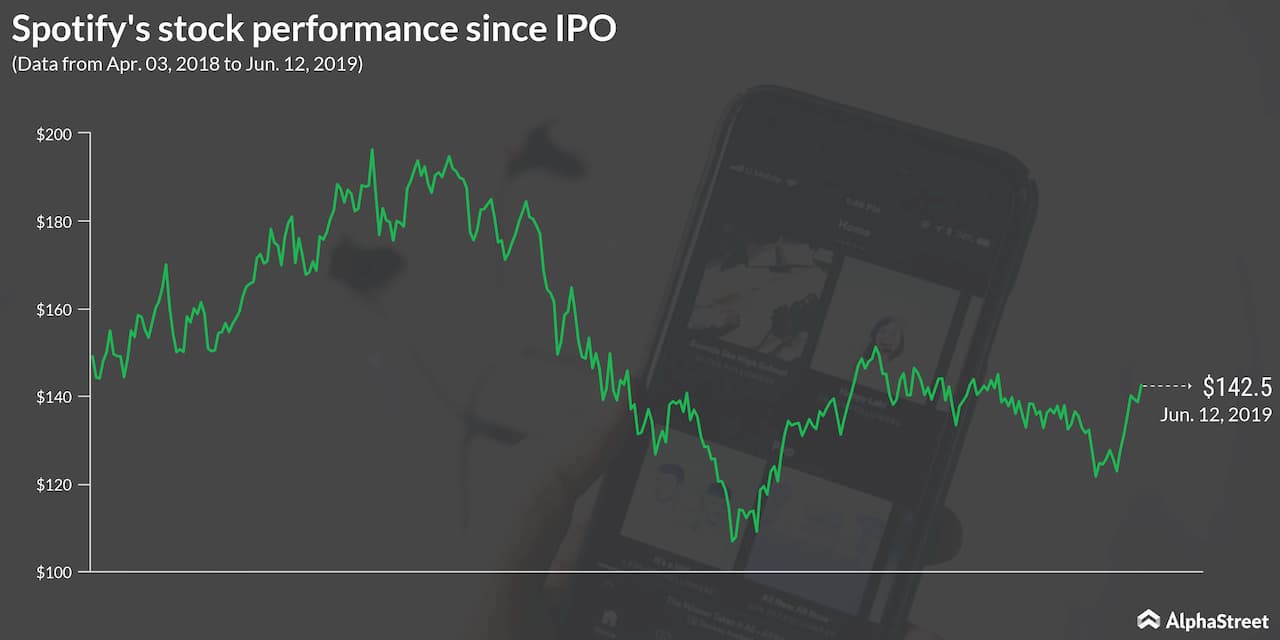

Spotify (NYSE: SPOT)

stock has recovered 38% since late December when it touched a new 52-week low

of $103. However, the streaming giant has lost about 15% since the stock market

debut in April 2018, as concerns about profitability and nimble rivals linger

with investors.

Let’s take a quick look at Spotify to get a better understanding of the stock.

Competitors

Spotify faces tough competition from Apple Music both in the US and globally. Apple Music has a catalog of around 50 million songs, which is larger compared to Spotify, giving it an advantage over the Swedish firm. According to a report by Reuters, Apple Music had 28 million paid subscribers in the US as of the end of February versus Spotify’s 26 million.

Other competitors include Deezer, Pandora (now

part of SiriusXM), and music services by Google and Amazon.

Deezer is a French company that has 14 million active users and its service is available in over 180 countries. The streaming service has 53 million tracks and 100 million playlists.

Pandora Media was founded in 2000 and as of

2018, the company was said to have 71.4 million active users and 6 million

subscribers. Pandora was acquired by SiriusXM Holdings Inc. (NASDAQ:

SIRI) in 2019 for $3.5 billion.

Spotify also faces competition from Google Play Music, YouTube Music and Amazon Prime Music.

To take on the competition, the streaming major has made its foray into podcasting by acquiring three firms Parcast, Gimlet, and Anchor. It has also expanded its presence globally by launching in India this year with more than 2 million users already onboard.

This is expected to help Spotify increase the total addressable market and increase its user base, which would augur well to achieve its long-term goal of reaching above 1 billion listeners.

Market

expansion

Spotify has two revenue generation models, Premium and Ad-Supported. The premium model offers ad-free music services to subscribers comprising unlimited online and offline high-quality streaming access to its catalog. On the other hand, the ad-supported model provides users with limited on-demand online access to its catalog, with advertisements.

The premium has been seeing steady growth, primarily helped by its Family Plan. It also benefited from the expansion of its Google Home Mini promotion as well as the price reduction on its Premium + Hulu offering in the US.

During the first quarter, the company

expanded its partnership with Hulu by offering limited commercial plan to

Standard $9.99 subscribers at no additional charge. This replaces its existing

$12.99 Spotify + Hulu bundle and builds upon the success and popularity of

Spotify Student + Hulu plan available in the US.

The company

believes that voice speakers are a critical area of growth, particularly for

music and podcasts, and Spotify plans to continue to pursue opportunities to

expand its presence in that area. In March, the company extended its

partnership with Google by expanding Google Home Mini promotion to two new markets,

the UK and France.

