After popularising the GPU technology about two decades ago, Nvidia Corporation (NASDAQ: NVDA) has dominated the market for that fast-growing microprocessor category so far. Of late, the chipmaker has been facing competition from Advanced Micro Devices, Inc. (NASDAQ: AMD) as the latter keeps expanding its clout in the graphics segment.

Very few Wall Street firms can claim the kind of growth Nvidia has achieved in the last two years, with the stock gaining more than four-fold during that period. After staying on an upward trajectory for several months, the stock hit an all-time high in early September, before withdrawing to the pre-peak levels later. Given the underlying strength, there is room for the stock to grow further, until at least the next earnings. The stock offers handsome returns at the current valuation, and those who can afford should go for it. It opened Wednesday’s trading at $560.

Stocks Peak

AMD’s past performance on the bourses shows that the stock behaved in a pattern similar to that of Nvidia. However, they are poles apart when it comes to the price -– currently trading slightly above $85, AMD is much more affordable. But unlike Nvidia, AMD seems to have peaked after the recent rally and the relatively high valuation makes it less attractive. Experts warn that the value might drop in mid-single-digit percentages in the coming months. In contrast, Nvidia has outperformed both AMD and the semiconductor industry so far this year.

Also read: AMD Q2 2020 earnings call transcript

After chasing semiconductor giant Intel (INTC) for a long time, AMD is currently enjoying an edge over its bigger rival by shipping the high-end 7nm processors that are a notch above their Intel equivalent. Though AMD was initially successful in gaining market share in GPU — an area considered to be Nvidia’s core competency — the latest data point to a climbdown from the prior-year levels.

Why Nvidia

The primary factor that gives Nvidia an advantage over others is its strong fundamentals and liquidity – operating cash flow was $1.6 billion at the end of the July-quarter. While market conditions are expected to remain favorable for chipmakers in the foreseeable future, largely due to the COVID-driven digital shift, Nvidia stands to benefit from the elevated GPU demand. At a time when AMD seems to have lost the GPU battle, at least for the time being, it faces a fresh threat from Nvidia’s latest graphics card that hit the market recently.

From Nvidia’s Q2 2021 earnings conference call:

“Despite near-term challenges, we are winning new business in areas such as healthcare, including Siemens, Philips, and General Electric and the public sector. We continue to expand our market opportunity with over 50 leading design and creative applications that are NVIDIA RTX-enabled, including the latest release from Foundry, Chaos Group, and Maxon.”

Emerging Trend

Being confined at home, due to lack of access to public places and educational institutions, the young population currently consumes more digital content than they did during the pre-pandemic days. As a result, there has been a surge in the demand for gaming chips, which accounts for nearly half of Nvidia’s sales. The company’s GeForce RTX GPUs are considered to be the most powerful chip architecture for both gamers and developers. Competitive pricing has pushed up orders so much that the management has warned of short-supply in the second half.

Related: NVIDIA Q2 2021 Earnings Call Transcript

It is a similar case with Nvidia’s data center business, which got a major impetus after the addition of Mellanox Technologies earlier this year. The deal brought together the firms’ capabilities in high-performance networking and data center technology. AMD, which is yet to catch up with Nvidia in the graphics sphere, witnessed a recovery in the sales of its enterprise-grade data center processor EPYC and desktop chip Ryzen this year. They had experienced weakness towards the end of 2019 due to cyclical factors.

