Like most technology companies, DocuSign Inc. (NASDAQ: DOCU) is riding the wave of the COVID-driven spike in digital transformation across the business world. The Silicon Valley tech firm, a pioneer of digital signature technology, has just wrapped its best quarter in recent years. The recent performance has also triggered speculation about the company’s future performance in the volatile market environment.

Stay tuned here to read management/analysts’ comments on earnings results

Though the stronger-than-expected second-quarter results pushed up the company’s shares initially, investor sentiment sagged later on Thursday when technology stocks witnessed a mass selloff that wiped out most of the recent gains. That caused the S&P 500 index to close sharply lower.

The pullback, despite the management projecting above-consensus numbers for the second half, is mainly attributable to the general slump in the sector amid concerns over the sustainability of the remote-work boom going forward. There is a possibility that people’s reliance on digital services would decline once the markets open up and work-from-home subsides.

Bullish View

However, the adoption of eSignature by new customers and the expansion of use cases by existing ones are expected to continue, which in turn should create new demand for other Agreement Cloud products also. In other words, the convenience offered by digital signature technology will be too irresistible for customers to ignore and switch back to the conventional process that involves physical documents.

Global Expansion

For the management, currently, international expansion is a key focus area. Chief financial officer Mike Sheridan, who will be taking over as the head of overseas operations, told analysts at the post-earning meeting, “I think a lot of what we’re seeing is that the structure of our international operations today look like what they were when we formed them four, five, six years ago, which is direct line reporting into headquarters, which is appropriate.”

When it comes to the pipeline, the company sees prospects both in the existing clients and new customers, considering the encouraging response to the concept of Agreement Cloud. With the right go-to-market strategy, it expects to generate significant demand for products like DocuSign CLM that complements eSignature.