The company

has also joined hands with Samsung, whereby the Spotify app will be preloaded

on millions of new Samsung devices globally. Separately, it offers a special

six-month free trial to new users in the US who purchase Samsung Galaxy S10

device.

Financials

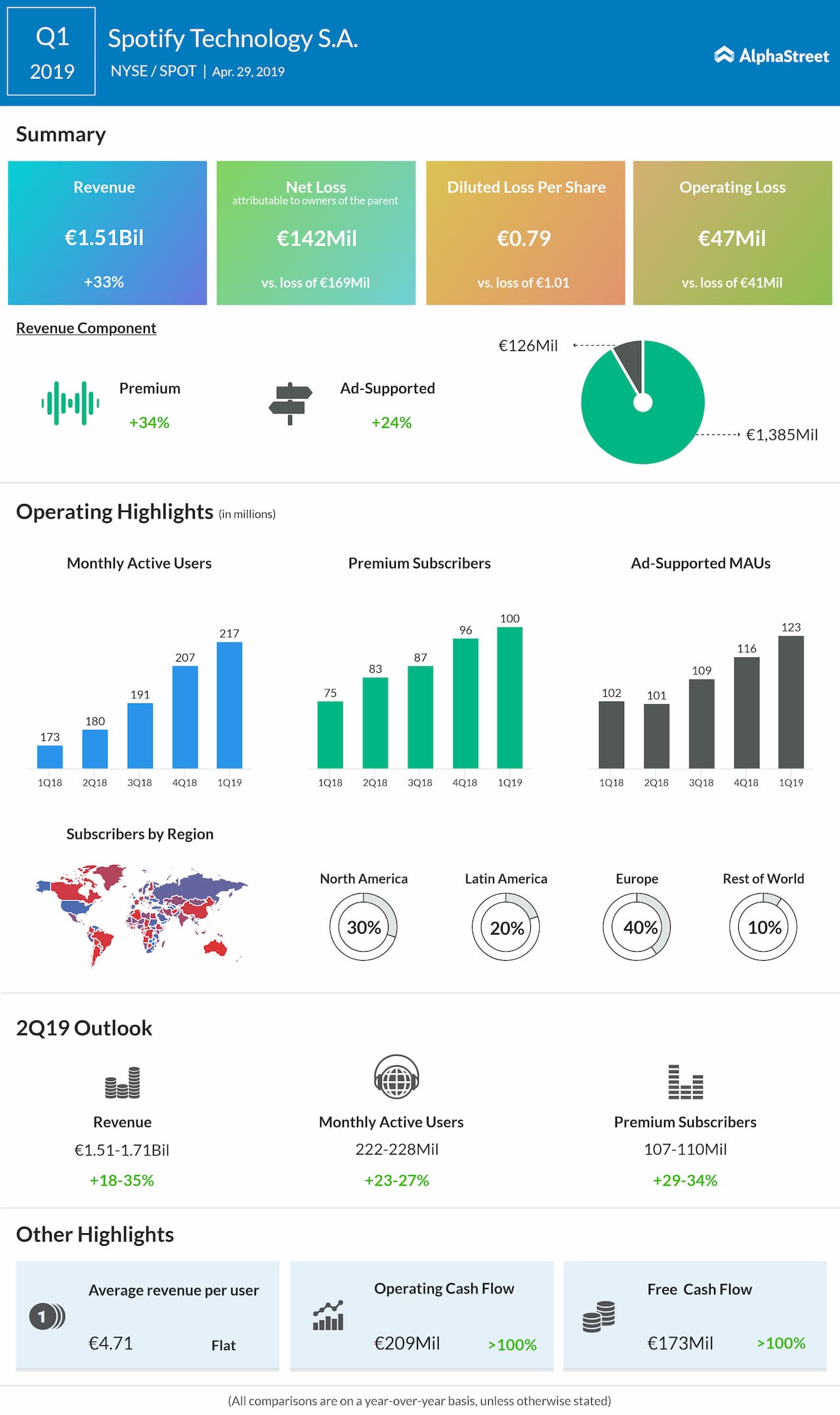

Spotify has not been a profitable company, though it did surprise Wall Street by reporting an operating income in the fourth quarter of 2018. The company swung to a loss in the very next quarter and is yet to provide a roadmap as to how it hopes to achieve profitability.

Being a budding market, the music streaming industry is prone to a lot of variables. Companies are spending most of their cash to grow their customer base and expand to new markets. Apple, with abundant cash reserves, come at an advantage here.

In the past four quarters, the company has twice missed earnings estimates. Though premium revenues have been quite steady, the same cannot be said about ad-supported revenues. Investors would now like to look beyond revenue and subscriber growth to assess the long-term prospects of this company.

Cash position

Though Spotify has been making its association with big music companies financially beneficial, it continues to pay huge amounts as royalty, putting liquidity under stress.

The music streamer, which is yet to report a profit after going public more than a year ago, has maintained positive working capital dynamics since then.

