The dominance of Nike Inc. (NYSE: NKE) in the sports apparel and footwear market has remained unchallenged over the past several years, and it is considered superior to the other major players in the market. Despite being a consumer discretionary brand, the sneaker maker’s sales bounced back quickly from last year’s COVID-induced slowdown.

The majority of the 20-odd analysts following the stock recommend buying it, projecting a 10% growth in the 12-month period, which looks reasonable considering the impressive past performance. The stock has become cheaper after retreating from last month’s record high. So, it is best to buy the dip and forget it.

DTC Push

Currently, the management’s CapEx program is focused on expanding the direct-to-customer channel, a strategy that would better align the business with the new market conditions. The shift from store-based operations to DTC and initiatives like the Nike Fitness Club and shopping app — that enables convergence between physical and digital shopping — is expected to create considerable demand for the brand and help the company maintain market dominance in the foreseeable future.

Read management/analysts’ comments on Nike’s Q1 earnings

While ramping up the digital infrastructure, efforts are also on to ensure a unique and interconnected customer experience. The back-to-school season, which followed a fruitful summer sports season, was highly rewarding for the company, thanks to the kid-specific designs and strong digital growth in that segment. Meanwhile, the persistent uncertainty due to the pandemic and the related production/logistics disruption would remain a concern as far as meeting the near-term goals is concerned.

Cautious Outlook

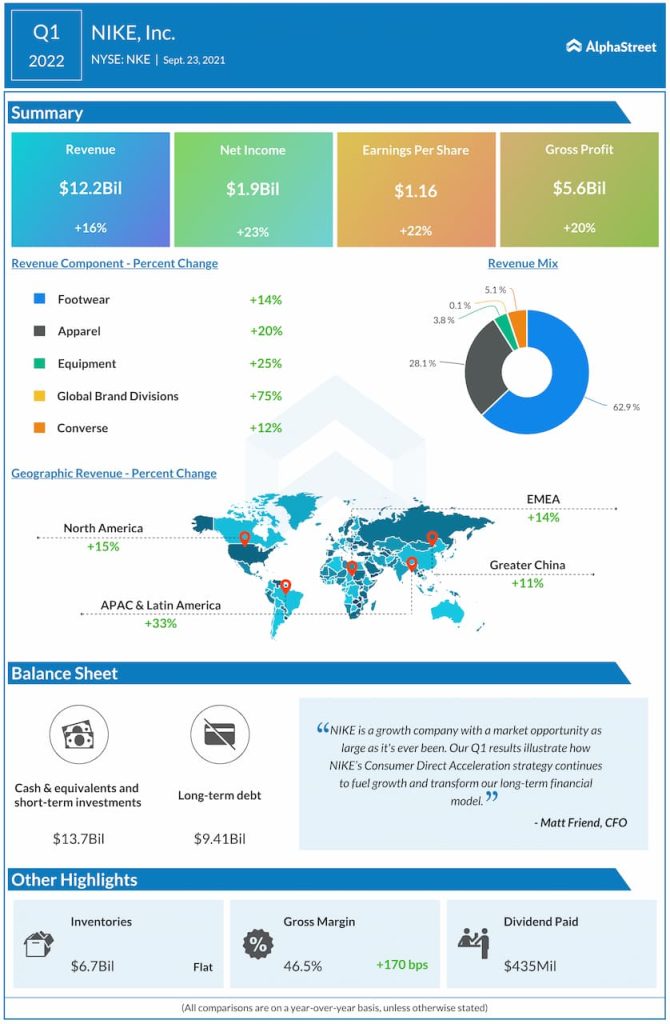

Nike started fiscal 2022 on a high note, with all geographical segments and the five operating units registering double-digit sales growth in the early months of the year, driving up total revenues to around $12 billion. At $1.16 per share, first-quarter earnings were up 22% year-over-year. But the stock dropped soon after the announcement as the management’s cautious outlook for the current quarter and fiscal year did not go well with investors.

From Nike’s Q1 2022 earnings conference call:

“Today, we’re in a stronger position relative to our competition than we were prior to the pandemic. Why? Because the changes happening in the market work in our favor. Consumers shift to digital that might have taken five years, will now only take two. That plays to NIKE’s advantage and our consumer-direct acceleration strategy is capitalizing on this marketplace transformation. We know that when we get to the other side of this, we’ll be in even stronger shape. We’ll be more agile, more direct, and more digital.”

Key highlights from Foot Locker Q2 2021 earnings results

Rival sneaker maker Under Armour Inc. (NYSE: UAA) last month raised its full-year 2021 sales growth outlook to 25%. In the third quarter, earnings and revenues increased and topped expectations, aided by the management’s aggressive marketing efforts. Adidas and Puma, the other prominent players in the market, also generated strong sales this year.

At the Bourses

Though the market’s initial response to Nike’s first-quarter earnings report was not very encouraging, the stock made steady gains since then and crossed the $150-mark. It traded lower on Tuesday morning, after closing the previous session lower.