Billings Surge in Q2

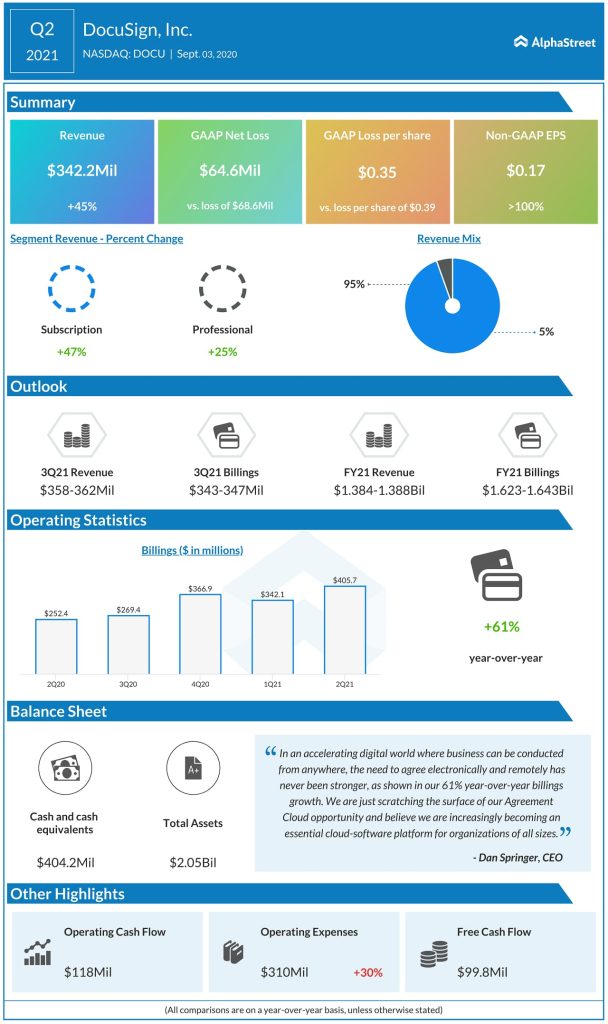

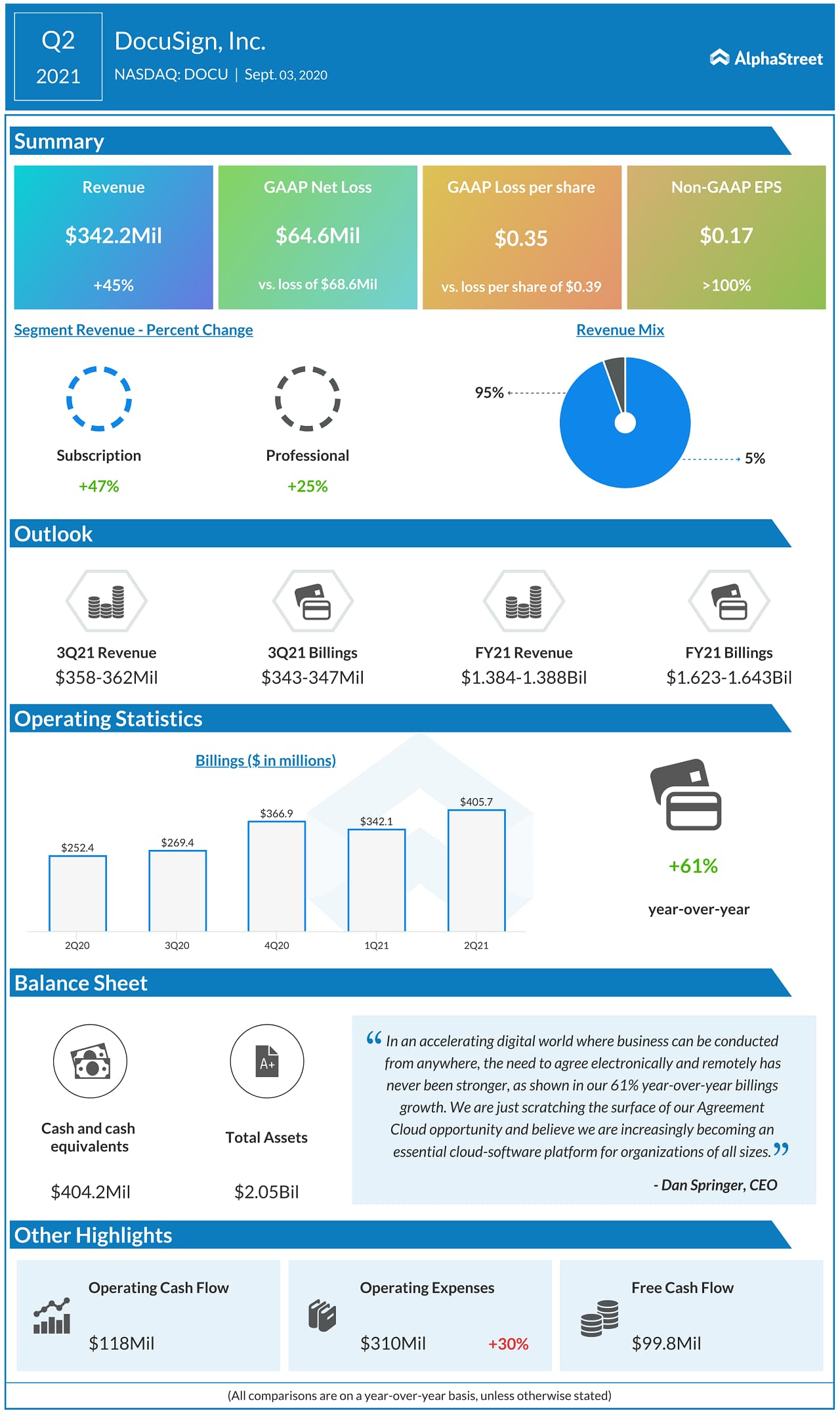

In the second quarter of 2021, adjusted earnings more than doubled to $0.17 per share as subscription business that accounts for about 95% of the total revenues witnessed strong growth. There was a 61% growth in total billings, reflecting the spurt in cloud migration during the pandemic period. The company added more new customers in the first half of the current fiscal year than it did in all of last year. There was an increase in demand from public sector entities.

DocuSign looks to leverage the positive momentum for its existing products during the COVID period and diversify into other areas of contract-management. After incorporating several new features into Agreement Cloud, plans are afoot to venture into remote online notary services and video-based solutions for certifying documents. The recent acquisition of Liveoak Technologies complements the initiative.

Our operating margins and cash flows reached record levels, while we continue to make key investments to address the heightened demand. As is evident from these numbers, the trends that emerged in the latter half of Q1 have continued throughout Q2. We’ve seen a sustained rise in demand for our core eSignature offering, not only from new customers but also those expanding across use cases, departments, and borders.

Dan Springer, chief executive officer of DocuSign

Stock Pulls Back

Shares of DocuSign dropped 19% this week alone, after hitting an all-time high of $268.6 at the beginning of the month. They closed Friday’s regular trading down 10%, after opening the session at $233.77. Meanwhile, the company’s market value nearly tripled since the beginning of the year.