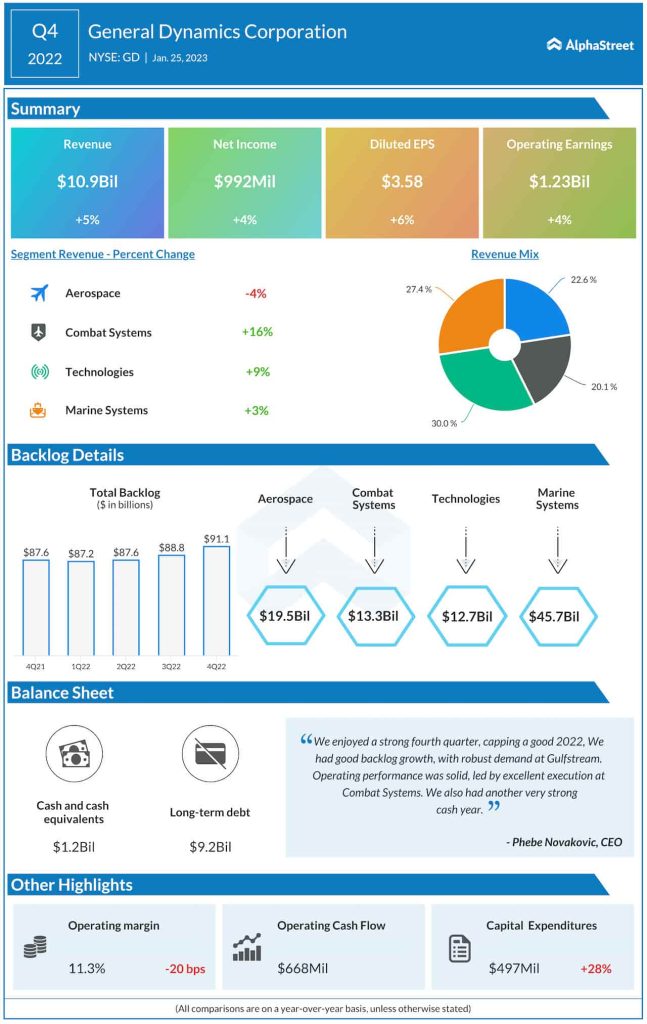

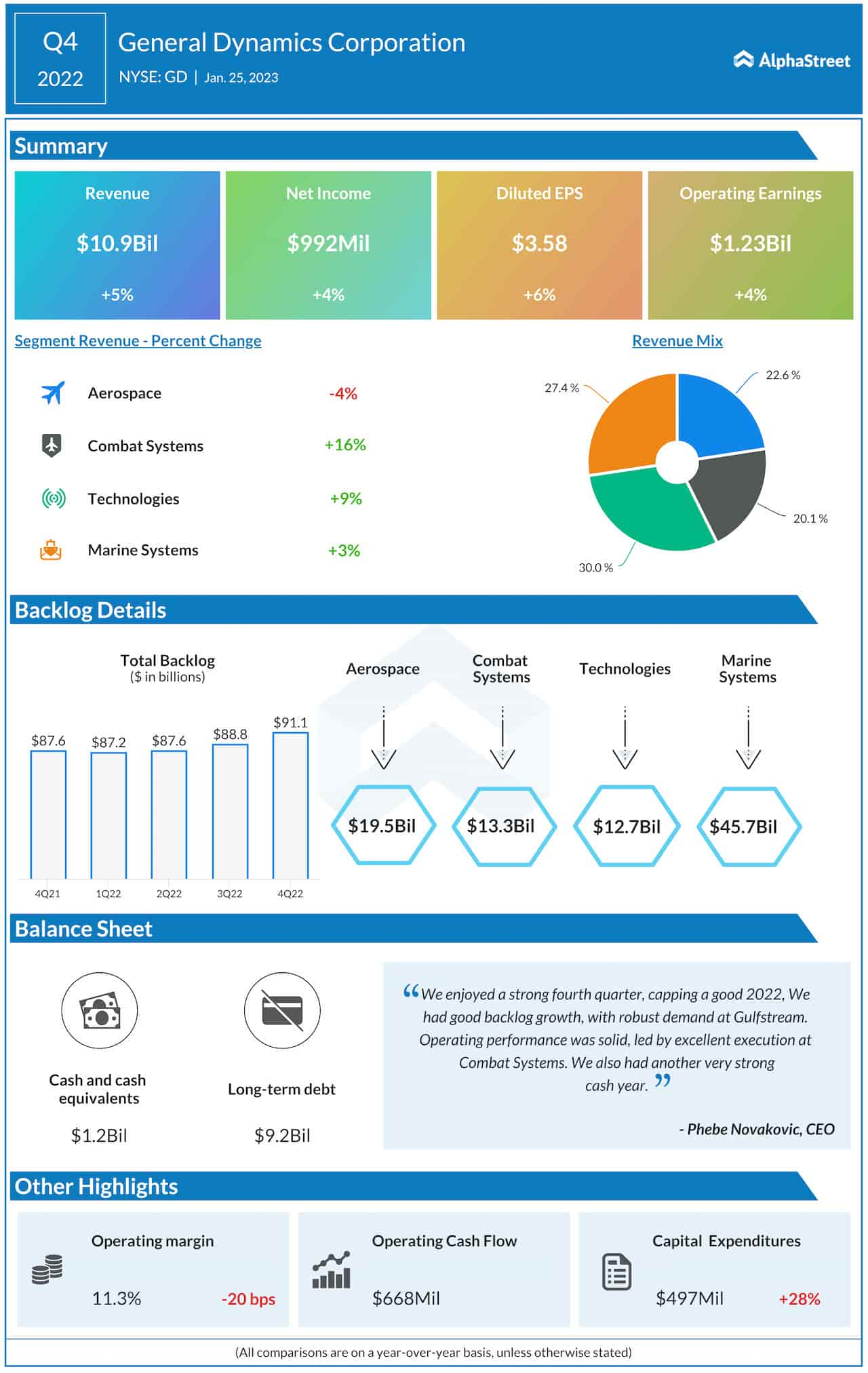

General Dynamics Corporation (NYSE: GD) is one of the most stable Wall Street companies, catering to the most important needs of the aerospace and defense industry globally. For the company, 2022 was a fruitful year in terms of contract wins and strengthening the balance sheet.

On Strong Footing

Unlike the majority of large-cap companies, General Dynamics’ business is more or less equally distributed among its four operating segments. This helps the company effectively deal with fluctuations in the performance of these business divisions. Considering the favorable backlog position and strong orders, the company seems to be headed for a strong 2023.

General Dynamics Corporation Q4 2022 Earnings Call Transcript

General Dynamics’ stock retreated from last month’s record highs and slipped below its long-term average, and the downturn continued after last week’s earnings announcement despite the positive results. Prospective investors, however, wouldn’t want to ignore experts’ bullish view on its finances, especially the robust cash flows that stood at a whopping $4.6 billion at the end of 2022. Also, the valuation is just right.

Pros & Cons

Meanwhile, taking a cue from the supply chain challenges and labor issues, the management issued cautious guidance for 2023, with the main numbers falling short of the market’s expectations. Those headwinds are expected to partially offset benefits from the growing demand for defense products. Another concern is the weakness in the information technology segment – which grew in low-single-digits in Q4 – and the company expects the slowdown to continue in the next few years. Beyond the short-term challenges, the company’s prospects remain encouraging, and so are the long-term investment opportunities.

Infographic: Lockheed Martin Q4 2022 revenue increases

Explaining the guidance for 2023, CEO Phebe Novakovic told analysts last week, “we anticipate an operating margin of 10.9%, up 20 basis points from 2022. This all goes up to a forecast range of $12.60 to $12.65 per fully diluted share. On a quarterly basis, we expect a pattern similar to what we’ve seen in recent years with sequential increases in revenue and operating margins throughout the year. As always, this forecast is purely from operations. It assumes we buy only enough shares to hold the share count steady to avoid dilution from option exercises.”

Q4 Outcome

Over the years, General Dynamics maintained strong profitability, with the quarterly numbers exceeding the market’s projections quite often. That reflects stable order growth that helped revenues to stay close to the $10-billion mark consistently. It was not different in the fourth quarter when revenues and net profit increased in mid-single digits to $10.9 billion and $3.58 per share, respectively, and topped expectations. In the whole of 2022, the company reduced its debt by $1 billion, returned $2.6 billion to shareholders, and invested $1.1 billion in capital expenditures.

GD traded higher throughout Monday’s session, making its position slightly better after the recent dip. The stock has dropped 8% so far this year, after a highly volatile 2022.