When coronavirus tightened its grip on the country early last year, Kimberly-Clark Corp. (NYSE: KMB) witnessed a sales boom. While most consumer goods companies are thriving on the shopping spree triggered by the shutdown, Kimberly-Clark is benefiting directly from the high demand for personal care products like tissues and napkins.

Pros vs. Cons

The Texas-based manufacturer of paper-based hygiene products has hiked its dividend consistently in recent years, eliciting significant investor interest. Despite experiencing volatility, the company’s shares maintained a steady uptrend and have created decent shareholder value. The stock, which experienced weakness in recent weeks, is expected to bounce back. However, experts recommend holding KMB, taking a cue from the lingering market uncertainty.

Read management/analysts comments on quarterly reports

But the stock is a good long-term bet, given the underlying strength of the company which has been around for more than a century, serving customers across the globe. The relevance of Kimberly-Clark’s products will only increase in the coming months as customers will likely stick to their new consumption habits.

In Growth Mode

With its cost-saving initiatives yielding results, the management is shifting focus to investing in long-term growth. The K-C strategy, focused on growing the brand portfolio, is on track and complements the ongoing restructuring that is expected to complete this year. But the business will face challenges in the near term amid the persistent market uncertainty.

We’ll continue to invest in our brands and commercial capability to ensure we’re able to grow both in the near term and in the long term. We gain market share in 2020 and our shares are off to a good start this year with strong gains in many key markets. At the same time, we’re moving rapidly especially with selling price increases to offset commodity headwinds. We’ve done this successfully in past commodity cycles and we expect to do this again now. I remain confident in the underlying health of our brands and in our growth strategies.

Michael Hsu, chief executive officer of Kimberly-Clark

Weak Q1

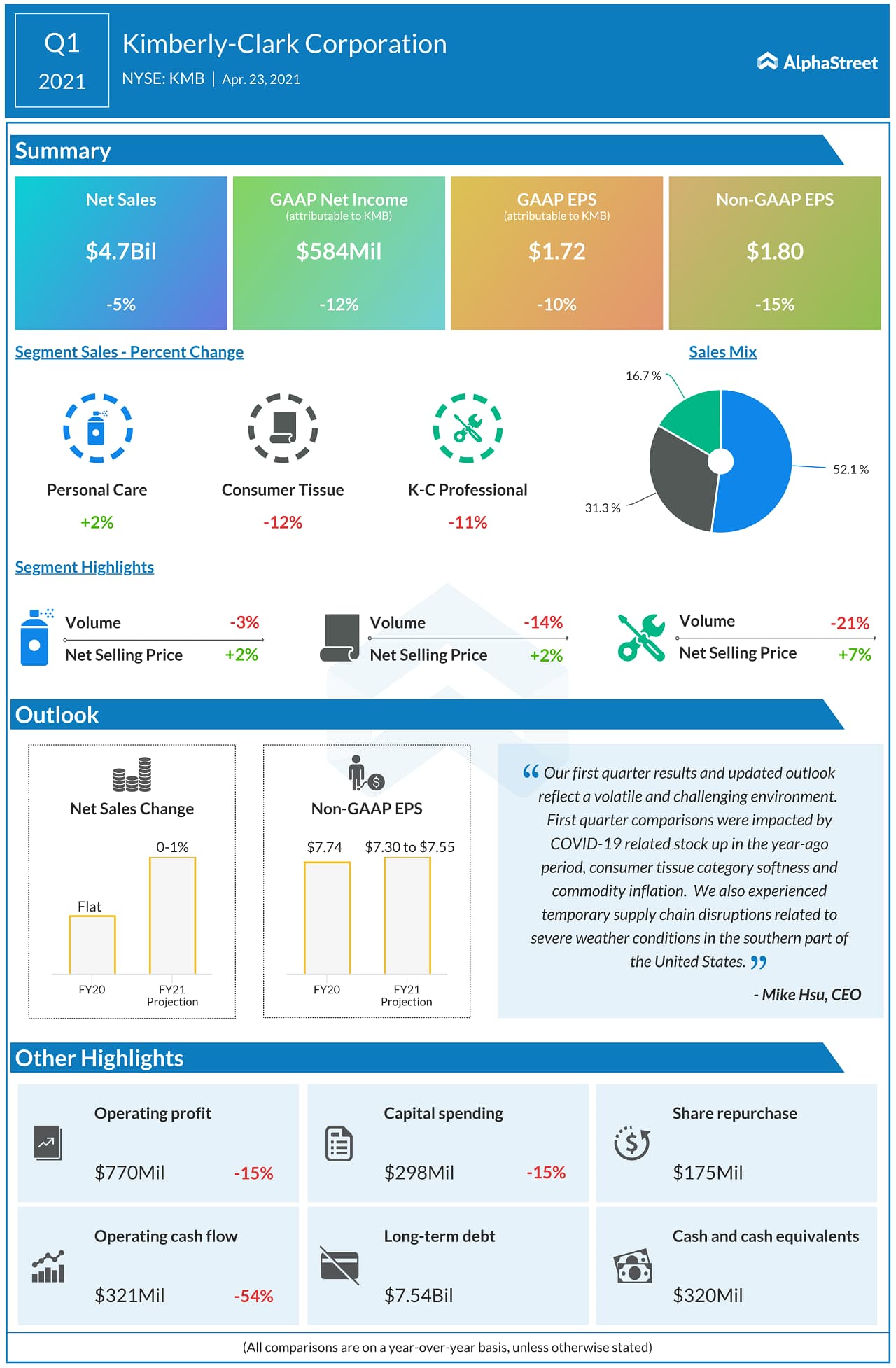

Kimberly-Clark entered fiscal 2021 on a low note, with first-quarter earnings and revenues shrinking and missing Wall Street’s prediction. There was a 5% year-over-year decline in sales to $4.7 billion, which translated into a double-digit fall in adjusted earnings to $1.80 per share. A modest increase in the core personal care business was more than offset by weakness in the other segments. But its impact on profit was partially offset by a broad-based increase in selling prices.

Procter & Gamble posts strong Q3 results

Last week, Kimberly-Clark’s stock suffered one of the biggest losses after the company released its first-quarter report, paring most of the recent gains. It fell about 8% in less than a week and closed the last session slightly above $130.