Fast-food chain Chipotle Mexican Grill, Inc. (NYSE: CMG) has successfully turned the COVID-related movement restrictions into its favor by leveraging its strong digital infrastructure. Unlike many restaurant chains that suffered significant sales slumps during the shutdown, Chipotle remained largely unaffected, rather it gained from strong online orders.

Ending a downtrend, the company’s stock moved up after it reported strong fourth-quarter results this week, marking one of the biggest single-day gains in recent times. On the positive side, CMG has become a lot cheaper than it used to be, offering a rare opportunity to those waiting for an entry point. But many prospective buyers would still find the stock expensive.

Read management/analysts’ comments on Chipotle’s Q4 results

CMG was considered overvalued after the share price more than tripled since the early days of the pandemic. It made steady gains and reached an all-time high of $1944.05 in September last year, before paring a part of the gains later. If analysts’ bullish outlook is any indication, the post-earnings recovery will continue. The majority of experts recommend buying the stock, with a target price of $1931.53.

Digital Prowess

The company keeps bringing innovation to its online platform, mobile app, and third-party delivery services to boost sales. The response to its loyalty program has been encouraging so far. Buoyed by the success of new-town opportunities, Chipotle executives have raised their long-term expansion target — now aim to reach 7,000 restaurants in North America, compared to the earlier goal of 6,000 units. The idea is to boost customer experience by ensuring better access and convenience. It is worth noting that the company operated only 2,966 restaurants at the end of the fourth quarter.

“As a result of this pandemic, many new consumers were introduced to Chipotle via our digital channels and are now using us for alternative and, at times, incremental occasions. Having two large and growing businesses that are supported by separate make-lines makes it easy for guests to access Chipotle through different channels and is a key point of differentiation. Currently, about two-thirds of our guests use in-restaurant as their exclusive channel, with the remainder using Chipotle’s digital ecosystem to conveniently access our real food,” said Chipotle’s CEO Brian Niccol at the earnings conference call.

Risks

Currently, the main challenge facing Chipotle is elevated costs, mainly related to labor and raw materials, but the management has tackled the issue to a great extent by hiking prices. Also, the COVID-related uncertainties and emergence of new variants like omicron do not bode well for the company as far as its growth initiatives are concerned.

