The growing demand for new therapeutic solutions and advanced research in areas like human-genome will keep the biotechnology industry busy in the coming years. After throwing markets out of gear, the COVID-19 pandemic has stretched the healthcare system to the limit, often exposing its vulnerability. Retail pharmacy chain Walgreens Boots Alliance Inc. (NASDAQ: WBA), which has been at the forefront of the vaccination program, is facing COVID-related headwinds despite benefiting from the immunization drive.

Revenues of the Illinois-headquartered drug-store chain have remained under pressure from faltering patient-physician interactions, owing to movement restrictions, and its impact on margins could be a concern for shareholders. Meanwhile, the company’s stock is expected to extend the recent downtrend and settle near $50, which calls for caution as far as buying or selling is concerned.

Investing in WBA

Experts recommend adopting a wait-and-watch policy until the picture becomes more clear. That said, those willing to take risks can give the stock a try, for the relatively low valuation and decent dividends make it attractive.

From Walgreens’ Q2 2021 earnings conference call:

“Overall, we’re in a strong financial position to invest in future growth and to deliver shareholder returns. And the earnings we are reporting today show further evidence of that, with Q2 results ahead of expectations and giving us the confidence to raise full-year guidance, despite the significant operational impacts from COVID.”

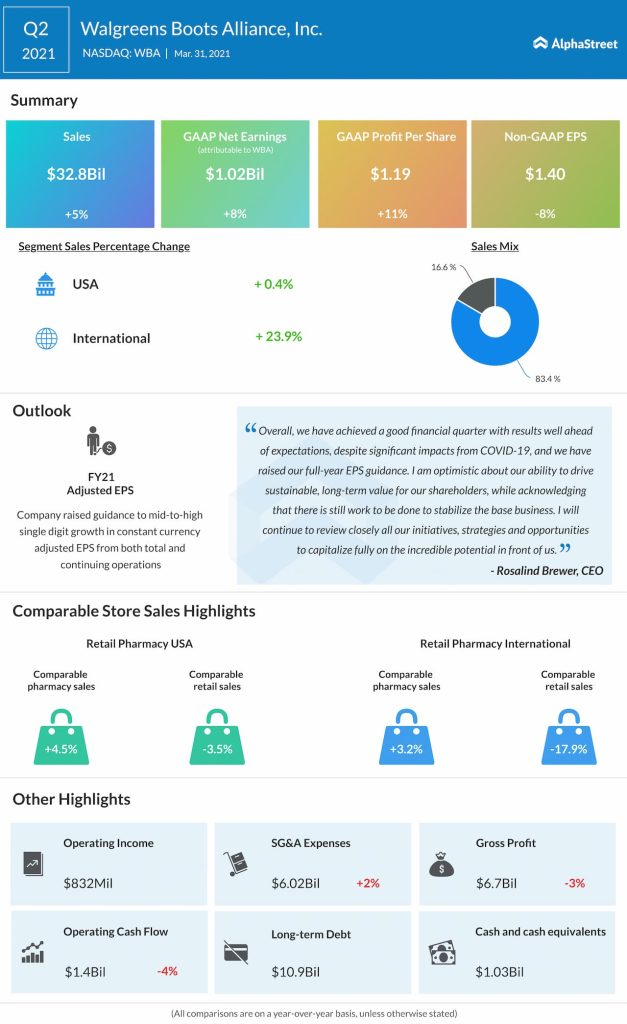

In the February quarter, domestic sales were almost flat while international sales grew in double-digits, driving the top-line up 5% to $32.8 billion. But earnings dipped 8% to $1.40 per share, hurt mainly by higher costs. Nevertheless, both numbers exceeded the market’s prediction, as they did in the trailing two quarters. Muted store traffic, postponement of elective procedures, and decline in prescriptions were a drag on performance.

Despite the mixed outcome, the management raised the earnings growth guidance for fiscal 2021 to mid-to-high single-digit from the low single-digit growth estimated earlier.

Alliance Sale

Earlier this year, the management announced an organizational restructuring with focus on divesting the Alliance Healthcare business and a part of the European arm of Retail Pharmacy International to AmerisourceBergen. Under the plan, the remaining businesses were reorganized into the United States segment and the International segment.

Read management/analysts comments on Walgreens’ Q2 earnigns

The new organizational setup, together with investments in VillageMD to open its units at Walgreens primary care clinics, should drive growth going forward. Also, rising e-commerce capabilities — marked by facilities like curbside pick-up and drive-thru — and the recovery of retail pharmacy business, especially in the overseas market, might help the company overcome the COVID impact. Margins stand to benefit from the management’s cost reduction program, even as the long-term earnings and revenue trends look positive.

At the Bourses

Walgreens’ shares witnessed one of the biggest one-day gains after the earnings announcement this week, but they retreated in the following session. The stock, which has gained 33% in the past three months, traded higher Thursday afternoon.