The market reopening and economic recovery have eased the squeeze on people’s spending power to a great extent, marking an improvement from the peak months of the pandemic when customers mostly opted for pre-owned vehicles to save money. CarMax, Inc. (NYSE: KMX), a leading used car retailer, striving to maintain the COVID-driven sales boom through innovation.

However, it looks like investors are not impressed by CarMax’s solid performance. This week, the Richmond-based company’s stock traded at the lowest level in more than two years, but the downturn is unlikely to continue for a long time. Experts are of the view that the stock would reach around $145 in the next twelve months, which represents a 42% growth from the current levels.

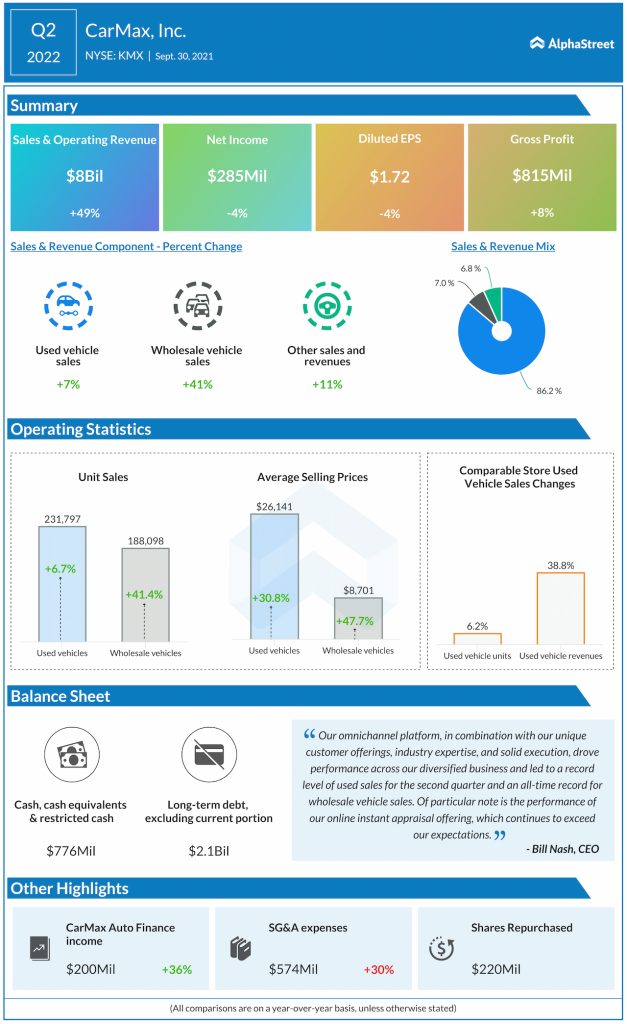

Read management/analysts’ comments on CarMax’s Q3 2021 earnings

The lower valuation and better affordability make KMX an attractive investment. Going by the current trend, the stock has the potential to create handsome shareholder value in the long term.

Resilience

Proving the skeptics wrong, CarMax maintained stable growth in sales and gross profit in recent quarters, even after the pandemic-related tailwinds subsided due to market reopening, thanks to its successful business model. It is mainly attributable to the company’s aggressive efforts to enhance omnichannel capabilities. There has been a steady increase in online sales.

There is enough reason to believe that customers would continue to be attracted by CarMax’s convenient and hassle-free platform that seamlessly integrates offline and online channels. It is worth noting that in the most recent quarter, at least one of the four components of the company’s omnichannel system was involved in about half of the total sales. At the same time, the company outperformed competitors and maintained its dominance in the sector in terms of sales volume.

From CarMax’s Q3 2021 earnings conference call:

“We’ve been focused on completing the rollout of our 100% self-service experience, where customers if they choose to can independently complete the entire car-buying process online. Currently, more than two-thirds of our customers have access to a complete end-to-end unaided online experience, an increase from a little over 50% from our last call. This expansion reflects customers’ ability to incorporate trade-ins without liens [Phonetic] to their online orders.”

Q3 Outcome

In the third quarter of fiscal 2022, net revenues climbed 65% annually to $8.5 billion. Reflecting the strong sales, net income increased to $269.4 million or $1.63 per share from $235.3 million or $1.42 per share in the year-ago quarter. The numbers also topped analysts’ estimates. The company sold 415,054 units through its combined retail and wholesale channels, which is up 29.3%.

Infographic: Highlights of Ford Motor’s Q4 2021 earnings report

Meanwhile, CarMax faces stiff competition from the likes of AutoNation, with every player in the thriving market aggressively vying for a bigger share of it. Also, there is a looming threat of brand-new vehicle manufacturers eating into the market for pre-owned vehicles as the economic recovery gathers steam.

Shares of CarMax lost about 21% so far this year, after ending 2021 on an upbeat note. The stock traded lower early Wednesday, after opening the session slightly above the $100-mark.