The mainstream auto industry has been hit by the COVID-driven financial insecurity and economic uncertainty but the crisis proved to be a boon for the automotive aftermarket as people put off new purchases and instead upgraded their existing vehicles for longer use. Advance Auto Parts, Inc. (NYSE: AAP) is thriving on the high demand for vehicle accessories and spare parts.

The company’s market value more than doubled since early 2020 when it was hit by a major selloff. After rising to a record high last week, the stock pulled back and traded lower on Monday. But, its long-term prospects look encouraging, with the consensus target price signaling an increase in the twelve-month period.

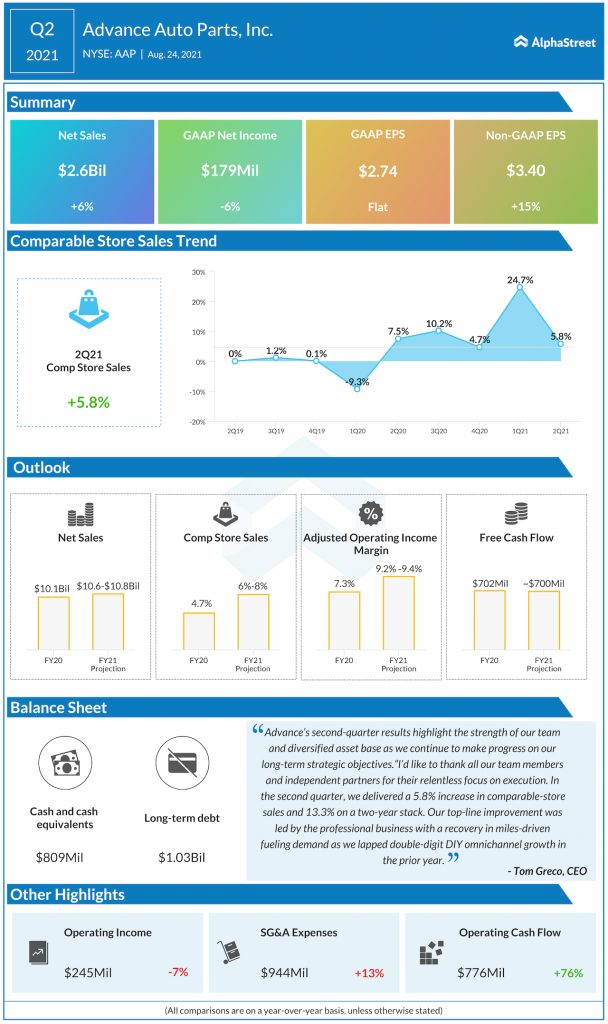

Read management/analysts’ comments on quarterly reports

Despite the strong gains, the valuation looks favorable, which makes AAP a good investment option. But the stock is not cheap enough yet and that would make some investors wait until it drops further. However, more gains are in the cards as the company gears up for third-quarter earnings next month.

Being confined to their homes, many people have taken up do-it-yourself tasks, and vehicle maintenance and modification are among the most popular activities that in turn drive auto parts sales. Meanwhile, the ongoing chip shortage, which is causing production and delivery delays, has added to the slowdown in new vehicle sales.

Taking advantage of its omnichannel capabilities, Advance Auto Parts achieved strong quarterly sales growth after experiencing weakness in the early days of the crisis. It also helped the company improve profitability. Curently, it is looking to tap into the unfolding opportunities — the recent tie-up with Bridgestone Retail Operations to sell the DieHard batteries is an important step in that direction.

Strategic investments are strengthening our professional customer value proposition. It starts with improved availability and getting parts closer to the customer as we leverage our dynamic assortment machine learning platform. Within our Advance Pro catalog, we saw improved key performance indicators across the board including, more online traffic, increased assortment and conversion rates and ultimately growth in transaction counts and average ticket.

Tom Greco, CEO of Advance Auto Parts

Advance Auto Parts is a market leader but that doesn’t insulate it from the stiff competition in the industry, with the main rivals being AutoZone, Inc. (NYSE: AZO) and O’Reilly Auto Parts (NASDAQ: ORLY). A marked slowdown in comparable sales growth, a key indicator of the demand trend, in the most recent quarter has raised fears that the virus-driven demand boom might be diminishing, which can be attributed to the market reopening. Also, the company’s margins face pressure from elevated costs, mainly those related to employee compensation and shipping.

Though same-store sales increased in the July quarter, growth decelerated to 5.8% from 24.7% in the preceding quarter. There was a 6% increase in net sales to $2.6 billion, which was in line with experts’ prediction. At $3.40 per share, adjusted earnings were up 15% from last year and above the estimates.

Tesla moves into overdrive: Key takeaways from Q3 earnings report

Advance Auto Parts’ stock has stayed above its 52-week average consistently for more than six months, reflecting the underlying strength. It closed the last trading session at $233.71, after gaining about 6% since last month.