The recent uptrend in the residential real estate market, after holding up the momentum during the pandemic, came as a surprise to many. Despite being part of an industry that is easily prone to economic uncertainties, KB Home (NYSE: KBH) is riding on the high demand for new constructions and favorable home prices. The homebuilder has navigated similar challenges in the past and stayed profitable, with earnings regularly beating estimates.

Unexpected Factors

Interestingly, the factors that drove the housing market growth were mostly unexpected, such as the record drop in mortgage rates and increased home affordability. That set the backdrop for many young Americans to consider buying their own residential property. The current trend shows the jobs of prospective home buyers, who typically belong to the middle/upper-income category, were not materially affected. KB Home’s strong presence in the country’s fast-growing areas also gives it an advantage as far as new home sales are concerned.

From KB Home’s Q4 2020 earnings conference call:

“As we continue to rotate into a high-quality mix of communities, effectively manage our costs and reduce our amortized interest, we are generating significantly higher margins, and our balanced approach to optimizing price and pace in this robust demand environment is providing further support. We begin 2021 with momentum with our backlog value up over 60% year-over-year and the potential to generate as much as $6 billion in housing revenues this year as we focus on building our scale.”

The stock is currently trading at the highest level in about 18 years, raising concerns that it is probably overvalued. Market experts are divided in their outlook, with the majority assigning buy rating. At $43.50, the current target price indicates a 5% upside. Last year’s 67% hike in dividend makes the stock more attractive. But that doesn’t mean it is immune to the potential volatilities in the housing market.

Mixed 2020

KB Home ended fiscal 2020 on a mixed note, with the disruption to the business offsetting benefits of the market recovery. There are also psychological factors that help KB Home, including the high propensity to buy new homes at a time when living in secured environments is a top priority for most people.

The company expects to leverage its solid backlog, community opening pipe-line, and effective cost structure to generate double-digit operating margin this year. Encouraged by the impressive financial performance, the management is planning to further increase the quarterly dividend. The current strategy also includes expansion into new markets, while strengthening foothold in existing markets. On the other hand, the reduction in investments in land and development, as part of preserving liquidity amid the COVID-related uncertainty, would weaken the growth prospects.

