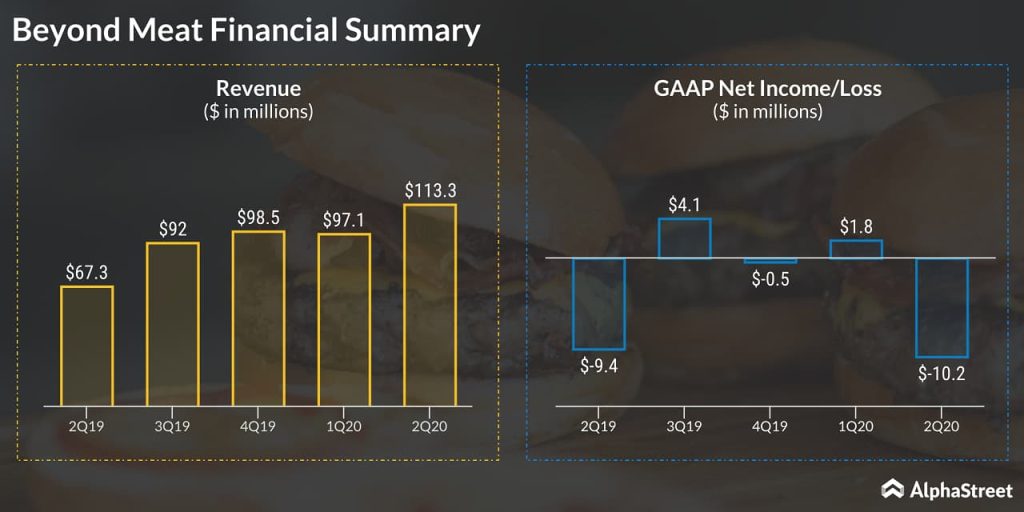

Plant-based meat producer Beyond Meat (NASDAQ: BYND) reported its second quarter 2020 results on Tuesday. Even though the numbers weren’t that bad, BYND stock tumbled 6.72% and closed at $132.69 yesterday. During Q2 earnings call, the management said that the company is now leaning more toward the retail business as its foodservice business was hurt by the global pandemic.

Q2 results

As the company projected in the first quarter earnings call, the ongoing COVID-19 health crisis resulted in the closure or limited operations of many of Beyond Meat’s foodservice customers in the second quarter. However, there was an increase in demand from retail customers as consumers shifted towards more at-home consumption, which partially offset the decline in sales to foodservice customers.

Changing focus

Across the US and international markets, retail net revenues increased 192% year-over-year in Q2, driven by expansion in total distribution points, higher sales velocity at existing outlets and new product introductions. In the US, Beyond Meat expanded in the club stores, including Sam’s Club and BJ’s Wholesale, added to the existing retail tailwinds.

When answering an analyst’s question, CEO Ethan Brown stated,

“So we did have this tremendous growth in US retail activity, and the thing that was most stunning to me was around this shift that the team was able to accomplish from roughly a 50:50 foodservice to retail distribution in the beginning of the year to this 88% retail, 12% foodservice, and to move all the lines in the products over that way.“

Decline in foodservice business

Revenue from US international foodservice business decreased 59% year-over-year during the second quarter. The management said that it has been taking steps to face the headwinds in foodservice business.

Beyond Meat offered aggressive promotional programs to many of its foodservice partners helping them to offer a plant-based meat options to consumers at reduced price points. The company increased its total foodservice distribution points globally by 16% to 8,000 outlets on a sequential basis.

Outlook

Once the normalcy levels are returned, foodservice business is expected to return to a strong growth trajectory. For the remainder of the year, Beyond Meat anticipates US foodservice demand to remain soft compared to the year-ago period, given the return of high rates of COVID-19 infections across many parts of the US.

Beyond Meat has been seeing growing activity in the international retail markets including China and some parts of Europe. The company expects this growth to continue in some parts of the globe as they are recovering quickly.

With regard to the 2020 outlook, the guidance remained suspended because of the effects of the COVID-19 pandemic. However, the management expects COVID-19 to continue to impact its business operating environment at least through the balance of the year.