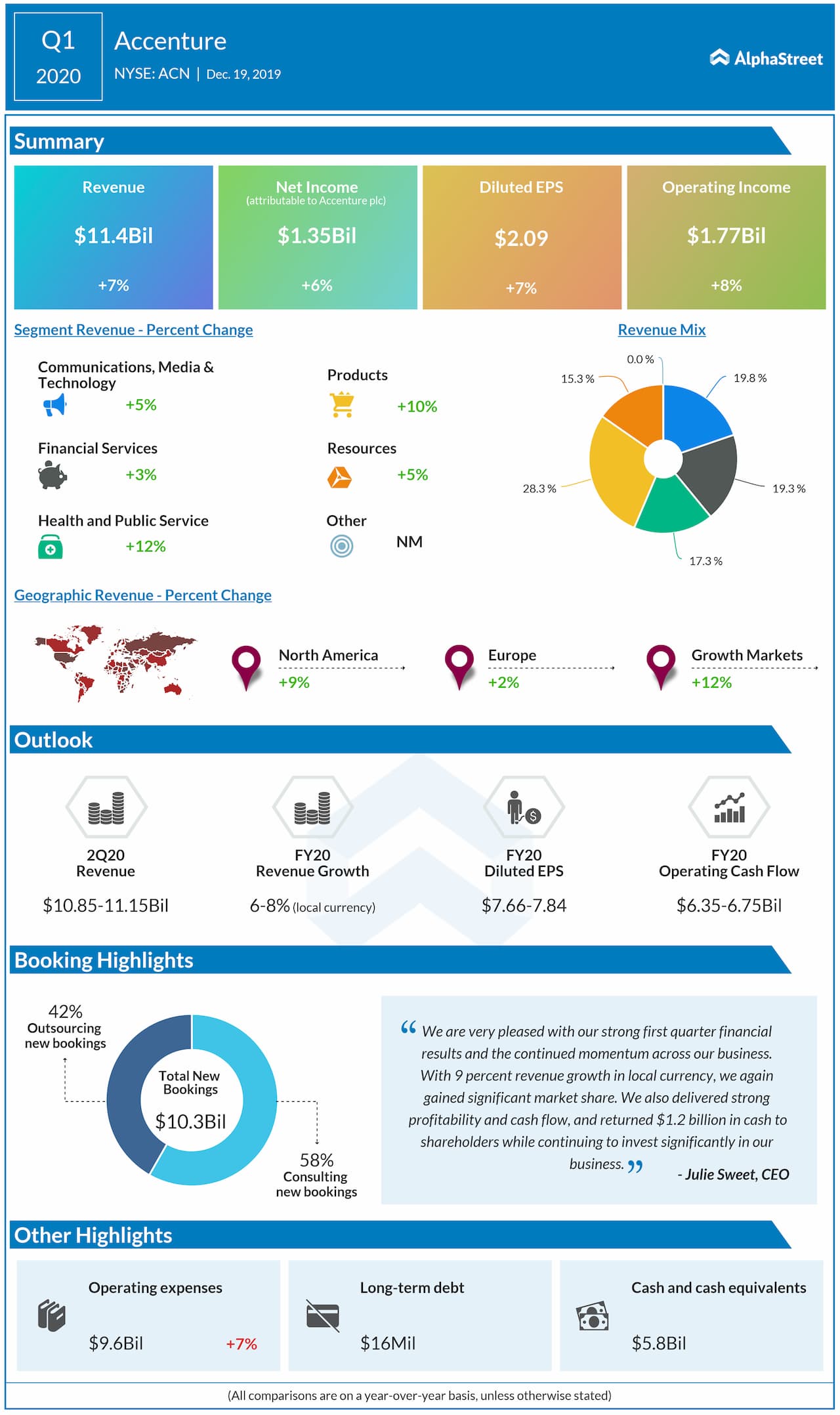

Another factor that makes the stock an investors’ favorite is its encouraging post-earnings performance in the past. In the first quarter, solid revenue growth across all the business units and geographic segments drove up the top-line. As a result, earnings rose 7% to $2.09 per share. The results also topped the market’s estimates, spurring a stock rally.

Future Perfect

The management’s financial projection indicates that the positive momentum will be sustained in the current quarter and beyond, marked by broad-based revenue growth and earnings performance.

Going forward, the mobile and cloud businesses will be playing a key role in revenue generation, offsetting a potential slowdown in banking that could be a drag on the financial services segment.

Pricing Holds Key

It is important to have a prudent pricing strategy in order to retain the client base as competitors in the overseas market, mainly in Europe and India, would be looking to grab market share through competitive pricing. Also, uncertainties in the global economy can weigh on enterprise spending, affecting Accenture’s order growth.

Also see: Accenture Q1 2020 Earnings Conference Call Transcript

It needs to be seen whether the current rate of market share growth would be maintained in 2020, considering the signs of saturation seen in some markets. In the past, the company managed its cash flow with focus on ensuring proper shareholder return without compromising on investments.