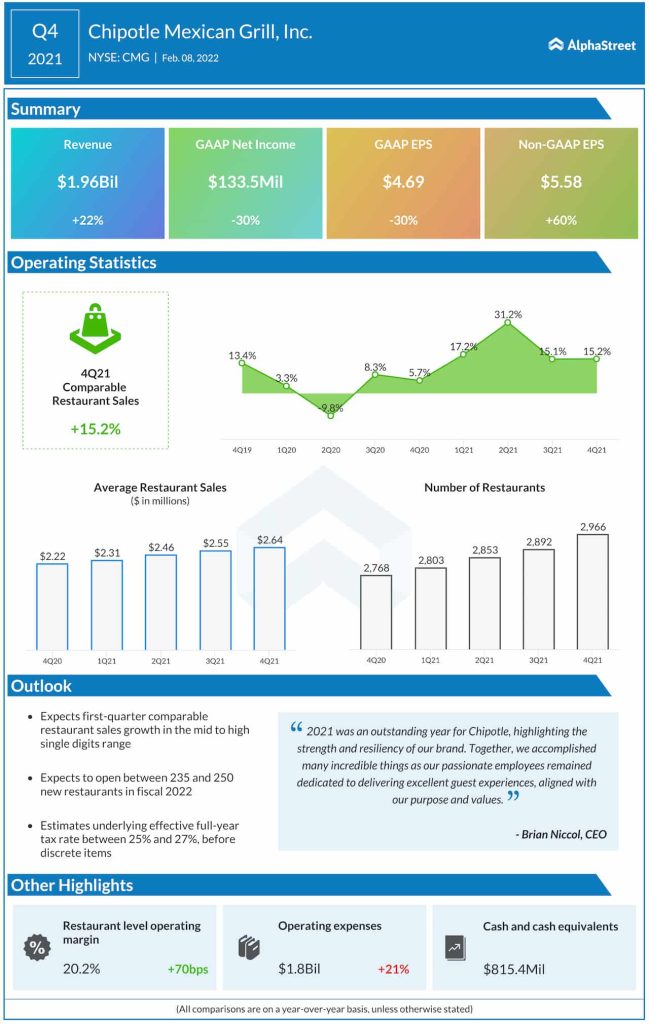

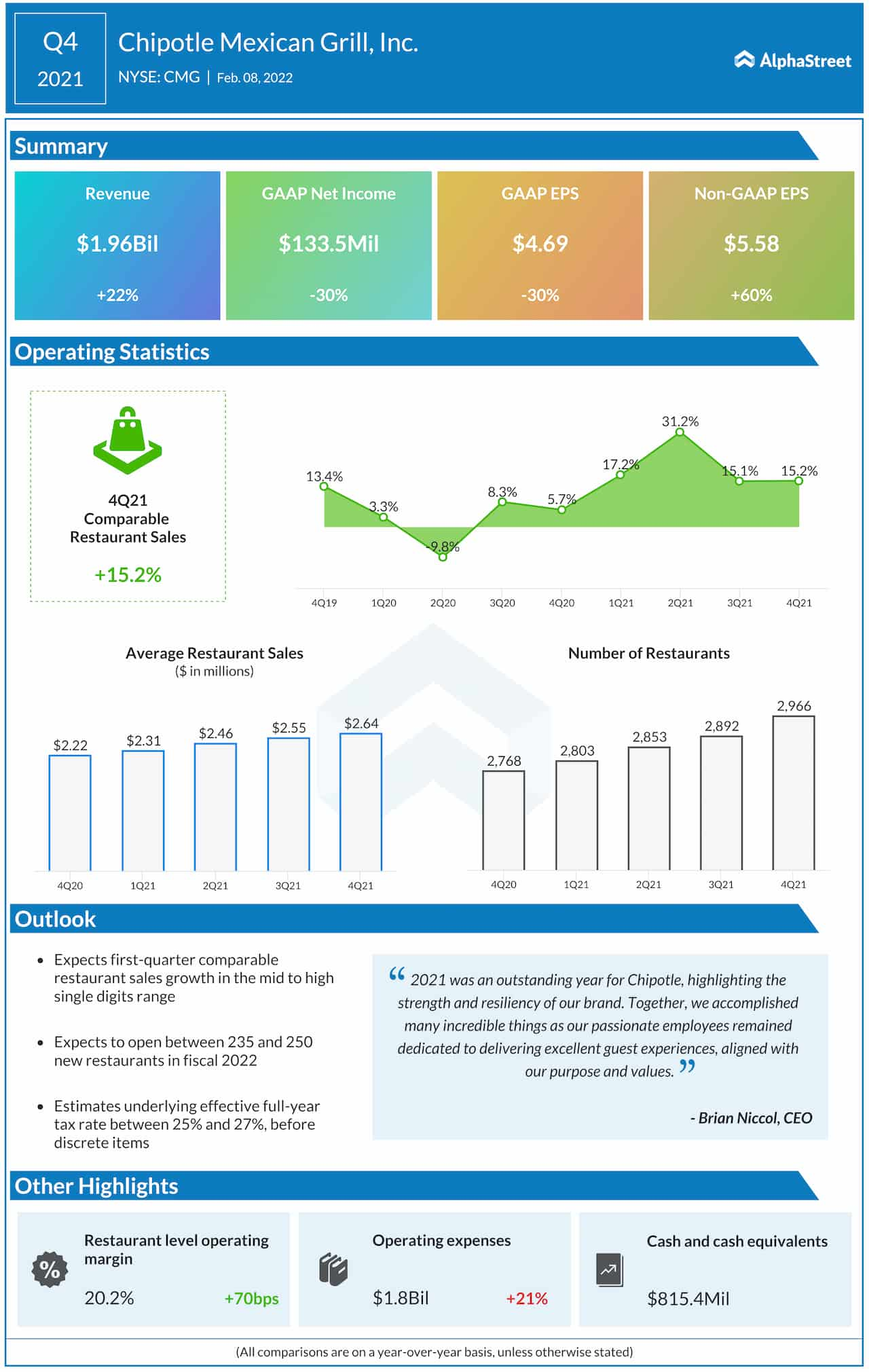

Earnings beat analysts’ estimates in each of the trailing four quarters when the top-line either topped or matched expectations. In the final three months of fiscal 2021, comparable restaurant sales grew by 15.2% driving up total revenues to $1.96 billion, which is in line with the market’s projection. At $811.3 million, digital sales were up 4% year-over-year. As a result, adjusted earnings jumped 60% annually to $5.58 per share, exceeding the consensus forecast.

Earnings: Starbucks Q1 profit misses estimates, comp sales up 13%

CMG experienced high volatility after peaking a few months ago. The stock, which has lost 17% so far this year, opened Wednesday’s session at $1,575.34 and traded higher in the afternoon.