Ends 1H on High Note

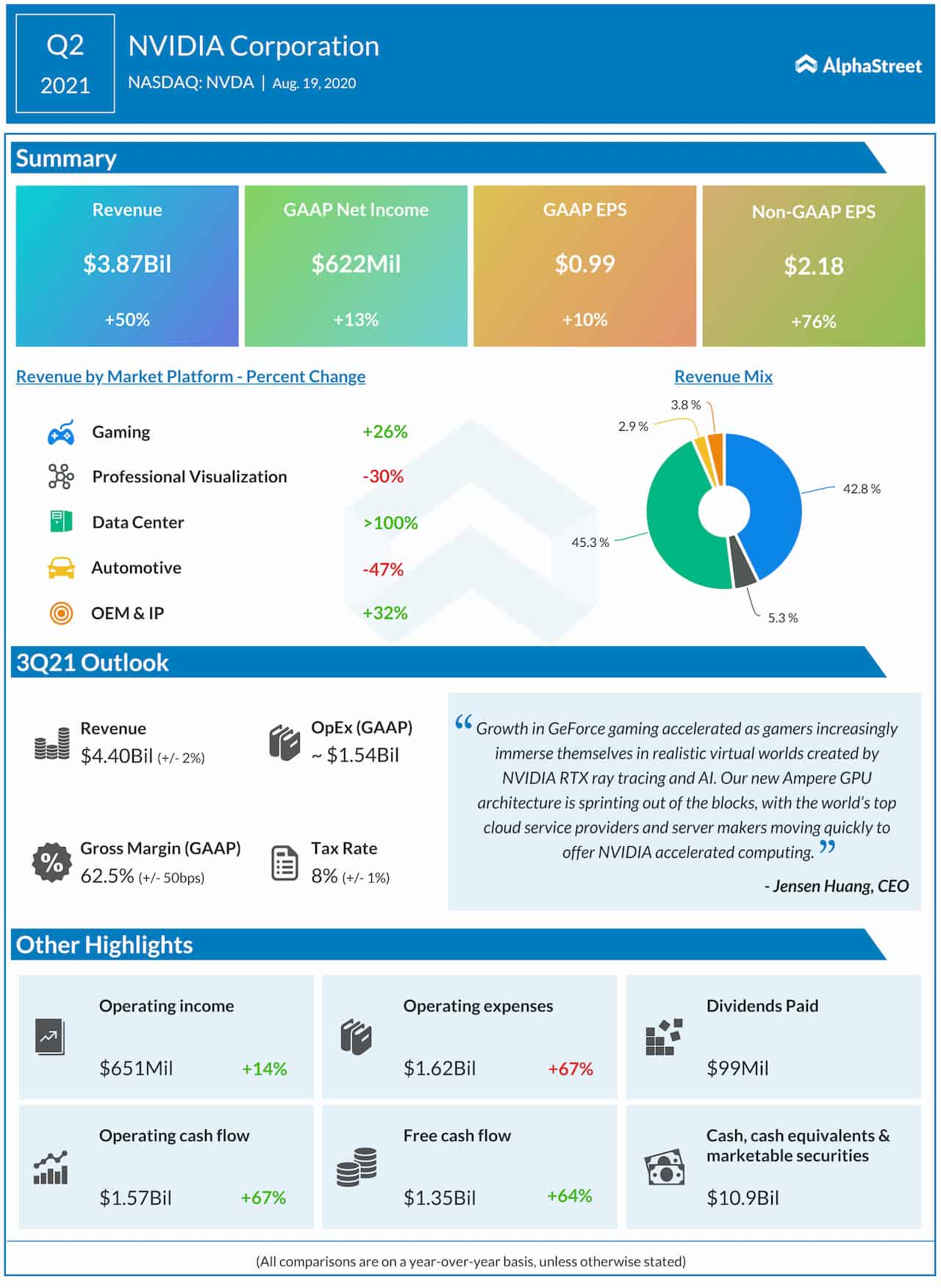

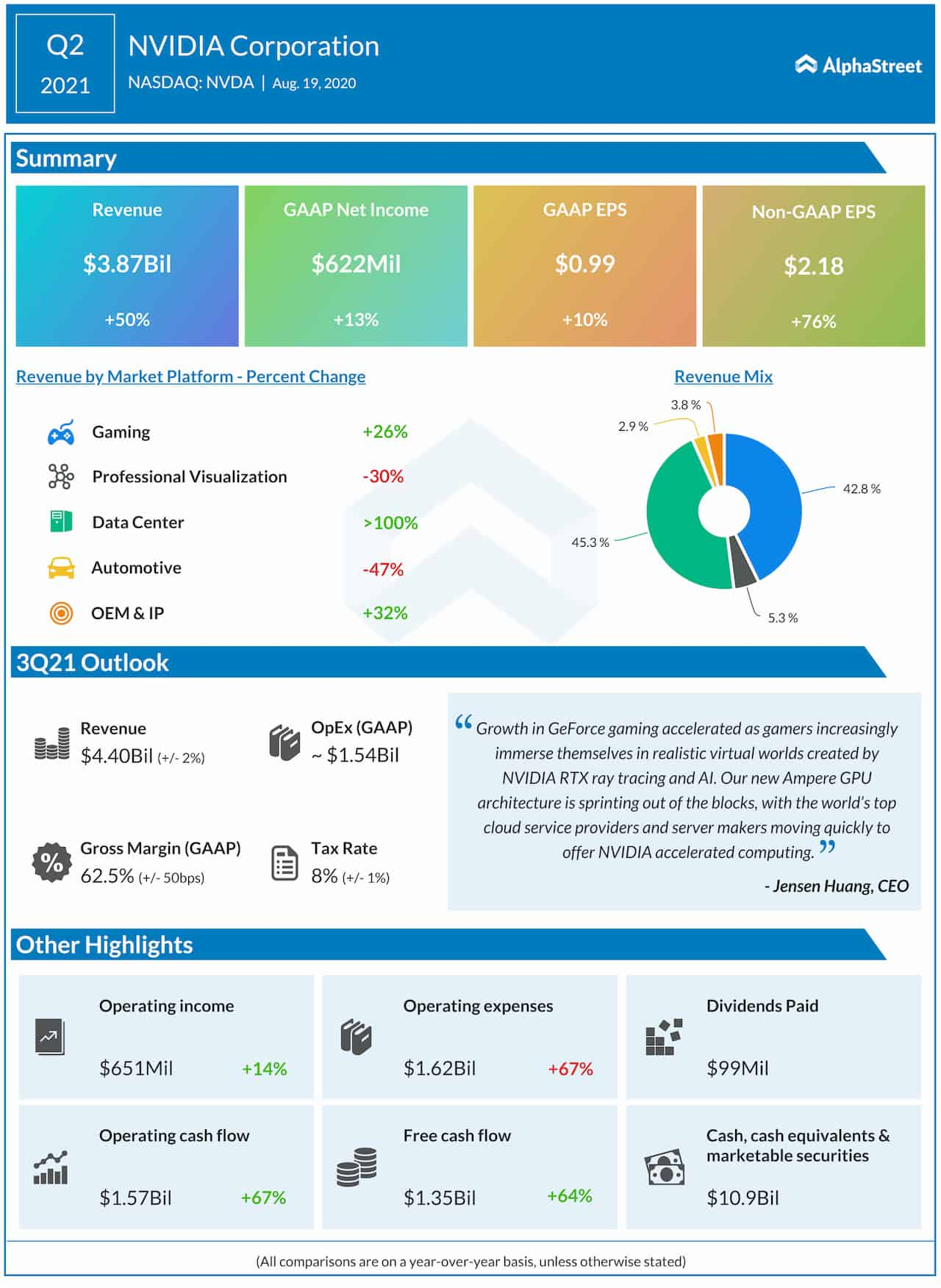

Higher demand for Nvidia’s core offerings translated into a sharp increase in revenues to $3.9 billion in the second quarter of 2021. Though operating expenses rose in double digits, it was offset by the 50% top-line growth. Consequently, net profit climbed 76% annually to $2.18 per share. The management expects a sequential increase in revenues and moderation in costs in the third quarter. It also sees a corresponding growth in gross margin, which was almost flat in the July-quarter.