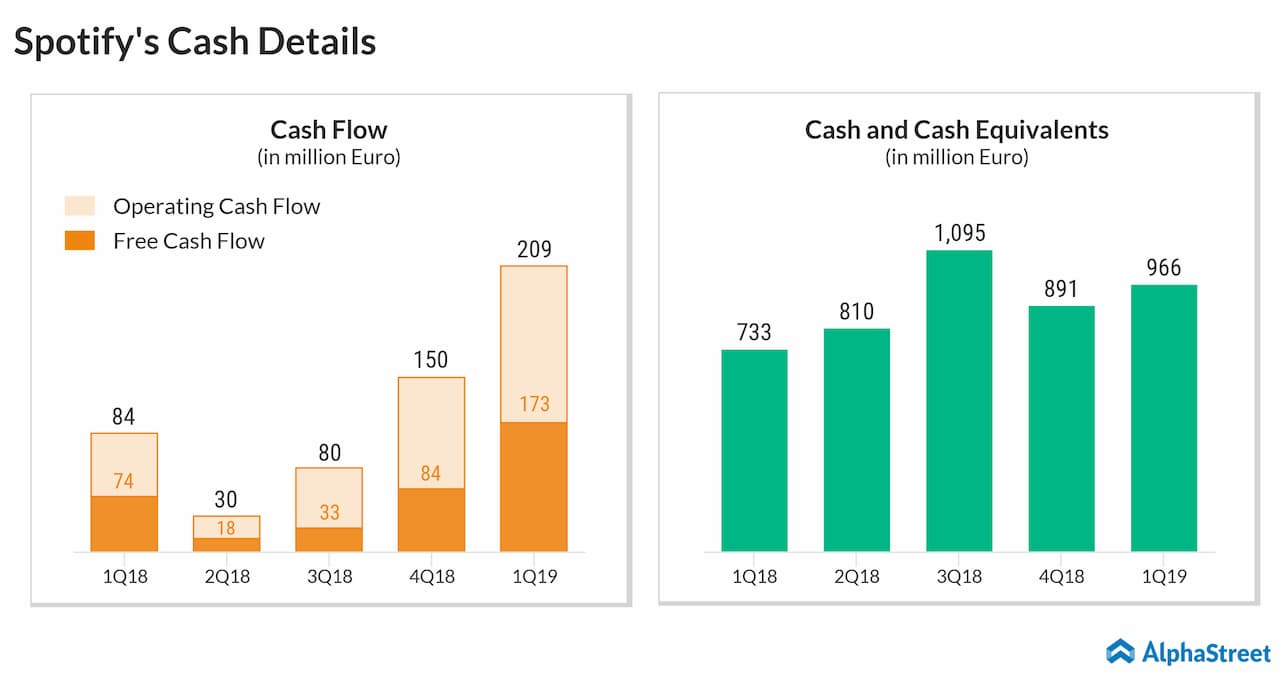

Emerging from the negative territory, it improved its cash flow consistently after the market debut. In 2018, total cash flow from operations surged to EUR 344 million from EUR 179 million a year earlier. In the March quarter, operating cash flow more-than-doubled to EUR 209 million and there was a corresponding growth in free cash flow to EUR 173 million.

While striving to improve free cash flow, the

management also sees a spike in capital expenditures, mainly associated with

investments in new office buildings in Europe and multiple locations in the US.

The total cost of the project is estimated at EUR 200 million.

Wall Street

view

When it comes to analyst estimates, 12 analysts tracked by TipRanks are expecting the stock to touch $168 mark in the next 12 months, which is an increase of 18% from today’s trading range of $142. On the rating front, 9 have given “buy”; 2 offer “hold” and 1 with “sell” recommendations.

Credit Suisse analyst Brian Russo, who has a

bearish outlook on the stock, stated, “While we expect significant subscriber

(subs) and revenue growth for SPOT, we believe consensus multi-year

expectations for its subs and margins are too high and see risk as ongoing

battles over content costs support concerns around Spotify’s profit

potential.”

When it comes to bull side, Benjamin Swinburne of Morgan Stanley believes Spotify has great potential to grow given its leadership position in Android along with higher engagement level compared to peers like Amazon Music.

Looking ahead

For the full-year 2019, Spotify expects revenue to be in the range of EUR 6.35 billion to EUR 6.8 billion, representing year-over-year growth of 21-29%. Total monthly active users are estimated to be between 245 million and 265 million, up 18-28% from the fiscal year 2018. Total premium subscribers are touted be in the range of 117 million to 127 million, up 21-32%.

Spotify has been focusing on investing in podcasts recently, with the aim of boosting revenues with a long-term perspective. Apart from growing the subscription revenue, Spotify expects to increase its ad-supported revenue through this long-term action plan. The company has been investing in non-English speaking countries also thus growing globally in the podcast industry.

However, investors should note down what Spotify has mentioned as risk factors in its SEC filing; “… we cannot assure you that the growth in revenue we have experienced over the past few years will continue at the same rate or even continue to grow at all. We expect that, in the future, our revenue growth rate may decline because of a variety of factors, including increased competition and the maturation of our business.”

Listen to on-demand earnings calls and hear how management responds to analysts’ questions