The COVID-related disruption had a relatively bigger impact on GoPro, Inc. (NASDAQ: GPRO), the company that redefined the concept of action photography, as customers chose to hold back discretionary spending. The setback came at a time when the company was making efforts to recover from a long-drawn slowdown.

[irp posts=”65354″]

Market watchers are not very optimistic about the tech firm’s current performance and project a loss for the second quarter, when revenues are estimated to fall by 62%. The results are scheduled to be released on August 6. The consensus target price on the stock points to a downtrend and reflects the bearish market sentiment.

Hold GPRO?

Right now, not many investors would be interested in the stock, which continues to test the patience of shareholders. But, the low price is enough reason to keep the stock under the radar, and some experts believe it is more likely to move up than lose further. For the favorable valuation to translate into returns, the company should get back on the recovery path as it did in the final months of the last fiscal year.

Reorganzation

Earlier this year, GoPro announced a restructuring plan, with a focus on reducing operating costs and optimizing operations, in the wake of the pandemic. Meanwhile, the ongoing efforts to ramp up the online platform are yet to bear fruit and the sluggish progress of the expansion plan suggests that the slowdown might extend into the post-COVID era.

The key to driving revenue growth is to reach out to new customers and lure existing ones into upgrading their products. That can be achieved by focusing more on the subscription program and using the direct-to-customer channel effectively as it will resonate well with customers in the changed market scenario.

The perennial weakness in operations raises questions about the sustainability of GoPro’s business model. Probably, it needs to revamp the product portfolio and revise the strategy in accordance with the changing customer mood.

Unsteady Recovery

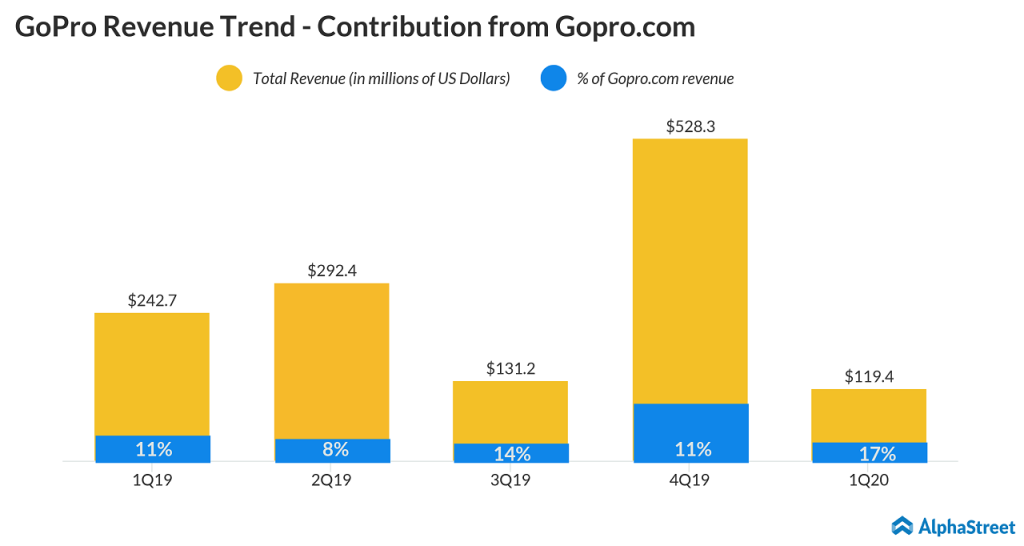

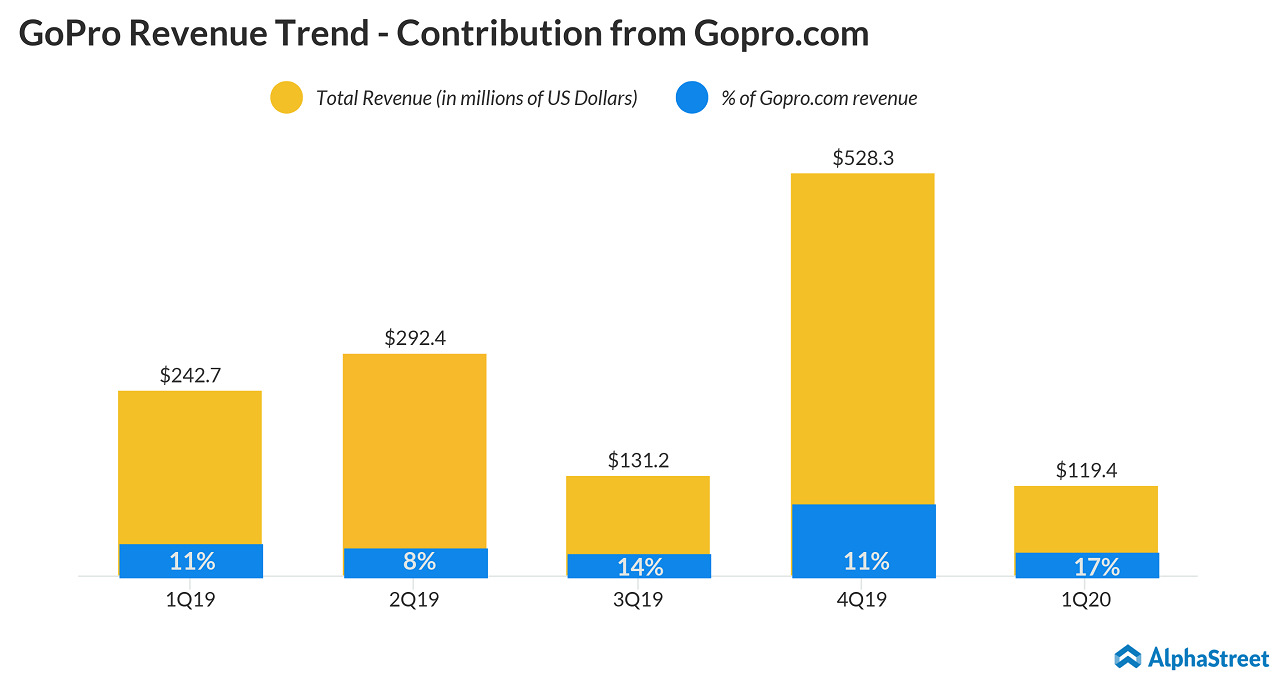

GoPro has been struggling to remain profitable and the bottom line often slipped into the negative territory in recent past, amid faltering sales. Revenues plunged 51% year-over-year to $119 million in the March-quarter when both the operating segments witnessed a double-digit decline. Consequently, net loss widened to $0.34 per share from $0.07 per share last year. Camera shipments were at a record low, reflecting the supply chain issues caused by the virus outbreak.

Want to read the management/analysts’ comments on the latest quarterly results? Check

After bottoming out during the recent selloff, GoPro shares rebounded and once again moved above $5 last month. However, the stock stays below its long-term average and continues to underperform the market though it has gained 17% since the beginning of the year.