Domino’s Pizza, Inc. (NYSE: DPZ) is probably the most popular pizza brand and it has dominated the market for quite some time, aided by competitive pricing and quality products. Restaurant chains, in general, have emerged from the slump experienced in the early days of the pandemic, leveraging the mass shift to tech-enabled home delivery.

Last year, the Michigan-headquartered fast food company’s performance in the stock market was not very impressive. The stock experienced high fluctuation and ended the year sharply lower. But it changed course after entering 2023 slightly higher and regained a part of the momentum. According to market watchers, DPZ is poised to become attractive as it gains further this year, but the stock is relatively expensive.

Pros & Cons

Domino’s has been keen on aligning its business with people’s changing consumption behavior. The company benefited from the growing presence of food-delivery aggregators like Uber in the market even as an increasing number of customers opt for home delivery. At the same time, the food delivery boom might put competitive pressure on the company going forward. High raw material costs and labor shortage would be a drag on its performance this year. Also, the company needs to strike the right balance between online and offline sales because dining out is in vogue once again, ever since markets started reopening.

Domino’s CEO Russel Weiner said at the last earnings call, “in a world where consumer confidence is shrinking and inflation is high, Domino’s will succeed as we have strong profitable franchisees, a team that makes disciplined decisions based on insights and have the digital supply chain and delivery expertise to offer best-in-class value and customer experience. We delivered around one out of every three pizzas in the United States before the pandemic and we deliver around one out of every three pizzas today.”

Domino’s Pizza, Inc Q3 2022 Earnings Call Transcript

Domino’s financial results for the fourth quarter are expected to be out on February 23 early morning. On average, analysts predict net earnings of $3.96 per share for the December quarter, which represents a 7% decrease from the year-ago quarter. Revenues are seen growing by 7% to $1.44 billion.

