Shares of McCormick & Co. Inc. (NYSE: MKC) were down over 1% on Tuesday, despite the company delivering better-than-expected results for the first quarter of 2022. The stock has gained 7% over the past 12 months. The company reiterated its guidance for the full year and expects favorable food consumption trends to act as a tailwind for growth.

Quarterly results

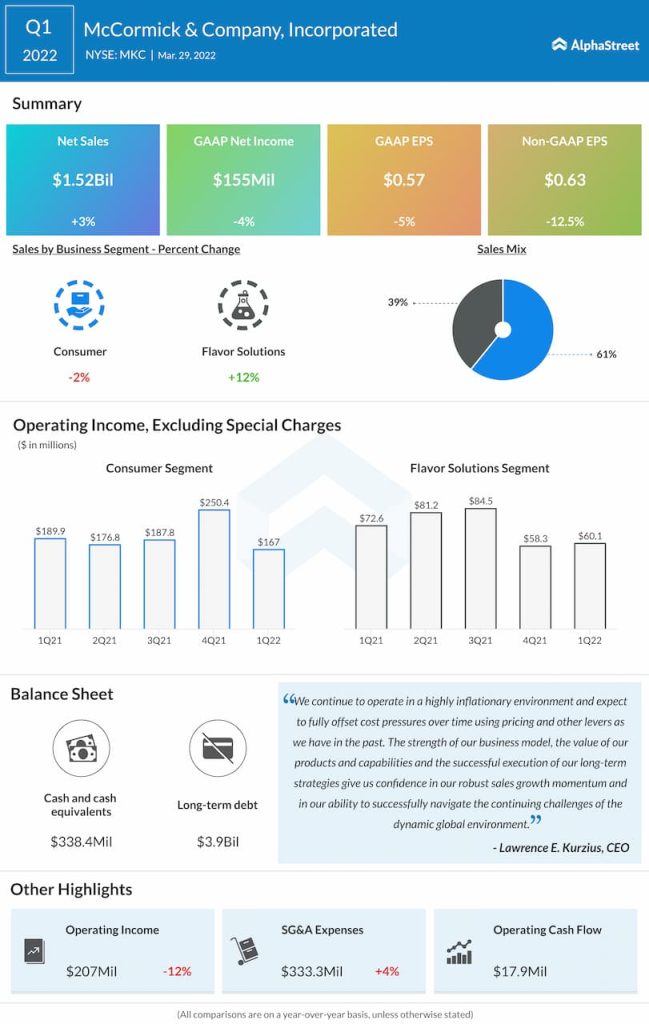

Net sales for the first quarter of 2022 increased 3% year-over-year to $1.52 billion, beating market estimates. In constant currency, sales grew 4%. GAAP EPS declined 5% to $0.57. Adjusted EPS dropped 12% to $0.63 but came above expectations. The bottom line was hurt by a drop in adjusted operating income caused by inflationary pressures.

Trends

McCormick continues to benefit from higher food-at-home consumption and it also saw strong demand from its foodservice and packaged food and beverage customers. Sales in the Consumer segment dropped 2%, reflecting a tough comparison against the 35% growth achieved in the prior-year quarter. The segment benefited from the trend of consumers cooking more meals at home.

Consumer sales in the Americas rose 2% helped by growth across the branded portfolio. Sales in the EMEA and Asia/Pacific regions fell 14% and 4% due to tough comparisons from the year-ago period. Sales in the Flavor Solutions segment increased 12%, helped by a pickup in away-from-home products and pricing actions. Flavor Solutions sales grew across all regions, driven by growth with packaged food and beverage companies, quick service restaurants and branded foodservice customers.

During the quarter, higher cost inflation negatively impacted gross profit margin leading to decline of 220 basis points. Operating income declined 12% to $207 million due to gross margin compression and other costs. Some of these pressures were offset by pricing actions and cost savings which the company will continue to implement through the year.

Outlook

Looking ahead to FY2022, McCormick expects to take advantage of customers’ rising preference for healthy and flavorful cooking, as well as their digital engagement and trust in brands. The company believes its strong portfolio will help meet the increasing global demand for flavor. This, combined with the company’s pricing actions and strategies, will help drive growth going forward.

For FY2022, sales are estimated to grow 3-5% year-over-year and 4-6% in constant currency. The top line growth is expected to be driven by new products, marketing, and customer engagement while pricing actions are expected to offset inflationary pressures. Operating income is expected to grow 13-15% YoY in 2022 while adjusted operating income is estimated to grow 7-9%. GAAP EPS is expected to range between $3.07-3.12 while adjusted EPS is estimated to grow 4-6% to $3.17-3.22.