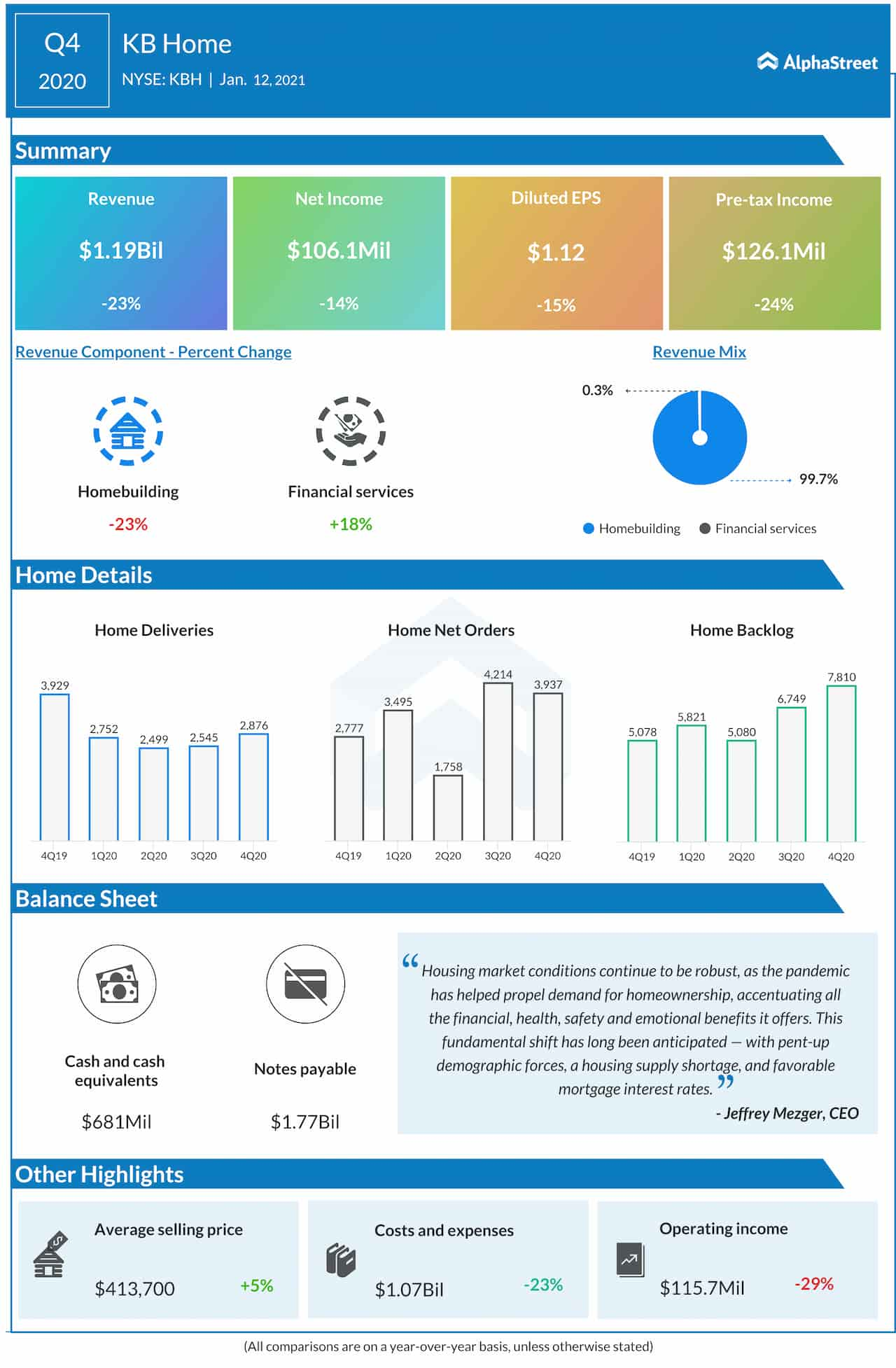

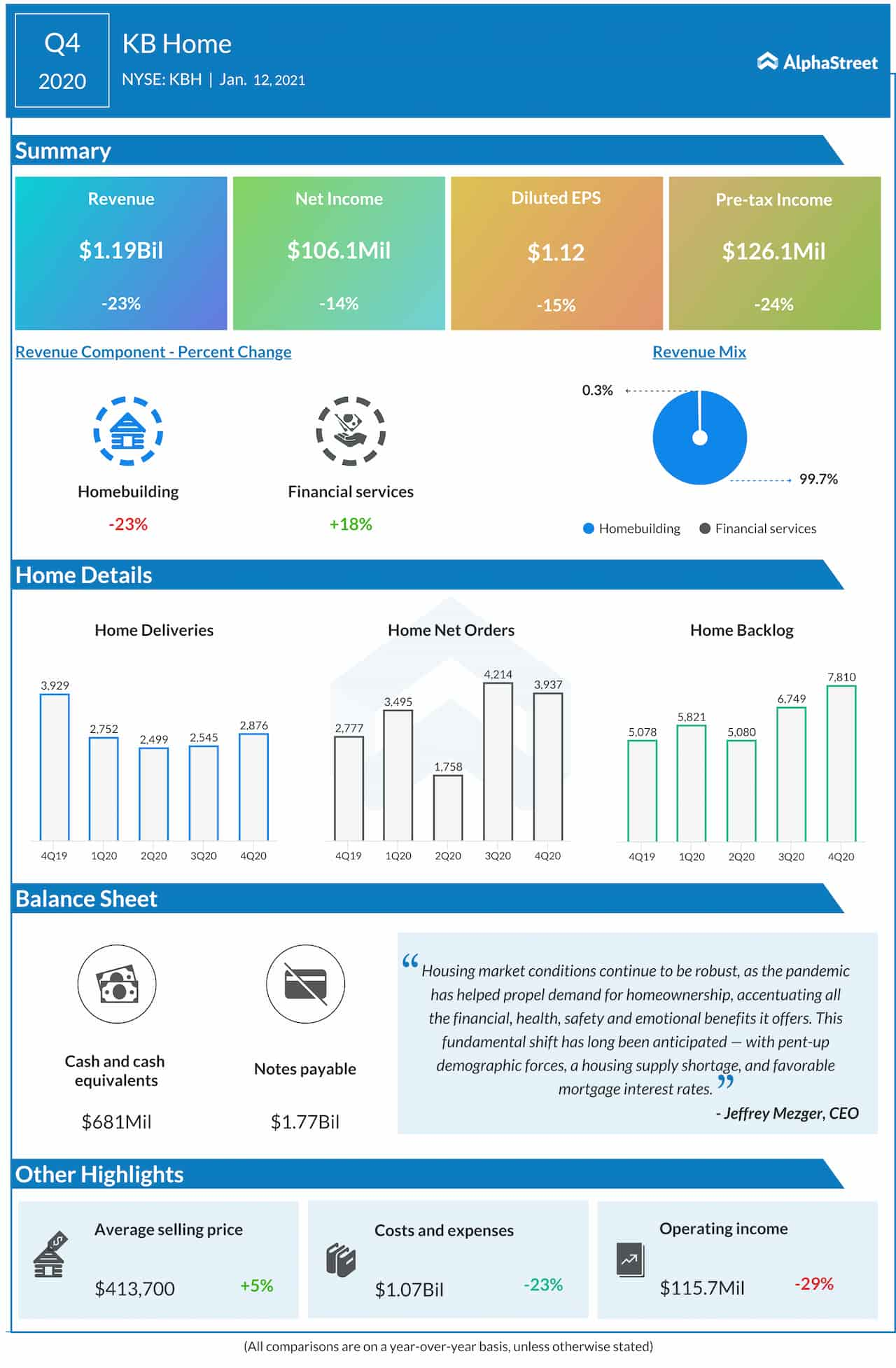

Q4 Results Beat

Meanwhile, the COVID-related disruption and curbs imposed by the government had a negative impact on KB Home’s performance in the fourth quarter. Both sales and earnings declined in double-digits to $1.2 billion and $1.12 per share, respectively. But it was better than the outcome analysts had predicted.

Read management/analysts’ comments on KB Home’s Q4 results

Shares of KB Home stayed in an upward trajectory after last month’s earnings report and reached multi-year highs, before pulling back last week. The downtrend continued and the stock traded lower throughout Thursday’s regular session. It has gained 23% so far this year.