Q3 Outcome

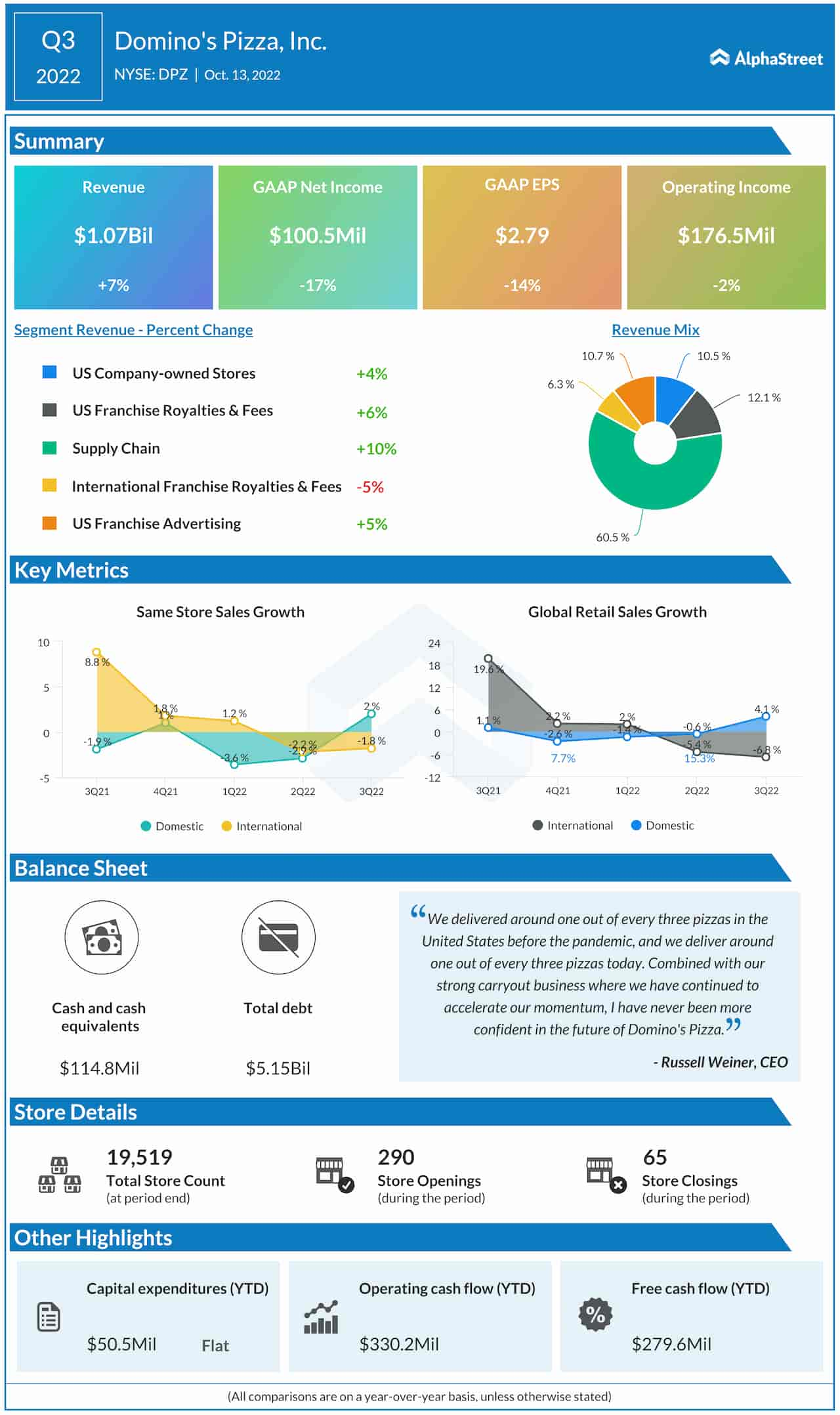

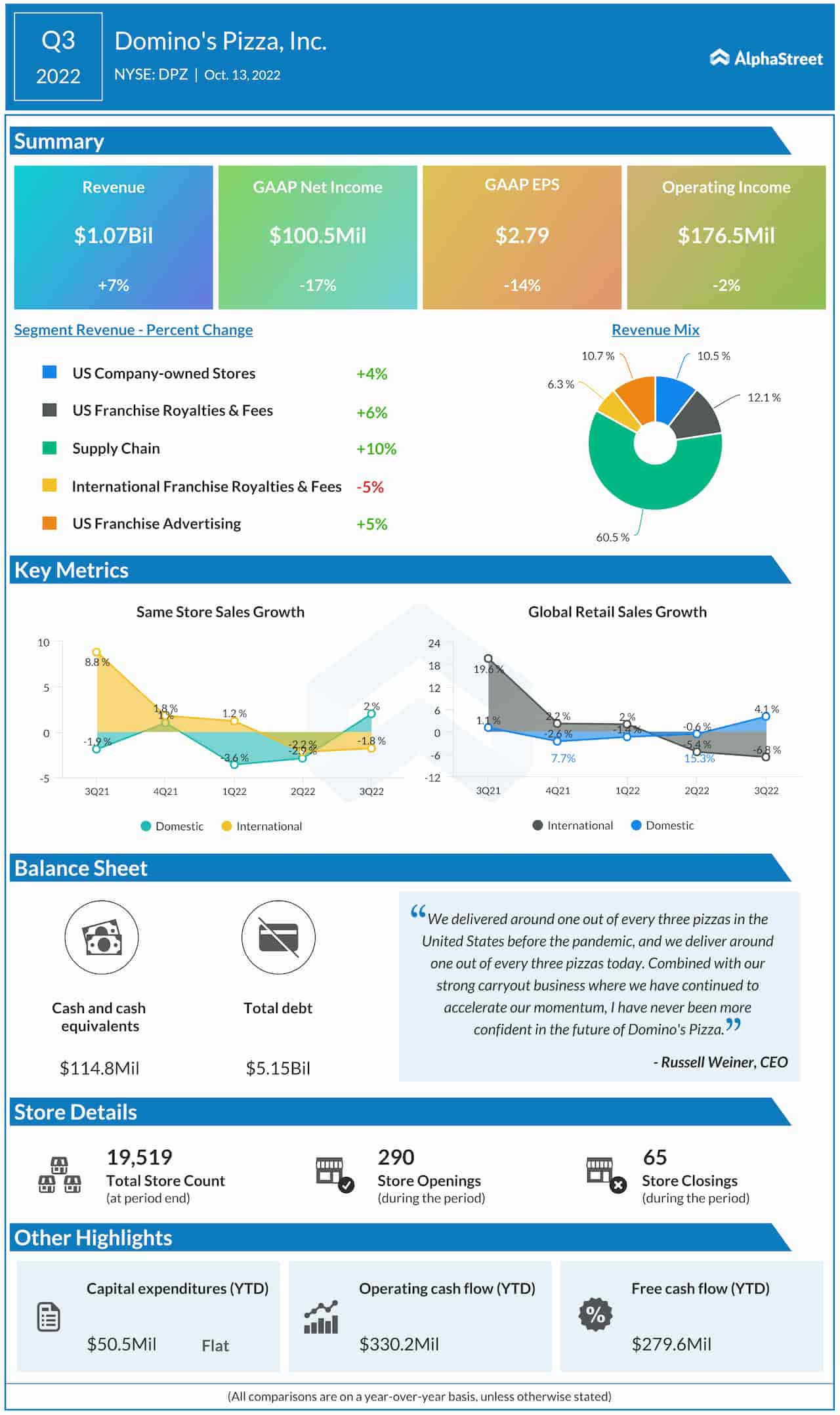

In the third quarter, non-GAAP earnings declined and fell short of expectations, as they did in the trailing three quarters, while sales matched estimates. Across all business divisions, except International Franchise Royalties & Fees, revenues advanced during the September quarter. Total revenues increased 7% annually to $1.07 billion, while earnings declined to $2.79 per share.

The stock opened Friday’s session at $360.10 and traded lower throughout the session, reversing the trend seen in the early part of the week. It has gained 6% so far this year.