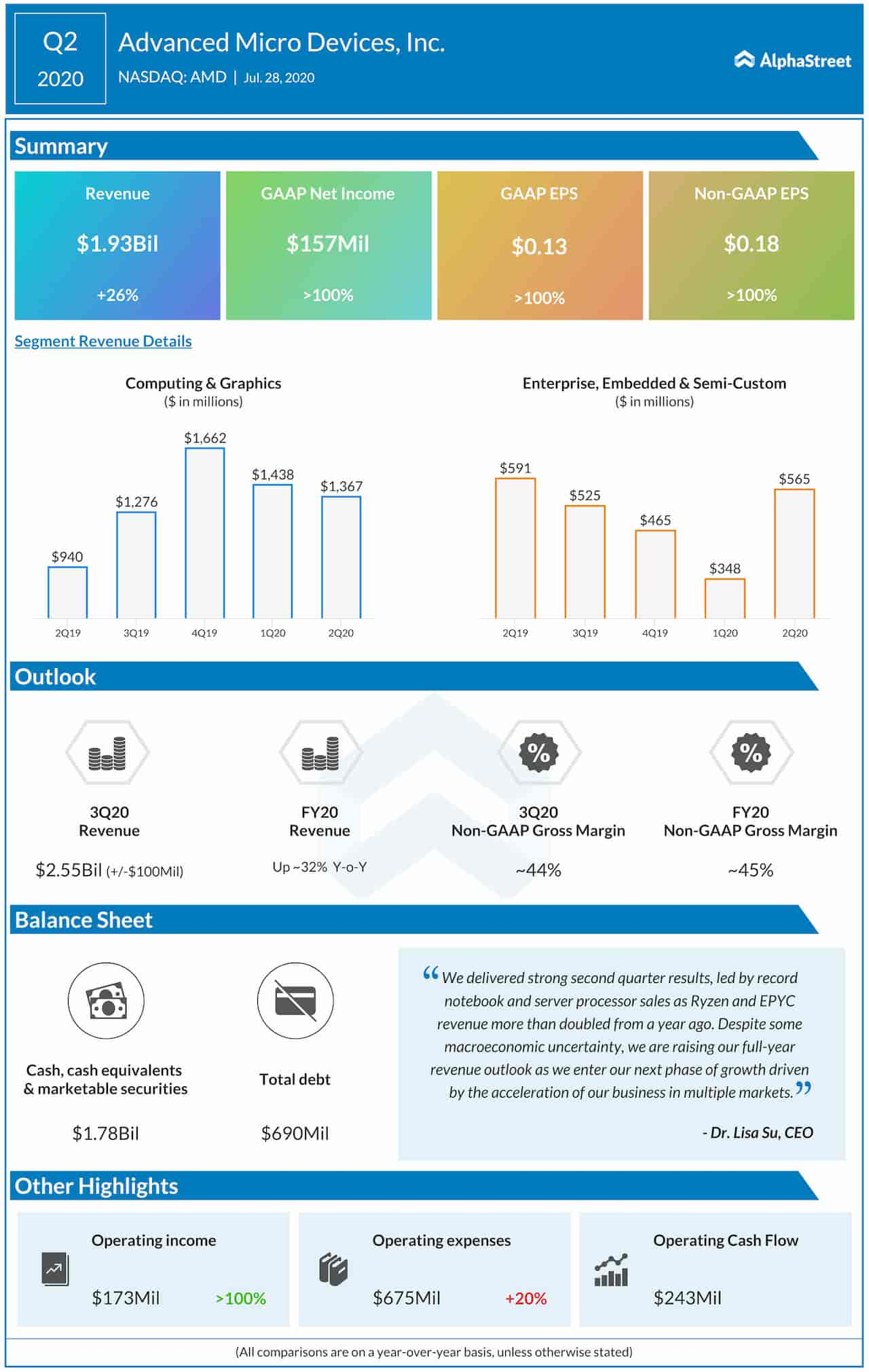

In July, AMD said its earnings more than doubled to $0.18 per share in the second quarter of 2020, when revenues grew by a quarter to $1.93 billion. The top line mainly benefited from higher computing processor sales, which was partially offset by weakness in the graphics segment. While AMD’s management remains bullish on the company’s prospects in the current quarter and full fiscal year, it has warned that macroeconomic uncertainties might weigh on performance.