Fashion retailer Nordstrom, Inc. (NYSE: JWN) has been in the firing line of coronavirus since the onset of the pandemic, with sales crumbling to new lows as customers stayed away from the stores. But the situation is not much different for the other retailers, except for those having full-fledged e-commerce platforms.

[irp posts=”63022″]

The Comeback

Though the Seattle-based company has started reopening its stores — among the first in the business to invite customers back to the stores — it might not translate into profit during the remainder of the current quarter as the items are considered to be consumer discretionary. For the time being, the focus will continue to be on the online platform, considering the complexities involved in selling products in stores, due to safety concerns.

It is important to understand how consumer behavior has changed in the last few months and retailers like Nordstrom need to make the best use of their online and offline facilities to adapt to the new trend. Meanwhile, the company claims to have filled a large part of its recent online orders with inventory trapped in stores.

Cash Power?

The management is pretty confident about the company’s liquidity position and expects to use it effectively to beat the slump. But experts are not very optimistic about the near-term prospects. Going by the current trend, it might take some time for the stock to recover from the recent lows, so it makes sense to hold it for now, or, delay investment decisions until the market stabilizes.

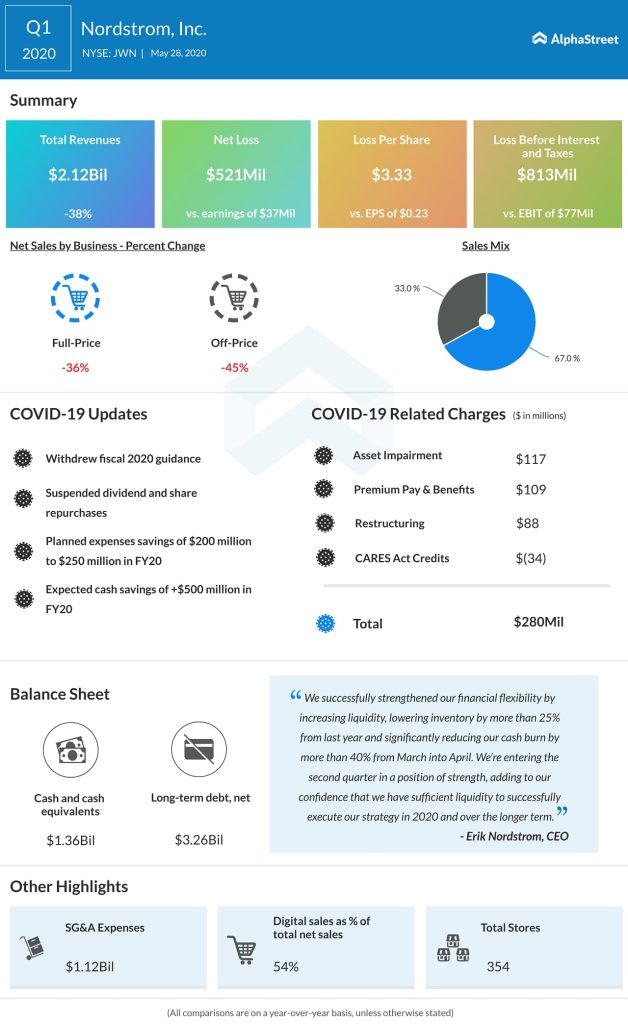

At last month’s earnings conference call, CEO Erik Nordstrom in his opening remarks said, “We increased our liquidity through proactive steps to shore up financing and reduce our cash burn. The significant reduction in our inventory levels enhances our financial flexibility and enables us to provide customers with a relevant merchandise offering across price points, brands, and key items. We’re confident that we have sufficient liquidity to execute our strategy in 2020 and over the longer-term.”

Q1 Fall

In the April-quarter, the company slipped to a loss of $3.33 per share from a profit of $0.23 per share last year. The negative earnings, after recording profit consistently for several quarters, was the result of a 40% plunge in revenues to about $2 billion. Online transactions accounted for nearly half of total sales. It was much worse than the outcome projected by market watchers, thanks to the widespread store closures that also prompted the management to withdraw its full-year guidance.

[irp posts=”63661″]

Nordstrom’s shares are currently trading about 75% below the record highs they reached a few years ago. The progressive downtrend was aggravated by the COVID-related selloff earlier this year. More recently, the stock suffered another setback following the dismal first-quarter results, though it pared a part of the loss later.